")

Celsius Holdings, Inc. CELH and Monster Beverage Company MNST are two outstanding names within the world vitality drink class, working at completely different ends of the expansion and scale spectrum. CELH is a fast-growing practical beverage firm targeted on zero-sugar, health-oriented vitality merchandise. The corporate has delivered outsized income development in 2025, pushed by portfolio enlargement and market share good points within the U.S. vitality class, and carries a market capitalization of roughly $11.5 billion.

Monster Beverage, against this, is a mature, world vitality drink chief with a broad portfolio led by Monster Vitality, Monster Extremely, Reign and different manufacturers, supported by deep worldwide distribution and powerful working leverage. MNST generates considerably greater revenues and profitability, with constant margin enlargement and a robust world footprint, translating right into a a lot bigger market capitalization of $75.6 billion.

Celsius Holdings and Monster Beverage are value evaluating now as they symbolize two structurally completely different performs on the identical class, making this a well timed face-off throughout the evolving vitality drink panorama.

The Case for CELH

Celsius Holdings is a high-growth challenger within the vitality drink class, pushed by sturdy model momentum and increasing distribution. The core CELSIUS model stays one of many fastest-growing vitality drinks in america, with continued market-share good points throughout comfort, mass and grocery channels. Retail takeaway remained wholesome within the third quarter of 2025, supported by higher shelf placement, expanded cooler presence and stronger merchandising beneath PepsiCo’s distribution community.

The corporate can be accelerating development by means of portfolio enlargement and integration. The transition of Alani Nu into PepsiCo’s direct-store-delivery system (starting Dec. 1) is predicted to meaningfully broaden distribution and visibility into early 2026. As well as, Rockstar Vitality gives entry to a broader shopper base and creates longer-term model revitalization alternatives as Celsius works to optimize manufacturing and sourcing.

Innovation stays a key development driver. Restricted-time choices, seasonal launches and a gradual stream of latest flavors throughout CELSIUS and Alani Nu proceed to resonate with youthful customers. Administration highlighted sturdy efficiency from latest taste launches, reinforcing Celsius’ capability to remain related in a aggressive class targeted on style, performance and clean-label attributes.

Celsius can be seeing advantages from an enhancing margin profile. Gross margin remained above 50% within the third quarter, supported by decrease promotional depth, improved income combine and operational efficiencies in freight, warehousing and co-packing. Elevated scale inside PepsiCo’s DSD community and clearer co-manufacturing plans are serving to enhance price alignment.

That stated, near-term outcomes could stay unstable. Administration expects the fourth quarter to be “noisy,” reflecting integration prices, distributor transitions, stock returns and timing-related impacts from Alani Nu’s community shift. Greater freight, advertising and marketing spend and non permanent co-packing inefficiencies could strain margins, whereas Rockstar is unlikely to contribute meaningfully to profitability till 2026. Regardless of these headwinds, shopper takeaway traits stay constructive, supporting the longer-term development outlook.

The Case for MNST

Monster Beverage stays a dominant, world chief within the vitality drink class, supported by sturdy model fairness, broad distribution and constant execution. The corporate continues to ship strong top-line development, pushed by sustained demand for its core Monster Vitality franchise and increasing traction throughout worldwide markets. Administration highlighted regular shopper takeaway traits, underscoring MNST’s resilience in amid a aggressive and promotional surroundings.

Innovation stays central to Monster’s development technique. The corporate continues to refresh its portfolio by means of new taste launches, extensions of the Monster Extremely line and focused choices beneath manufacturers equivalent to Reign and Java Monster. These launches are designed to seize incremental events, attraction to evolving shopper preferences and defend shelf area towards rising rivals.

Monster’s world footprint is a key aggressive benefit. Worldwide markets proceed to publish sturdy development, supported by the corporate’s long-standing strategic partnership with The Coca-Cola Firm, which gives unmatched distribution attain and execution capabilities. Administration emphasised continued momentum throughout the EMEA, Asia-Pacific and Latin America, serving to offset class normalization in components of North America.

Profitability stays a core energy. Monster Beverage continues to generate wholesome working margins and powerful money stream, supported by scale advantages, disciplined price management and favorable pricing actions. Whereas enter prices and logistics stay areas of focus, administration indicated that margins stay well-supported, reflecting the corporate’s capability to soak up price pressures.

Total, Monster Beverage represents a high-quality, cash-generative vitality drink chief with sturdy manufacturers, world scale and a confirmed working mannequin. Whereas development is extra average in contrast with smaller friends, MNST’s consistency, margin energy and worldwide enlargement runway place it properly for long-term worth creation, making it a compelling core holding throughout the beverage area.

How Does the Zacks Consensus Estimate Examine for CELH & MNST?

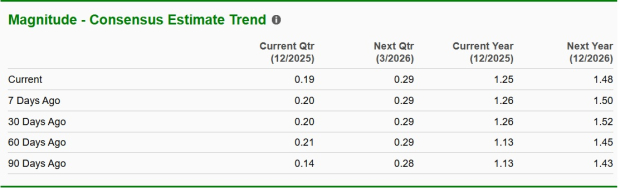

The Zacks Consensus Estimate for CELH’s present fiscal-year gross sales and earnings per share counsel a year-over-year enhance of 79.7% and 78.6%, respectively. The consensus estimate for EPS for the present fiscal 12 months has declined by a penny to $1.25 over the previous seven days. The consensus mark for the following fiscal-year gross sales and EPS implies year-over-year development of 32.8% and 18.7%, respectively. The consensus mark for EPS has dropped from $1.50 to $1.48 over the previous seven days.

Picture Supply: Zacks Funding Analysis

The Zacks Consensus Estimate for MNST’s present fiscal-year gross sales and EPS implies year-over-year development of 9.7% and 22.8%, respectively. The consensus estimate for EPS for the present fiscal 12 months has elevated from $1.98 to $1.99 over the previous seven days. The consensus mark for the following fiscal-year gross sales and EPS suggests a year-over-year soar of 9.5% and 13.2%, respectively. The consensus mark for EPS has risen by a penny to $2.25 over the previous seven days.

Picture Supply: Zacks Funding Analysis

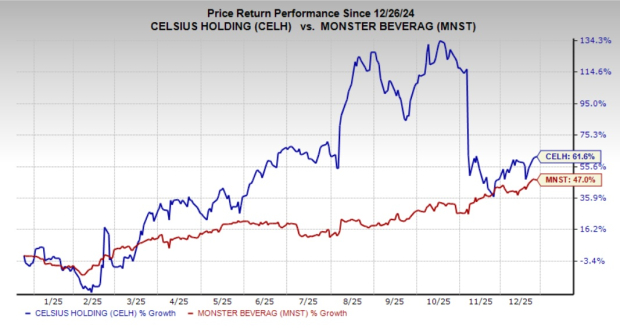

CELH & MNST: A Have a look at Previous-Yr Inventory Efficiency

Over the previous 12 months, shares of Celsius Holdings have surged 61.6% in contrast with Monster Beverage’s soar of 47%.

Picture Supply: Zacks Funding Analysis

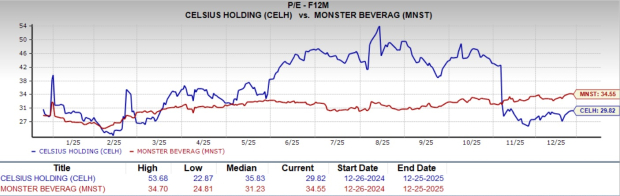

CELH & MNST: A Peek Into Inventory Valuation

Celsius Holdings’ ahead 12-month P/E of 29.82 stands under its one-year median of 35.83, indicating the inventory is buying and selling at a relative low cost to its latest growth-driven valuation. Monster Beverage’s ahead P/E of 34.55 sits above its median of 31.23, suggesting the inventory is valued at a modest premium to its latest historic vary. MNST’s premium valuation underscores its standing as a high-quality, cash-generative chief within the vitality drink class, with traders prepared to pay up for consistency, model energy and a protracted runway for worldwide development.

Picture Supply: Zacks Funding Analysis

CELH & MNST: Which Is the Higher Guess Now?

Each Celsius Holdings and Monster Beverage are well-positioned to profit from the long-term development of the vitality drink class, although by means of completely different paths. Celsius provides a lovely development profile, supported by sturdy model momentum, increasing distribution and a rising innovation pipeline, although near-term execution dangers and integration-related volatility stay. In the meantime, Monster Beverage stands out for its scale, consistency and world attain, underpinned by sturdy manufacturers, sturdy money era and a confirmed working mannequin. At this juncture, MNST seems higher suited to traders looking for stability and regular development, whereas CELH stays an interesting possibility for growth-oriented traders prepared to tolerate near-term variability.

MNST sports activities a Zacks Rank #1 (Sturdy Purchase), whereas CELH at present carries a Zacks Rank #3 (Maintain). You’ll be able to see the whole record of at the moment’s Zacks #1 Rank shares right here.

Zacks Naming Prime 10 Shares for 2026

Wish to be tipped off early to our 10 prime picks for the whole thing of 2026? Historical past suggests their efficiency might be sensational.

From 2012 (when our Director of Analysis Sheraz Mian assumed duty for the portfolio) by means of November, 2025, the Zacks Prime 10 Shares gained +2,530.8%, greater than QUADRUPLING the S&P 500’s +570.3%.

Now Sheraz is combing by means of 4,400 corporations to handpick the perfect 10 tickers to purchase and maintain in 2026. Don’t miss your likelihood to get in on these shares once they’re launched on January 5.

Be First to New Prime 10 Shares >>

Monster Beverage Company (MNST) : Free Inventory Evaluation Report

Celsius Holdings Inc. (CELH) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.