The house furnishings trade continues to face vital headwinds, and Ethan Allen Interiors Inc. (ETD) stays firmly on the defensive. Persistent strain from commerce tensions, a sluggish housing market, and shifting shopper spending patterns has weighed on furnishings and residential decor demand, leaving little room for earnings development.

Ethan Allen’s efficiency displays these challenges. ETD inventory has underperformed throughout a number of timeframes, lagging each its friends and the broader market over the previous one, three, and ten years. Regardless of a short post-pandemic rebound, gross sales have been primarily flat for a number of years, and up to date quarterly outcomes present no indicators of significant acceleration.

Technically, the chart is deteriorating once more, with shares showing susceptible to a different breakdown. Essentially, the outlook has worsened as analysts have minimize earnings estimates sharply in latest weeks, citing weak order developments and margin strain. But the inventory nonetheless trades at a premium to its historic valuation, leaving little cushion if situations deteriorate additional. For now, the danger/reward stability skews clearly to the draw back.

Picture Supply: Zacks Funding Analysis

Ethan Allen Interiors Inventory Will get Downgraded

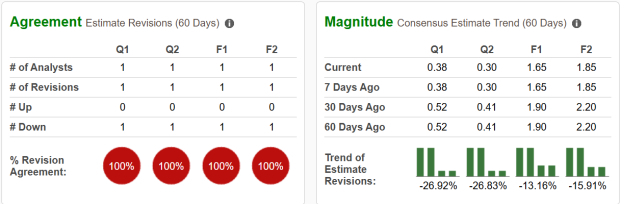

Ethan Allen Interiors has seen a wave of downward earnings revisions over the previous week, with the tempo of cuts accelerating. Whereas estimates have been trending decrease since late 2023, the declines have lately grow to be extra pronounced, with present quarter projections are down almost 27%, and full yr estimates have fallen 13.2%. Because of this, the inventory now carries a Zacks Rank #5 (Robust Promote) score.

Valuation provides to the strain. ETD presently trades at 14.3x ahead earnings, a reduction to the broader trade common however nonetheless effectively above its five-year median of 10.6x. Given the corporate’s weakening outlook and comfortable demand backdrop, this premium seems tough to justify. Except earnings expectations stabilize, the mixture of estimate cuts and an elevated a number of suggests additional draw back threat for the inventory.

Picture Supply: Zacks Funding Analysis

Shares of Ethan Allen Breakdown

The latest worth motion in ETD inventory displays its weakening fundamentals. After buying and selling principally sideways for the previous two years, shares have now damaged under a key assist degree, confirming a technical breakdown. The lack of this assist aligns with the corporate’s deteriorating earnings outlook and accelerating analyst downgrades.

So long as the inventory stays under that prior assist zone, momentum favors the draw back. Buyers could wish to keep on the sidelines till Ethan Allen exhibits indicators of stabilization in each its fundamentals and chart sample.

Picture Supply: TradingView

Ought to Buyers Keep away from ETD Inventory?

Given the accelerating earnings downgrades, weak gross sales developments, and confirmed technical breakdown, Ethan Allen Interiors seems positioned for additional weak spot. The corporate’s elevated valuation leaves restricted margin for error, and trade situations stay unfavorable.

Till earnings stabilize and demand within the dwelling furnishings market improves, traders are seemingly higher off avoiding ETD and specializing in sectors with clearer development catalysts and stronger momentum.

Quantum Computing Shares Set To Soar

Synthetic intelligence has already reshaped the funding panorama, and its convergence with quantum computing may result in essentially the most vital wealth-building alternatives of our time.

Right now, you’ve gotten an opportunity to place your portfolio on the forefront of this technological revolution. In our pressing particular report, Past AI: The Quantum Leap in Computing Energy, you may uncover the little-known shares we consider will win the quantum computing race and ship large features to early traders.

Ethan Allen Interiors Inc. (ETD) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.