Whereas macroeconomic and geopolitical challenges mount, the ecommerce market is rising by means of innovation, expertise and perception, because it continues to remove slices of the entire retail pie. Commerce Division numbers are proof of this pattern: ecommerce gross sales within the first quarter of 2026 grew 9.8% over 1Q25 (2.7% sequentially), with complete retail gross sales rising 3.9% (1.5% sequentially). Ecommerce accounted for round 16.9% of complete U.S. retail gross sales. A degree to notice right here is that buyers are more and more mixing their on-line and offline procuring experiences, so this distinction could in the end change into irrelevant. As a corollary, it’s these retailers which have the capability to promote by means of each channels that can be capable of compete tomorrow.

Whereas ecommerce continues to take share from conventional retail, the tempo has moderated. Moreover, geopolitics is a serious problem for ecommerce gamers in the intervening time given the wars, tariffs and tensions between nations as we speak which are disrupting provide chains, rising prices and decreasing efficiencies. This creates a extremely aggressive surroundings the place progress comes primarily from worth competitors and share features.

Our picks Wayfair W and Carvana CVNA are doing exactly that. Wayfair gives an enormous vary of house enchancment merchandise together with nationwide infrastructure and logistics in a sexy format that permits it to document vital share features. It has trimmed its value construction, so its surging revenues are falling by means of to the underside line. Carvana is seeing even stronger share features, because it gives a superior on-line shopping for expertise in a used-car market that’s nonetheless largely brick-and-mortar.

Each corporations are delicate to rate of interest actions nonetheless, subsequently the newest FOMC deliberations will not be supportive. We consider they may proceed to develop regardless due to their distinctive capabilities and market positioning.

The comfort of on-line procuring (notably by means of cellular units) stays the highest cause for ecommerce volumes, together with the merging of bodily and digital channels. Gen-Z is the largest driver, which is, more and more, the extra related demographic.

Many of those consumers have grown up on the Web and are accustomed to a excessive stage of digitization. They’re additionally probably to hang around on widespread social media platforms, permitting themselves to be influenced by the newest tendencies there. That is driving a wholly completely different perspective on the ecommerce house, one which revolves round digital influencers and seems to be increasing with extra superior expertise similar to AR/VR, social commerce and generative AI.

In regards to the Business

Web – Commerce refers to all financial exercise (B2B, B2C, C2C, DTC) by means of web sites, cellular apps, on-line marketplaces. and social commerce platforms. It subsequently continues to evolve because the applied sciences driving it advance, whether or not on the patron facet or the platform supplier facet that more and more features a mixture of chatbots, AI and social media, in addition to funds and checkout methods, digital advertising and marketing, logistics and success, cross-border commerce, and buyer information/analytics instruments.

Differentiation comes from higher expertise for improved showcasing, vary, simpler navigation and fee, speedier supply and returns, model constructing, comparability procuring, loyalty, and so forth. in addition to good customer support and extra (and free) delivery choices, which typically tip the scales in favor of bigger gamers.

Present Traits Driving the Web-Commerce Business

- ·Macroeconomics and geopolitics don’t favor the trade proper now. The macroeconomic surroundings is making a extra cautious and cost-sensitive backdrop for the trade, shifting it from a high-growth part to 1 centered on effectivity and profitability. Elevated inflation has decreased customers’ actual buying energy, resulting in weaker discretionary spending and a larger give attention to necessities, reductions and value-driven purchases. On the similar time, still-high rates of interest maintain borrowing prices for each customers and corporations elevated, affecting each the manufacturing and consumption sides of the equation. Shopper confidence concerning the present labor market continues to melt and consumption continues to be being pushed largely by inflation. In consequence, there may be continued strain on conversion charges and basket sizes, whereas rising labor, logistics and warehousing prices proceed to squeeze margins. In consequence, corporations are prioritizing value management, automation and higher-margin income streams similar to promoting and subscriptions to maintain profitability in a slower-growth surroundings. Geopolitics is concurrently reshaping the trade by disrupting the worldwide infrastructure that e-commerce depends upon. Commerce tensions, tariffs and regional conflicts are rising the price of items and creating volatility in provide chains, resulting in delays, inventory shortages and better delivery bills. On the similar time, the worldwide buying and selling system is changing into extra fragmented, with corporations shifting towards regional provide chains and “friendshoring” methods to scale back danger, even at the price of effectivity. Regulatory complexity can be rising.

- Competitors is heating up. Ecommerce has raised the bar on what’s an appropriate on-line market. Right now, it’s one that gives low costs, quick or free delivery, hassle-free returns and a seamless omnichannel expertise. Then once more, as a result of it’s so simple to modify platforms, buyer loyalty is tough to pin. Subsequently, gamers more and more discover that mere on-line presence isn’t sufficient. They need to attempt for operational excellence, differentiated buyer experiences, environment friendly logistics and disciplined capital allocation with a purpose to keep in enterprise.

- AI is shaping as much as be one of many main enablers of ecommerceas a result of it transforms e-commerce from a generic market right into a extremely personalized, data-driven ecosystem that reinforces each income progress and profitability. AI permits platforms to make use of buyer information to optimize each step of the procuring expertise. Corporations like Amazon and Shopify leverage AI to ship demand forecasting, focused promoting, dynamic pricing and personalised product suggestions, considerably bettering conversion charges and common order worth. On the operational facet, it helps optimize stock and provide chains, decreasing prices and enabling environment friendly deliveries. The newest improvement right here is agentic commerce the place LLM fashions like ChatGPT suggest merchandise, examine options and full the sale. Even in the event you’re not sure about what to purchase, the assertion of your basic intention could also be sufficient to finish a sale. In consequence, clients get more and more snug with the superior suggestions and personalization it gives. For instance, Adobe estimates that visitors to retail websites from generative AI instruments was up 693.4% 12 months over 12 months within the 2025 vacation season.

- The entire retail expertise between bodily and digital continues to blur as most customers mix their on-line and offline actions. This normally takes the types of analysis on-line and purchase in-store or purchase on-line and choose up in-store. Bodily shops are more and more expertise facilities permitting the standard contact and really feel that many shoppers can’t do with out. Some additionally favor to stroll out with their buy. Subsequently, a strong bodily presence is undoubtedly a optimistic. Additionally, any expertise that will increase the velocity of supply/pickup is most well-liked. This may increasingly entail elevated reliance on robots, self-driven supply autos and drones that might ease bottlenecks and make deliveries smoother and cheaper.

- A number one pattern is Gen-Z popularizing social commerce. Social commerce means the power to find, analysis and full the acquisition of merchandise and experiences on a social media platform. Customers shift from intent-based search to content-driven discovery whereas scrolling by means of quick movies, influencer content material or dwell streams on platforms like TikTok or Instagram.

Zacks Business Rank Signifies Weak spot

The Zacks Web – Commerce trade is a fairly giant group inside the broader Zacks Retail And Wholesale sector. It carries a Zacks Business Rank of #180, which locations it within the backside 27% of 247 Zacks industries.

Our analysis reveals that the highest 50% of the Zacks-ranked industries outperforms the underside 50% by an element of greater than 2 to 1. So the group’s Zacks Business Rank, which is principally the common of the Zacks Rank of all of the member shares, signifies adverse near-term prospects.

Ecommerce being within the backside 50% of Zacks-ranked industries is the results of its relative efficiency versus others. What we’re seeing within the mixture estimate revisions for 2026 is a kind of regular decline till March this 12 months, adopted by slight restoration. The 2027 estimate follows the identical basic pattern however the restoration is considerably sharper.

The previous 12 months has seen the combination earnings estimate for 2026 shrink 6.5%, whereas that for 2027 dropped 1.2% from 2025 actuals. The macroeconomic uncertainty, antagonistic geopolitics, the cautious tone round fee cuts, shopper thrift are contributing to softer spending and thus weaker estimates.

Earlier than we current just a few shares that you could be wish to think about in your portfolio, let’s check out the trade’s latest stock-market efficiency and valuation image.

Business Returns Have Been Reasonable

Over the previous 12 months, the Zacks Digital – Commerce Business has traded comparatively near the broader Retail and Wholesale sector though the S&P 500 pulled forward in November.

The shares on this trade have collectively gained 1.9% over the previous 12 months, in comparison with the two.4% achieve for the broader Zacks Retail and Wholesale Sector and the 24.2% achieve for the S&P 500.

One-12 months Value Efficiency

Picture Supply: Zacks Funding Analysis

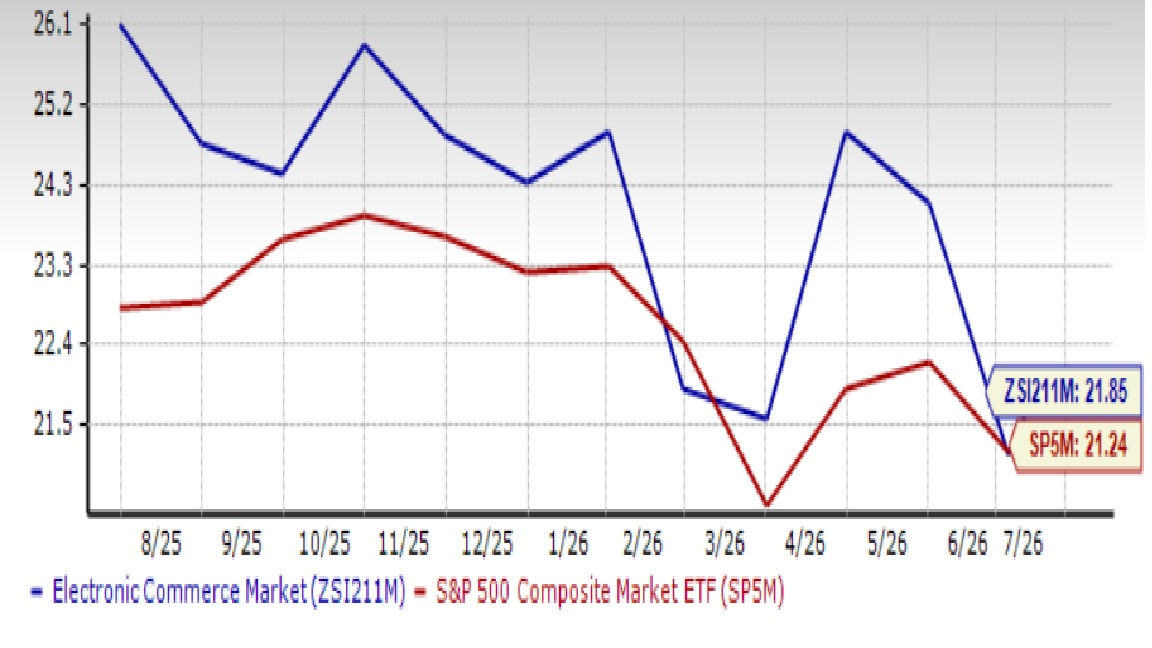

Business Considerably Undervalued

Over the previous 12 months, the trade has principally traded at a premium to the S&P 500 and a reduction to the broader trade. Its present price-to-forward 12 months’ earnings (P/E) of 21.85X represents a premium of two.9% to the S&P 500’s 21.24X, a 5.1% low cost to the broader retail sector’s 22.97X and a ten.3% low cost to its median worth of 24.37X. The shares have traded within the vary of 21.12X to 26.11X over the previous 12 months.

Ahead 12 Month Value-to-Earnings (P/E) Ratio

Picture Supply: Zacks Funding Analysis

2 Shares to Add to Your Portfolio

There’s a vital number of shares on this trade by way of traces of enterprise, enterprise mannequin, location and so forth. That is additionally the explanation that selecting shares particularly within the present surroundings could be tough. We’ve used our proprietary rating system to choose 2 shares that seem engaging as we speak.

Wayfair Inc. (W): Boston, MA-based Wayfair is a web-based retailer of a broad vary of house enchancment merchandise throughout the furnishings, décor, lighting, kitchenware, house enchancment and out of doors classes. It has a big provider community and proprietary logistics infrastructure supporting deliveries throughout the U.S.

Wayfair’s biggest power is within the scale of its choices (over 40 million merchandise from greater than 20,000 suppliers), which together with its investments in its logistics community and expertise platform, allows it to ship distinctive customer support and document share features. Internally, the aim is to maximise EBITDA {dollars} whereas utilizing extra money to handle debt and purchase again shares. The primary-quarter EBITDA margin of 5.2% was the most effective in 5 years, so the plan seems to be on monitor.

A sequence of restructuring actions over the previous couple of years has pushed this enchancment. In the course of the pandemic the corporate had expanded operations, taking in further arms to cope with the surging visitors. Between Aug 2022 and Mar 2025, it reduce over 5000 positions internet of relocations, flattening the organizational construction to hurry up resolution making and scale back value. AI adoption helped get rid of over 300 positions. It additionally exited German operations citing higher prospects within the U.S., Canada, UK and Eire. The outcome was a focus of sources on initiatives that had been prone to yield the best returns.

With a leaner working construction and stronger income progress outlook, Wayfair seems to be poised for continued progress. Current outcomes had been primarily pushed by share features because the housing market to which it’s tied stays sluggish. Whereas it seems that rates of interest won’t come down additional any time quickly, this might be an extra catalyst, as it will deliver mortgage charges down and large-scale house shopping for would return.

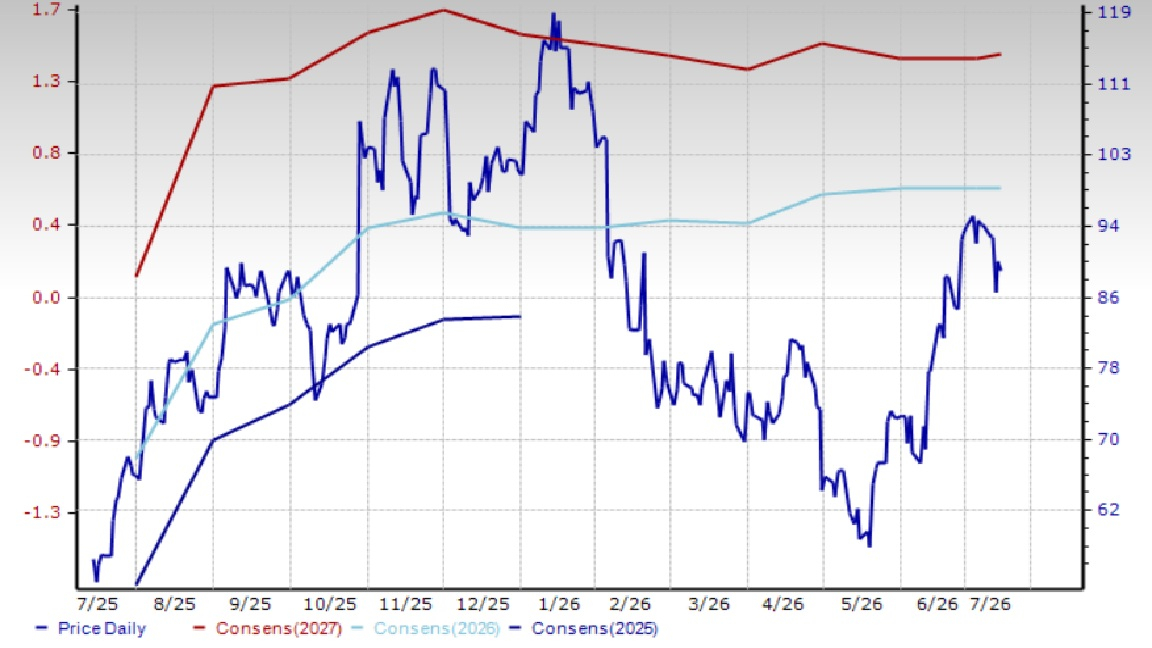

Analysts are clearly optimistic about Wayfair. The corporate definitely has a terrific monitor document of beating estimates, posting optimistic surprises in three of the final 4 quarters, at a median fee of 56.7%. For 2026, analysts anticipate 5.6% income progress and 11.9% earnings progress. For 2027, income and earnings progress are anticipated to be a respective 5.9% and 29.6%. Within the final 30 days, analyst estimates for 2026 and 2027 have elevated 12 cents (4.3%) and a penny (lower than a proportion level).

The shares of this Zacks Rank #1 (Robust Purchase) firm’s shares are up 59.6% over the previous 12 months.

Value & Consensus: W

Picture Supply: Zacks Funding Analysis

Carvana Co. (CVNA): Tempe, AZ-based Carvana, by means of its web site and cellular app, is America’s main on-line market for used automobiles. The complete transaction, from looking stock, financing, and buying automobile safety merchandise and insurance coverage, is accomplished on-line with choices for house supply or choose up at a automotive merchandising machine. Following the acquisition of ADESA’s U.S. public sale enterprise, it additionally operates a nationwide logistics community, in addition to automobile public sale, inspection and reconditioning amenities.

Carvana reported very sturdy quarterly outcomes whereby unit volumes grew 40% (the sixth straight quarter of 40%+ progress) as the corporate continued to take share in a market that was primarily flat within the final quarter. The give attention to its vertically built-in working mannequin and use of expertise to enhance buyer expertise helped it take share. Whereas wholesale costs elevated quickly throughout the quarter, there was the everyday lag in passing these on at retail, which compressed wholesale-to-retail spreads, hurting margins.

The corporate additionally stands to learn from any enchancment within the rate of interest. Decrease rates of interest would deliver extra consumers into the market, and plenty of substitute consumers could be prone to commerce of their autos, including to the used-car provide. Moreover, the used automobile market within the U.S. is way bigger than the brand new automobile market, as used automobiles are less expensive. In consequence, affordability issues are prone to drive a considerable portion of substitute demand towards used autos.

New automobile manufacturing has largely recovered from the pandemic period disruption and new automobile gross sales are anticipated to stay regular going ahead. This, along with continued enchancment in trade-in exercise, ought to progressively replenish the provision of late-model used autos and create a more healthy market for each consumers and sellers.

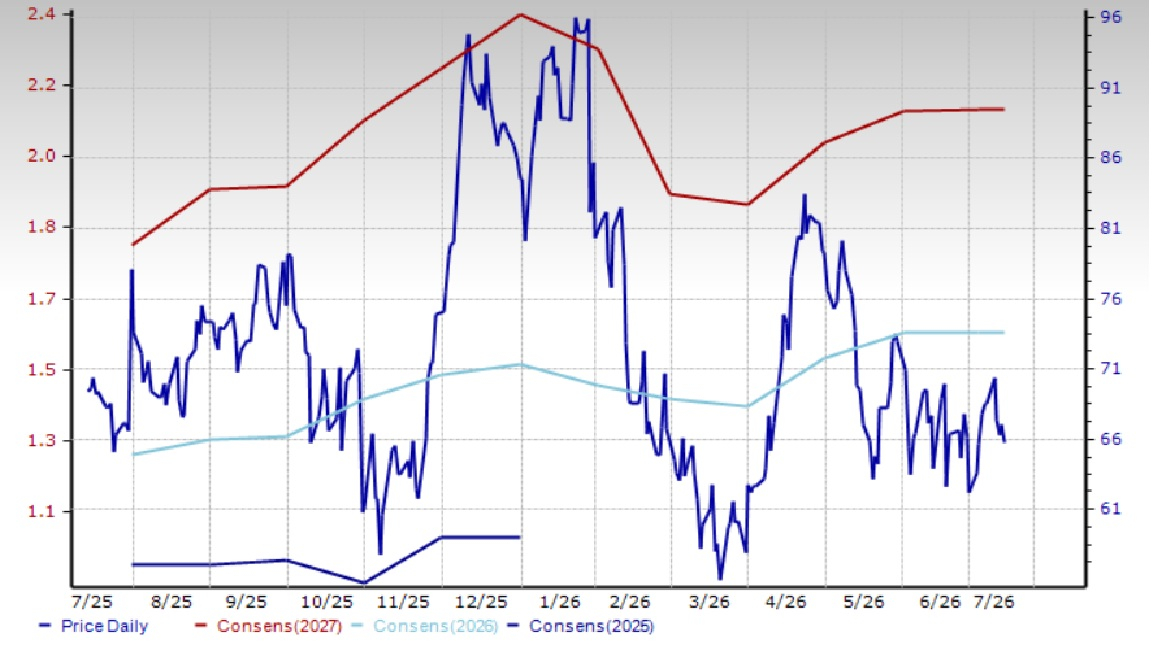

Analysts are optimistic about double-digit income progress each this 12 months and the following though the earnings progress fee is predicted to say no a bit this 12 months. After all, precise progress charges could find yourself greater. Carvana definitely has a very good monitor document of beating estimates: beating estimates in three of the final 4 quarters at a median fee of 71.6%.

For 2026, analysts anticipate 38.5% income progress and -6.5% earnings progress. For 2027, income and earnings progress are anticipated to be a respective 25.7% and 34.5%. Within the final 60 days, analyst estimates for 2026 and 2027 have elevated 5 cents (3.3%) and 4 cents (1.9%), respectively.

The shares of this Zacks Rank #2 firm are down 5.2% over the previous 12 months.

Value & Consensus: CVNA

Picture Supply: Zacks Funding Analysis

Zacks’ Analysis Chief Names “Inventory Most Prone to Double”

Our workforce of consultants has simply launched the 5 shares with the best chance of gaining +100% or extra within the coming months. Of these 5, Director of Analysis Sheraz Mian highlights the one inventory set to climb highest.

This prime choose is a little-known satellite-based communications agency. Area is projected to change into a trillion greenback trade, and this firm’s buyer base is rising quick. Analysts have forecasted a serious income breakout in 2025. After all, all our elite picks aren’t winners however this one might far surpass earlier Zacks’ Shares Set to Double like Hims & Hers Well being, which shot up +209%.

Free: See Our Prime Inventory And 4 Runners Up

Wayfair Inc. (W) : Free Inventory Evaluation Report

Carvana Co. (CVNA) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.