Getty Photographs

Expensive Fellow Shareholders,

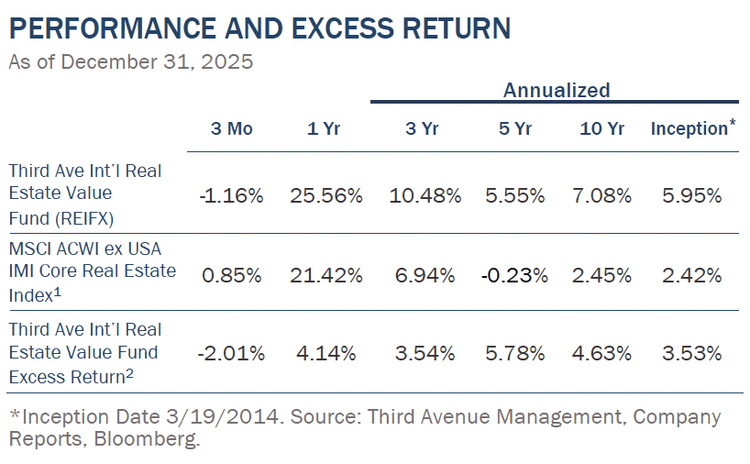

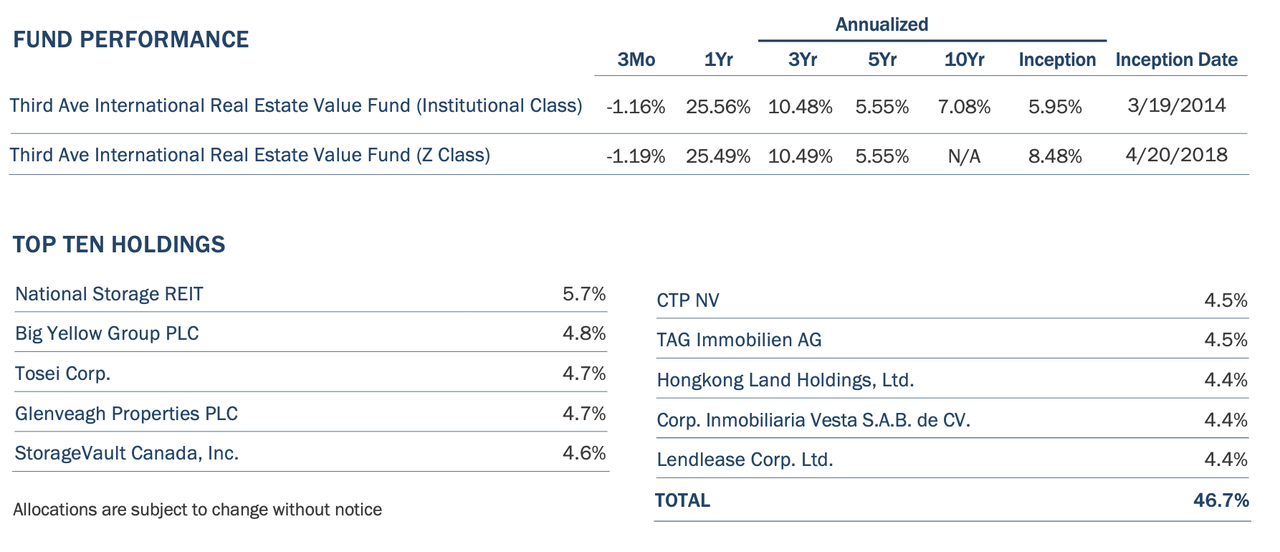

We’re happy to offer you the Third Avenue Worldwide Actual Property Worth Fund (the “Fund”) report for the quarter ended December 31, 2025. The Fund delivered a +25.56% return (after charges) for the calendar 12 months, outperforming the MSCI ACWI ex USA IMI Core Actual Property Index[1], which returned +21.42% over the identical time interval.

The Fund’s complete return for the 12 months was supported by the 13% share worth appreciation for the holdings (in native foreign money), a 4% dividend yield on the underlying holdings, and an 8% tailwind from a weaker U.S. Greenback. On the identical time, lively capital recycling and powerful earnings progress helped preserve the Fund’s ahead price-to-earnings ratio at simply 13 occasions, in addition to a 30% low cost to our conservative estimate of actual property worth as measured by internet asset worth (“NAV”) for the holdings at year-end.

Exercise

On the begin of 2025, Fund Administration highlighted a rising disconnect between the earnings-compounding capability of the Fund’s holdings and the low multiples at which they have been buying and selling. In reality, we famous that, if this disconnect persevered, privatization exercise at significant premiums might speed up.

By 12 months’s finish, this thesis materialized: three holdings entered privatization discussions, with two transactions confirmed. Given the Fund’s low earnings a number of and huge reductions to our conservative estimates of internet asset worth, we anticipate that elevated merger and privatization exercise will proceed within the 12 months forward.

The Fund’s prime performer in 2025 was Mandarin Oriental (MAORF)(MNOIY), which returned +95%. Early within the fourth quarter, its largest shareholder, Jardine Matheson, supplied to denationalise the corporate at a 52% premium to its present share worth. For context, Fund Administration’s 2022 funding thesis anticipated this final result. On the time, Mandarin was finishing a US$2 billion workplace and retail improvement in Hong Kong, the worth of which was anticipated to equal the corporate’s whole market cap and indicate no worth for the substantial resort portfolio and administration platform. Alibaba’s subsequent settlement to accumulate half of the asset triggered a whole privatization of the remaining shares. The transaction additionally highlights the numerous worth inherent in listed Asian actual property firms, in Fund Administration’s opinion.

Two of the Fund’s self-storage holdings additionally entered privatization negotiations throughout the quarter. Such developments align with Third Avenue’s long-held view that valuations in worldwide self-storage stay unreasonably low, regardless of the scalability and structural progress of those platforms—lots of which function 10–20 years behind the extra mature U.S. market.

Of notice, Nationwide Storage (Australia) obtained a privatization supply from Brookfield Asset Administration and the Authorities of Singapore Funding Company (“GIC”) at a 27% premium, per our NAV estimate. The corporate exemplifies attributes frequent throughout many Fund holdings: irreplaceable belongings in high-demand markets, inflation-resistant money flows, a value-accretive working platform, a simple capital construction, and powerful alignment between administration and minority shareholders. But like many investments throughout the Fund, its shares commerce at a steep low cost to intrinsic worth previous to the privatization effort, leading to a pointy uplift alongside the settlement.

Alternatively, Blackstone’s discussions with Massive Yellow (BYLOF) within the U.Ok. didn’t lead to a transaction; nonetheless, we imagine that any future privatization would possible require a premium of ~35% above the present share worth. The founders—who collectively personal greater than £100 million of shares—seem open to a sale on the proper valuation.

Through the quarter, Fund Administration took benefit of share worth volatility to extend publicity to 2 current Fund positions. First, Australian diversified developer and asset supervisor Lendlease Company Ltd. (LLESY) (“Lendlease”), which continues to commerce at round half of our evaluation of its NAV regardless of making important progress on asset gross sales, enterprise simplification, and the growth of its high-quality Australian venture pipeline in a capital-efficient method. Someday this 12 months, Lendlease is more likely to promote sufficient belongings and cut back leverage sufficiently to begin a extremely accretive share buyback, which ought to act as a share worth catalyst. Second, the Fund’s place in German and Polish residential proprietor and developer TAG Immobilien (TAGOF)(TAGYY) (“TAG”). Underpinned by a portfolio of over 83,000 resilient German rental models, TAG continues to broaden into the higher-growth Polish residential market, the place favorable market situations exist. Regardless of now accounting for nearly half of TAG’s earnings, the Polish publicity stays considerably underappreciated on the present share worth. Ongoing favorable fundamentals ought to act as a catalyst for TAG shares over time.

Positioning

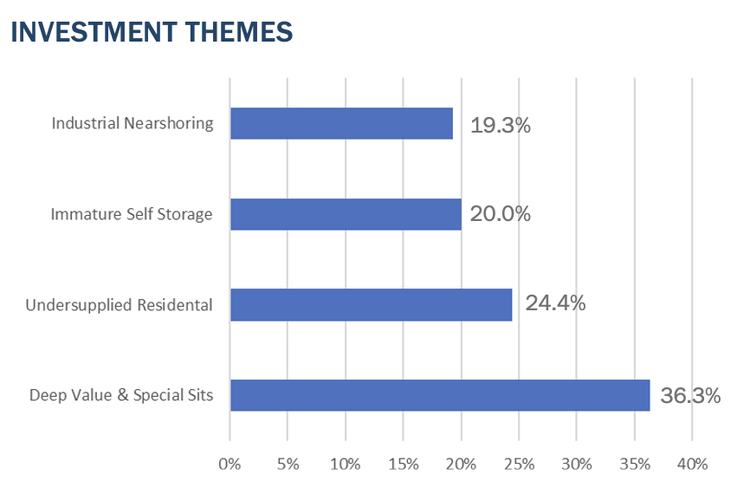

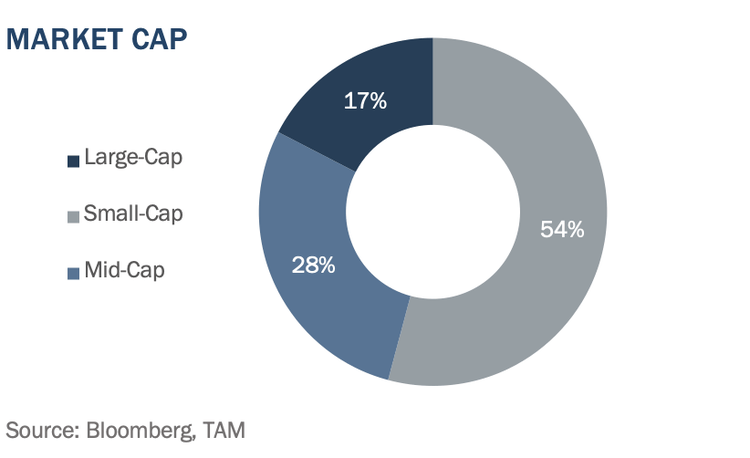

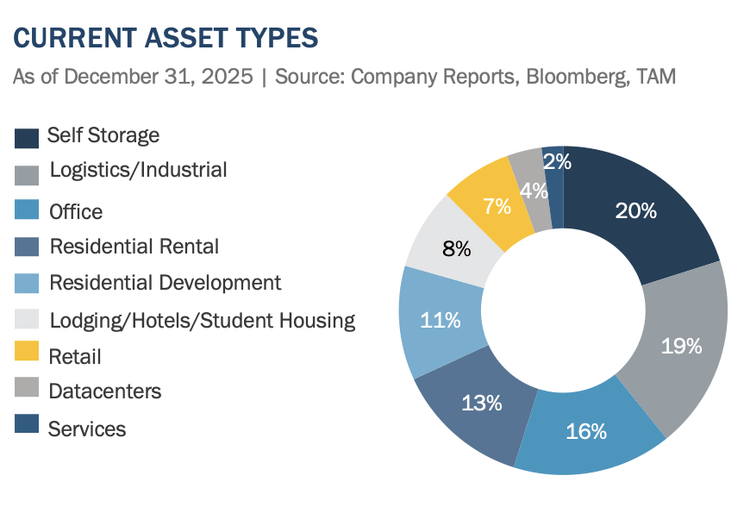

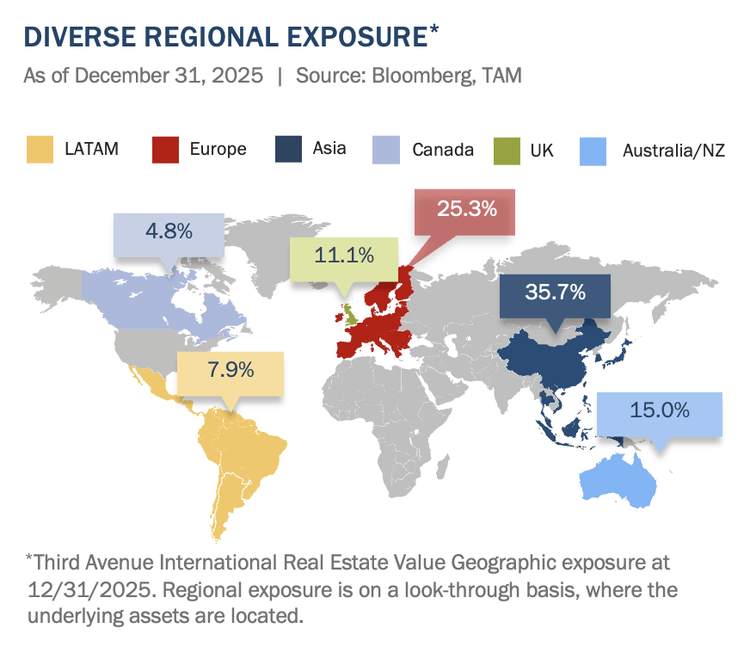

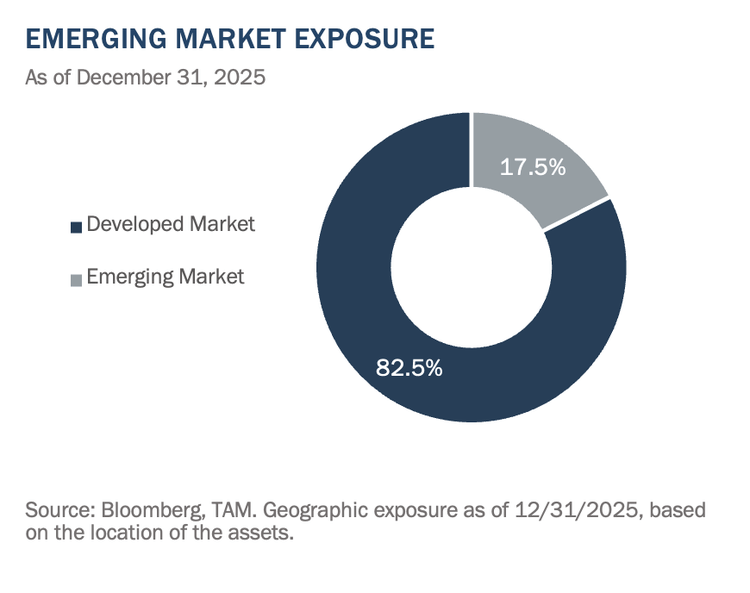

Together with the above-referenced exercise, the allocations for the Third Avenue Worldwide Actual Property Worth Fund stay broadly per latest quarters. That’s to say, the Fund’s publicity continues to emphasise investments in (i) deep worth and particular conditions, (ii) undersupplied residential markets, (iii) self-storage platforms with lengthy runways for progress, (iv) mid-cap firms with specialised, non-traditional actual property belongings, and (v) diversified geographic publicity as highlighted within the following charts.

Outlook Commentary

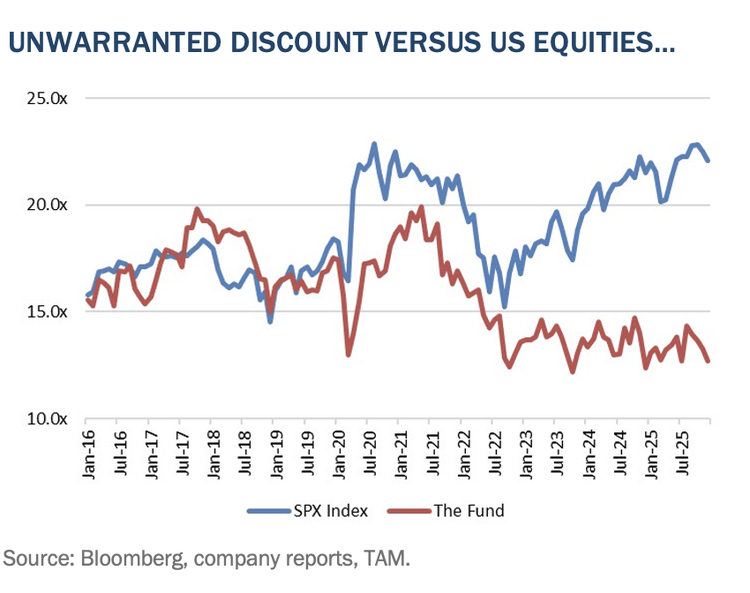

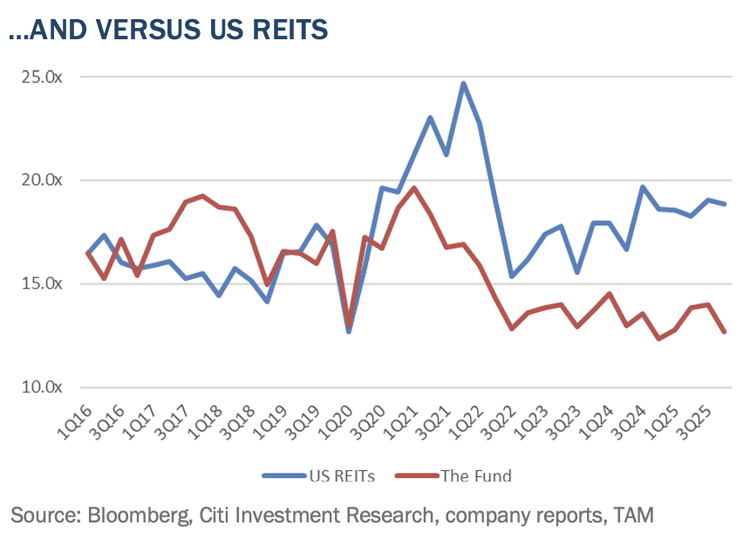

Regardless of a powerful 2025, Fund Administration stays constructive about 2026. Valuation stays a key benefit, in our view, with the price-to-earnings ratio for the Fund’s holdings at 13 occasions (within the combination) when in comparison with 22 occasions for the S&P 500—the widest relative low cost in a decade, as proven under.

The Fund’s low a number of is especially compelling given its earnings progress potential. Not solely that, however the Fund’s holdings additionally commerce at a significant low cost to the U.S. REIT sector regardless of expectations for increased earnings progress within the 12 months forward.

With that being the case, it appears possible that a number of macro elements might assist a number of growth, together with (i) a regime shift in world capital flows towards worldwide markets and tangible belongings, (ii) continued U.S. Greenback weak spot, which instantly advantages Fund returns and improves liquidity (and the price of capital) internationally, and (iii) potential rate of interest cuts, which have traditionally supported actual property valuations and led to fund flows into listed property securities.

Even when valuation reductions persist and multiples stay secure, the setup of NAV progress, earnings growth, and sturdy earnings yield can generate enticing complete returns, in Fund Administration’s view, with an earnings yield of shut to eight% and the potential for top single-digit earnings progress. On this regard, the Fund’s underlying investments goal these select-pockets with idiosyncratic drivers of worth from ongoing operations, together with (i) bettering fundamentals in Hong Kong, the place rising capital formation is supporting residential, retail, and workplace markets, (ii) severely undersupplied housing markets in Sydney, Dublin, Melbourne, and Poland, which ought to see rising rents, residence costs, and transaction volumes, (iii) self-storage demand progress, supported by rising housing exercise and normalizing expense traits, and (iv) industrial energy in Mexico, Central and Jap Europe, Thailand, and Vietnam, pushed by provide chain diversification away from concentrated Chinese language manufacturing.

Moreover, the Fund’s investments usually contain important ‘useful resource conversion’ alternatives, the place an organization creates worth not by way of its ongoing operations however by restructuring belongings, liabilities, or possession to unlock hidden or latent worth. These investments embrace (i) a number of Asia-Pacific firms targeted on strategic initiatives like promoting non-core belongings, simplifying operations, and utilizing proceeds to purchase again shares at reductions, (ii) companies finishing massive improvement pipelines, similar to datacenter tasks in Spain and Hong Kong, that may notably enhance money move, and (iii) publicity to Japanese property companies that actively improve worth and commerce belongings to appreciate their value.

In the end, useful resource conversion could contain absolutely privatizing an actual property firm, as seen this quarter with Mandarin and Nationwide Storage. Fund Administration maintains the view that if the general public markets don’t acknowledge the worth of listed actual property internationally by way of elevated share costs, the personal markets will accomplish that by way of privatization at important premiums.

With a compelling mixture of sector-level tailwinds and company-specific catalysts, Fund Administration stays extremely optimistic in regards to the Fund’s future. We additionally deeply recognize your continued belief and assist. Please attain out at realestate@thirdave.com with any questions, feedback, or concepts. In any other case, we look ahead to updating you once more subsequent quarter.

Sincerely, The Third Avenue Actual Property Worth Staff

Quentin Velleley, CFA Portfolio Supervisor

Editor’s Notice: The abstract bullets for this text have been chosen by In search of Alpha editors.