Alphabet GOOGL shares had been already star performers earlier than the corporate’s Q1 earnings launch on Wednesday, making a few of us anxious that the inventory is likely to be priced for perfection. However they actually hit it out of the park, with spectacular momentum not simply within the cloud enterprise but additionally search, subscriptions, and backlog.

With Alphabet administration greater than answering the AI monetization query by means of these file outcomes, the market didn’t lose a beat over additional will increase in capital expenditures. The corporate expects to spend within the $180 billion to $190 billion vary now, up from the earlier guided vary of $175 billion to $185 billion.

Amazon’s Q1 outcomes weren’t Alphabet-good, however they had been however very sturdy, with cloud revenues exhibiting clear acceleration and rising at their quickest tempo since 2022 at +28%. The expansion tempo is predicted to choose up additional in Q2 and past, given new offers with Meta META, Anthropic, and OpenAI.

Amazon’s 2026 Q1 cloud income development of +28% follows development charges of +24% and +20% in 2025 This fall and Q3, respectively. Alphabet’s cloud income development was in a league of its personal, up +63%, which follows development charges of +48% in 2025 This fall and an estimated +35% to +40% in 2025 Q3. Not like Alphabet and Amazon, Microsoft MSFT disenchanted as soon as once more, developing quick in its outcomes and commentary for the third quarter in a row.

The one purpose why somebody would discover fault with Microsoft’s +29% cloud income development is that the corporate’s development tempo in every of the previous two quarters was in a comparable vary. Microsoft has lengthy famous capability points weighing on its cloud development, which appears believable since Alphabet additionally famous this challenge.

Microsoft shares have been true laggards within the Magazine 7 group, down -14.5% this yr vs. Alphabet’s +23.1% rise and the S&P 500 index’s +6.2% achieve. The corporate has been swept up within the software program turmoil, so the difficulty isn’t the stalled cloud unit. Microsoft had additionally banked closely on OpenAI for its LLM, and that relationship has unraveled ‘bigly’. It’s affordable to count on that they’ll finally get there, in spite of everything, they’ve the sources and other people, however it’s going to probably take them some time.

At this stage within the Q1 reporting cycle, Nvidia NVDA is the one Magazine 7 member that has but to report March-quarter outcomes. Nvidia is scheduled to report Q1 outcomes on Could 20th, with EPS and revenues for the interval anticipated to be up +118.5% and +78.7% from the identical interval final yr, respectively.

Combining the precise outcomes for the 6 Magnificent 7 members which have reported already with estimates for Nvidia, whole Q1 earnings for the group are anticipated to be up +45.7% from the identical interval final yr on +24.6% increased revenues, which might observe the group’s +26.1% earnings development on +19.4% income development in 2025 This fall.

The chart under exhibits the group’s blended Q1 earnings and income development relative to the previous interval and the anticipated development over the following three durations.

Picture Supply: Zacks Funding Analysis

The chart under exhibits the Magazine 7 group’s earnings and income development image on an annual foundation.

Picture Supply: Zacks Funding Analysis

Please observe that the Magazine 7 group is on observe to herald 26.2% of all S&P 500 earnings in 2026 and account for 34.1% of the index’s market capitalization.

The Magazine 7 group has been having fun with a steadily bettering earnings outlook, with analysts elevating their estimates. We noticed that pattern in play forward of the beginning of the Q1 earnings season, and one thing related is in place for 2026 Q1 as effectively.

The chart under exhibits how combination earnings estimates for the Magazine 7 group have developed since July 2025.

Picture Supply: Zacks Funding Analysis

2026 Q1 Earnings Season Scorecard

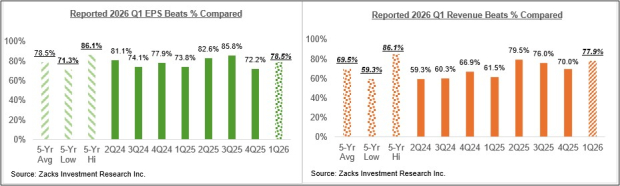

By Friday, Could 1st, now we have seen Q1 outcomes from 317 S&P 500 members or 63.4% of the index’s whole membership. Whole earnings for these 317 index members are up +23.4% from the identical interval final yr on +11.1% increased revenues, with 78.5% beating EPS estimates and 77.9% beating income estimates.

We’ve one other very busy week on the reporting entrance, with greater than 1400 corporations reporting outcomes, together with 127 S&P 500 members. We’ve a great mix of notable ‘new age’ tech gamers like Palantir, Uber, Airbnb, DoorDash, and Pinterest, and ‘legacy blue chip’ operators like McDonald’s, Disney, and DuPont on deck to report outcomes this week.

The comparability charts under put the expansion charges for the businesses which have reported with what we had seen from this identical group of corporations in different latest durations.

Picture Supply: Zacks Funding Analysis

The comparability charts under put the Q1 EPS and income beats percentages for this group of corporations relative to what we had seen from them in different latest durations.

Picture Supply: Zacks Funding Analysis

The chart under exhibits how web margins for the 317 index members which have reported Q1 outcomes examine to different latest durations for this identical group of corporations.

Picture Supply: Zacks Funding Analysis

For an in depth have a look at the general earnings image, together with expectations for the approaching durations, please try our weekly Earnings Traits report >>>>A Robust & Steadily Bettering Earnings Image

Past Nvidia: AI’s Second Wave Is Right here

The AI revolution has already minted millionaires. However the shares everybody is aware of about aren’t more likely to maintain delivering the largest earnings. Little-known AI companies tackling the world’s greatest issues could also be extra profitable within the coming months and years.

Microsoft Company (MSFT) : Free Inventory Evaluation Report

NVIDIA Company (NVDA) : Free Inventory Evaluation Report

Alphabet Inc. (GOOGL) : Free Inventory Evaluation Report

Meta Platforms, Inc. (META) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.