syahrir maulana/iStock by way of Getty Pictures

Pricey Companions,

The primary quarter of 2026 gave buyers lots to fret about. Rising tensions within the Center East pushed oil costs larger, inflation issues resurfaced, and the long-anticipated pivot to decrease rates of interest continues to be postponed. Markets, by no means quick on creativeness, have begun spinning acquainted narratives: that costly cash punishes development, that AI’s guarantees might exceed its near-term returns, and that the safer wager lies in power, cyclicals, and companies whose money flows arrive sooner relatively than later. There may be additionally a rising concern that AI itself might disrupt complete classes of present software program companies — rendering yesterday’s winners out of date in a single day.

We is not going to fake these issues are frivolous. They aren’t. When the price of capital rises, the arithmetic of investing genuinely modifications — a greenback earned a decade from now’s price much less at this time than it was in a world of low cost cash. That’s not opinion; it’s math. And we’ve at all times believed in taking math critically.

However here’s what we’ve additionally discovered, after watching markets swing from greed to panic throughout many cycles: the headlines that really feel most pressing are not often those that decide long-term outcomes. The companies that compound wealth over a long time accomplish that not as a result of they have been spared from troublesome environments, however as a result of they have been constructed to endure them. We have now spent the previous decade constructing a portfolio of precisely that sort.

None of what we’re seeing at this time is new. Completely different costumes, similar play.

Efficiency in Context

In the course of the first quarter, Rowan Avenue declined 19.8%, in comparison with a 4.3% decline for the S&P 500. That’s not a outcome we get pleasure from reporting. On the similar time, it displays the extra concentrated strategy we take and isn’t uncommon for portfolios constructed round a smaller variety of high-conviction investments.

We spend money on a targeted group of companies that we imagine can compound worth at enticing charges over lengthy durations of time. Within the quick time period, their inventory costs might be extra unstable—significantly in environments just like the one we’re experiencing at this time, the place rates of interest are larger and investor focus has shifted towards companies with nearer-term money flows.

Rowan Avenue is designed for long-term compounding, not for minimizing short-term volatility or intently monitoring a benchmark. Because of this, returns can differ meaningfully from 12 months to 12 months.

We have now seen this earlier than.

In early 2022, we went by an identical interval the place inventory costs declined sharply, even because the underlying companies continued to carry out effectively. On the time, we wrote that the portfolio was, in some ways, in one of many strongest positions in our historical past regardless of the decline in inventory costs.

That didn’t really feel apparent on the time. What adopted was a interval the place enterprise efficiency in the end reasserted itself. The fund returned +102.6% (internet) in 2023, +56.6% in 2024, and +11.1% in 2025.

As Benjamin Graham noticed:

“Within the quick run, the market is a voting machine, however in the long term, it’s a weighing balance.”

A Put up-Quarter Replace

We’re penning this letter in mid-April, roughly two weeks after quarter-end. Since March 31, markets have moved sharply — and our portfolio has recovered roughly half of the primary quarter decline. Based mostly on our inside estimates as of April 17, year-to-date efficiency stands at roughly -10%, in comparison with the official quarter-end determine of -19.8%. We word that this mid-month determine is an inside estimate solely, has not been verified by our fund administrator, and displays solely a partial month.

We share this to not recommend the troublesome interval is behind us — it might not be. We share it as a result of it illustrates exactly the purpose we’re making all through this letter. The basics of the companies we personal haven’t modified. Their aggressive positions, earnings energy, and long-term prospects stay intact, in our view. What modified was the value a number of. That is what long-term possession of remarkable companies really seems like. Value and worth diverge. Typically dramatically. The buyers who profit are these with the temperament to stay targeted on the underlying companies, not the day-to-day actions of their inventory costs.

Volatility is the Value of Admission

The desk under reveals the annual returns of our largest holdings by portfolio weight as of March 31, 2026 and illustrates a easy actuality of long-term investing: even distinctive companies expertise vital volatility. We have now included an April 17 column to mirror the significant restoration in our portfolio since quarter-end, as mentioned within the Efficiency part above. The figures mirror annual inventory worth returns and don’t symbolize Rowan Avenue Capital fund efficiency or returns achieved by the fund on these positions.

The April 17 column tells its personal story — and it’s the similar story this letter is constructed round. That is what long-term possession really seems like in apply. Not a clean upward line — however a recurring collection of positive factors, losses, and exams of conviction. Drawdowns of 30%, 50%, even 75% usually are not uncommon. They’re a recurring function of proudly owning distinctive companies — not anomalies.

Everybody describes themselves as a long-term investor. Only a few are keen to endure what that really seems like. Volatility is the value of admission.

The charts that observe carry this sample to life throughout three of our largest holdings — Meta Platforms, Tesla, and Shopify. Completely different companies, totally different drawdowns, similar lesson.

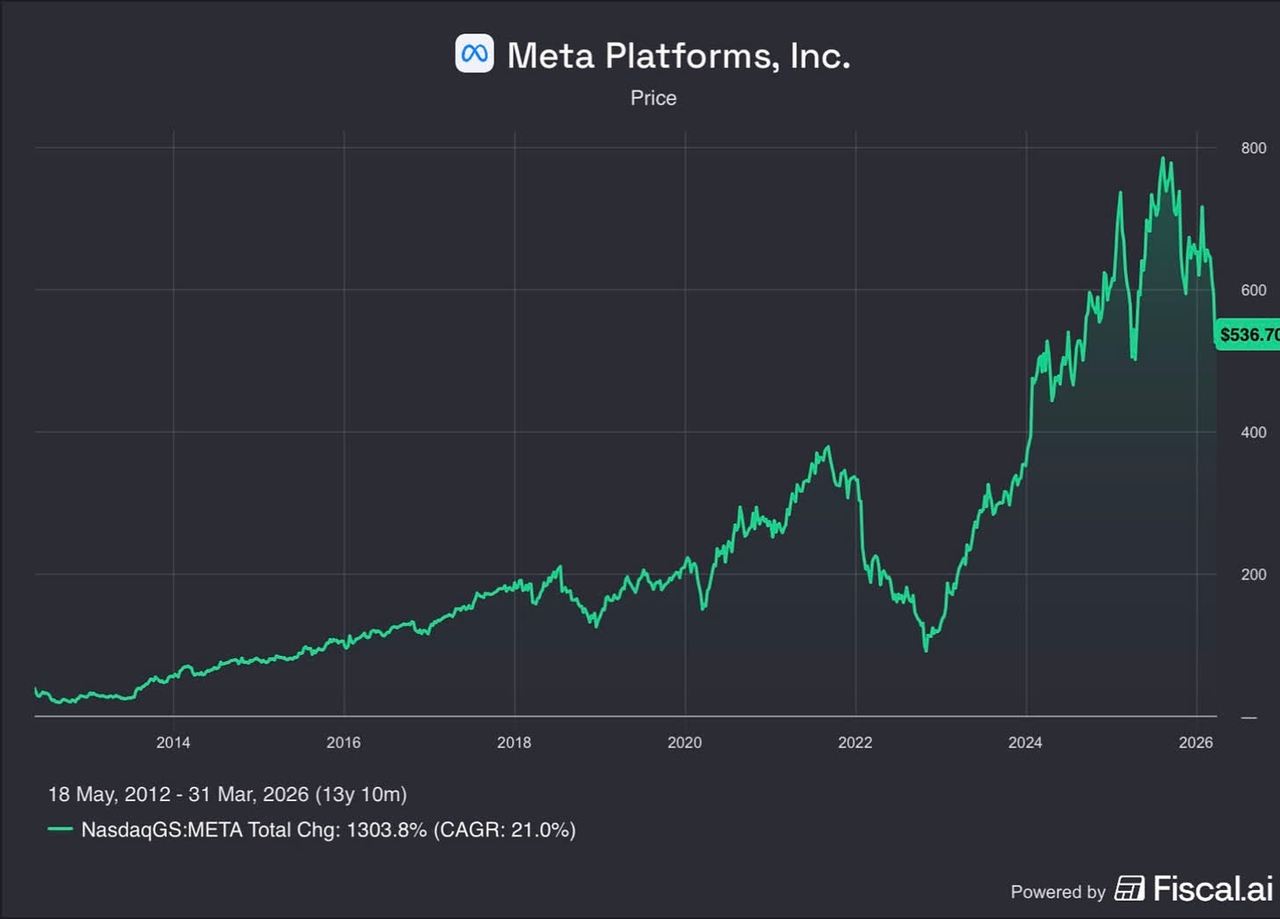

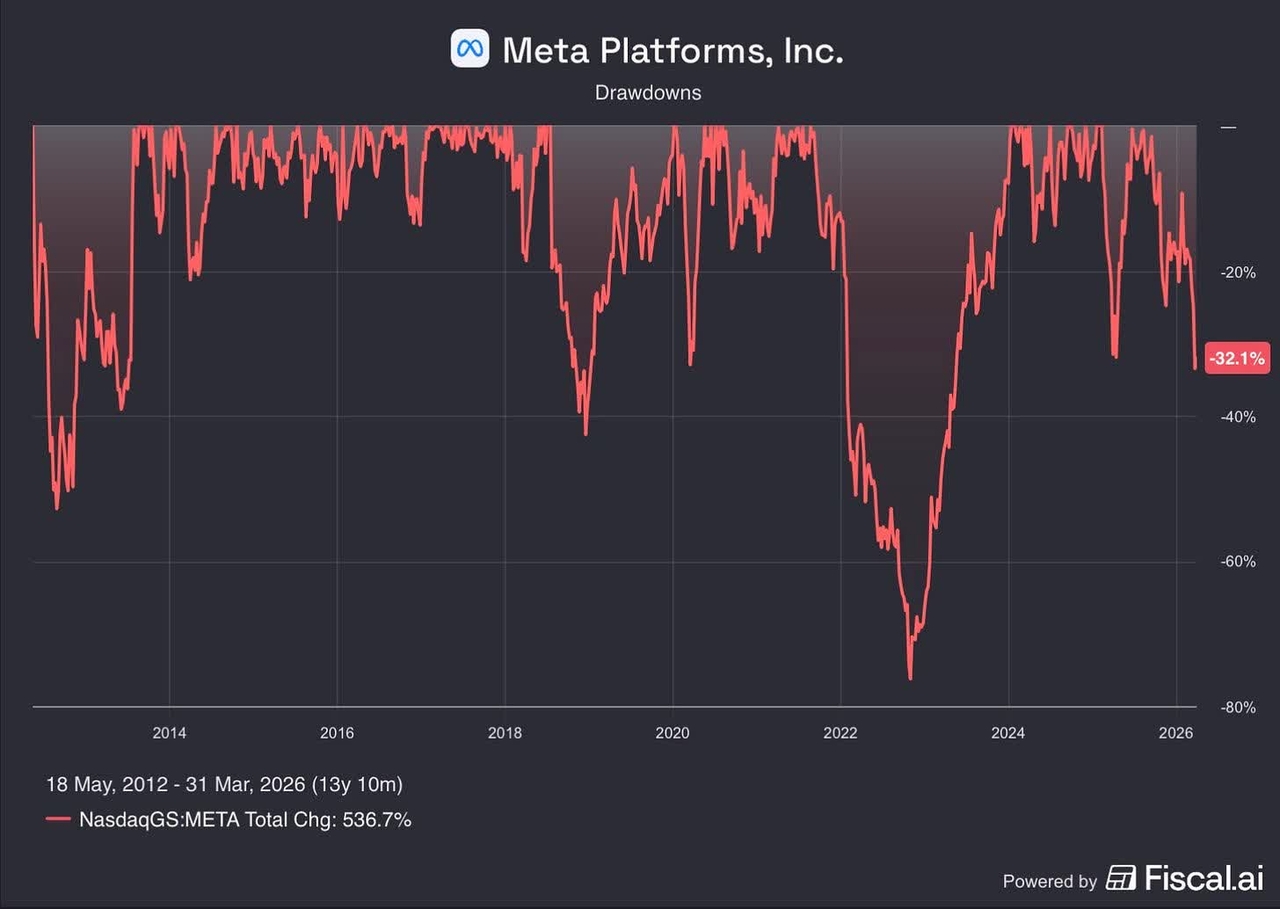

Meta Platforms (META)

Meta has delivered a cumulative return of roughly 1,300% since its IPO, or about 21% yearly. The trail to these returns, nevertheless, has been something however clean.

Over the previous decade, the inventory has skilled quite a few drawdowns of 30% or extra, a number of declines of fifty% or extra, and, most notably, a decline of practically 80% in 2022.

These durations weren’t remoted occasions — they have been a recurring function of proudly owning this enterprise. And but for many who remained targeted on the underlying fundamentals, the long-term final result has been distinctive.

We imagine at this time represents probably the most compelling alternatives in Meta we’ve seen since 2022. Please learn our full evaluation under — together with our views on the AI spending debate, the current authorized setbacks, and why we imagine the market could also be repeating a well-known mistake.

Tesla (TSLA)

Tesla gives an much more putting instance—not simply of volatility, however of how disproportionate long-term outcomes might be relative to the expertise alongside the way in which.

Since its IPO in 2010, the inventory has delivered a cumulative return of roughly 22,000%, or about 41% yearly. that outcome at this time, the trail can seem nearly inevitable. In actuality, it was something however.

There have been a number of durations alongside the way in which the place the inventory declined sharply—on quite a few events by greater than 50%, and as soon as by over 70%—usually accompanied by shifting narratives across the enterprise. At totally different factors, the issues ranged from questions concerning the firm’s survival, to valuation, to rising competitors, founder conduct and execution threat.

Every of these moments felt unsure in actual time. And but, for buyers who have been in a position to stay targeted on the long-term trajectory of the enterprise, the end result has been extraordinary.

The most important winners not often really feel snug to personal.

Whereas Tesla has demonstrated this sample over a few years, our possession of the enterprise continues to be comparatively current.

We outlined our funding thesis intimately in our Q3 2025 letter, and our view stays unchanged. From right here, our function is to not predict short-term actions, however to stay disciplined and permit the long-term economics of the enterprise to play out.

Shopify (SHOP)

Shopify has been an distinctive enterprise over time, compounding at over 40% yearly since its IPO.

The trail to these returns, nevertheless, has been removed from clean, together with a number of sharp drawdowns and a decline of greater than 80% in 2022.

We skilled this firsthand. After initiating our place in early 2022, the inventory declined by a further ~50%. We believed the drawdown mirrored a number of compression, not elementary deterioration. The enterprise continued to develop revenues, develop its service provider ecosystem, and strengthen its aggressive place. The value was damaged. The corporate was not.

It didn’t really feel good. The perfect alternatives not often do.

What adopted was an extended and uncomfortable interval of endurance earlier than payoff. The inventory rebounded 124% in 2023 — and but we have been nonetheless underwater on our funding. It was not till 2024 — when Shopify generated over $1 billion in working revenue for the primary time and the inventory gained one other 37% — that we lastly obtained our capital again and started producing actual returns. The inventory then rose 51% in 2025, making it our greatest performer of the 12 months.

Three years of endurance. Three years of watching the enterprise execute whereas the inventory examined our conviction repeatedly.

Extra not too long ago the inventory has once more declined meaningfully — down 26% at quarter-end, although it has since recovered to roughly -17% as of mid-April. There may be nothing uncommon about that. It’s the similar sample, taking part in out once more.

Shopify is a transparent instance of why endurance — particularly by durations of valuation compression — is usually required earlier than fundamentals are totally mirrored in inventory costs. In our expertise, the returns in companies like Shopify are earned by these keen to endure durations when inventory costs and enterprise efficiency briefly transfer in reverse instructions.

Underlying Enterprise Efficiency

Regardless of the current decline in inventory costs, the underlying companies we personal proceed to carry out effectively. Based mostly on present estimates, our portfolio firms are anticipated to develop revenues at roughly 18% yearly and earnings at roughly 21% yearly over the following a number of years. These figures symbolize a weighted common throughout a bunch of companies working in several industries and geographies.

In our expertise, durations like this — when worth and worth diverge — have persistently offered essentially the most enticing funding alternatives.

In our Q2 2025 letter, we wrote that our edge doesn’t come from predicting short-term market actions, however from our willingness to personal a concentrated group of high-quality companies and stay targeted on their long-term compounding potential.

That precept is way simpler to articulate when markets are rising than when they’re declining. Intervals just like the one we’re experiencing at this time are when that self-discipline is examined — and, in our view, when it issues most.

Portfolio Replace: Constellation Software program

In the course of the quarter, we initiated a place in Constellation Software program (TSE: CSU) (CNSWF), funded by the sale of the rest of our Spotify place. Constellation is without doubt one of the most distinctive capital allocation platforms within the public markets — an organization that has compounded shareholder capital at roughly 28% yearly since its 2006 IPO by systematically buying and working mission-critical vertical market software program companies. The inventory has not too long ago declined roughly 50% from its highs, creating what we imagine is a uncommon entry level right into a enterprise of this high quality. For these desirous about an in depth dialogue of our funding thesis — together with our views on the AI disruption narrative and the current management transition — we’ve revealed a full write-up on our Substack.

The Alternative As we speak

We need to be direct with our companions and with anybody contemplating investing alongside us for the primary time.

We have now been right here earlier than — not simply as observers, however as contributors with actual stakes. In 2021-2022, when our portfolio declined sharply we remained targeted on the underlying companies and their long-term prospects. We wrote on the time that we believed the portfolio was in one of many strongest positions in its historical past. Few wished to listen to it. Even fewer wished to speculate. What adopted was a cumulative internet return of roughly +252% over the next three-year interval (2023–2025).

We aren’t promising a repeat. No trustworthy investor could make that declare.

However here’s what we are able to say with conviction: the companies we personal at this time are stronger than they have been in 2022. Their aggressive positions are deeper, their earnings energy is larger, and their long-term alternatives are bigger. In some ways, we imagine that is the strongest and most targeted portfolio we’ve constructed since our inception in 2015 — a small group of remarkable companies which have every been examined by adversity and emerged with their aggressive positions intact or strengthened.

And but their inventory costs have declined meaningfully from current highs. In our view, the hole between what these companies are price and what the market is keen to pay for them at this time is as vast because it has been since that interval.

We have now invested a major majority of our private internet price alongside yours. We earn nothing except our companions earn money. That’s not a advertising and marketing line — it’s the construction we selected intentionally on day one, as a result of we imagine it’s the solely trustworthy strategy to handle different individuals’s capital.

Intervals like this are by no means snug. They weren’t snug in 2022, and they don’t seem to be snug at this time. However in our eleven years of managing capital by euphoria and despair, one lesson has confirmed itself repeatedly: it’s exactly in these moments — when costs are low, sentiment is poor, and endurance feels unrewarded — that crucial long-term returns are made.

To our present companions — thanks in your continued belief and endurance. We have now been right here earlier than, and we stay as convicted as ever within the companies we personal collectively. In case your circumstances enable, we imagine including to your funding at present ranges represents one of many extra compelling alternatives we’ve seen since 2022.

To these contemplating investing alongside us for the primary time — if this mind-set resonates with you, we’d welcome the chance to companion over the long run.

Greatest regards,

Alex and Joe

Editor’s Observe: The abstract bullets for this text have been chosen by Searching for Alpha editors.