PVH Company PVH posted third-quarter fiscal 2025 outcomes, whereby each revenues and earnings topped the Zacks Consensus Estimate. Nonetheless, the underside line fell 12 months over 12 months, whereas the highest line elevated.

PVH delivered a strong third quarter, surpassing steering on reported revenues, working margin and EPS, with constant-currency revenues matching expectations. Outcomes mirrored disciplined execution of the PVH+ Plan and sustained model power throughout Calvin Klein and Tommy Hilfiger, supported by stepped-up product innovation and impactful world advertising initiatives.

Administration reaffirmed its full-year constant-currency income and margin outlook and narrowed projections for reported revenues and non-GAAP EPS towards the excessive finish of prior ranges, signaling confidence in its model momentum and ongoing cost-efficiency positive factors. Notably, PVH continues to learn from SG&A financial savings unlocked by way of its multi-year Progress Driver 5 program.

Trying forward, PVH is concentrated on accelerating innovation inside core product classes, increasing globally resonant advertising campaigns and enhancing market execution throughout key areas. These initiatives, coupled with a strengthened demand-driven provide chain, are anticipated to bolster model relevance by way of the again half of 2025 and help the corporate’s long-term strategic development framework.

Delving Deeper Into PVH’s Q3 Efficiency

PVH Corp reported adjusted earnings of $2.83 per share, down 6.6% from the year-ago quarter’s $3.03. Nonetheless, the underside line surpassed the Zacks Consensus Estimate of earnings of $2.56 per share and the corporate’s steering of $2.35-$2.50.

PVH Corp. Worth, Consensus and EPS Shock

PVH Corp. price-consensus-eps-surprise-chart | PVH Corp. Quote

Revenues jumped 2% 12 months over 12 months (down 1% at fixed forex) to $2.29 billion and beat the consensus mark of $2.26 billion.

Direct-to-consumer revenues had been flat in contrast with the prior-year interval’s figures (down 1% on a constant-currency foundation). Revenues in PVH Corp’s owned and operated additionally delivered flat development, although revenues declined 2% in fixed forex, as positive factors in APAC had been outweighed by softer ends in the Americas and EMEA. In the meantime, owned and operated digital commerce grew 1%, and was flat in fixed forex, with will increase within the Americas and APAC offset by declines in EMEA.

Wholesale revenues climbed 4% from the prior-year interval (up 1% on a constant-currency foundation), buoyed by development within the Americas, partially offset by decreases in EMEA and APAC.

PVH Corp’s Prices & Margin Particulars

The corporate’s gross revenue of $1.29 billion dipped 1.81% 12 months over 12 months. The gross margin contracted 210 foundation factors to 56.3% as a result of larger U.S. tariffs, elevated promotional atmosphere, margin strain from bringing beforehand licensed ladies’s classes in-house and elevated freight prices, together with added reductions tied to Calvin Klein supply delays.

Adjusted promoting, normal and administrative bills had been $1.09 billion, up 0.8% 12 months over 12 months. The corporate’s adjusted earnings earlier than curiosity and taxes totaled $202.3 million, down 14.5% from the prior-year quarter.

PVH’s Segmental Evaluation

EMEA revenues elevated 4% 12 months over 12 months to $1.11 billion. Nonetheless, on a constant-currency foundation, revenues declined 2% on account of softness in each the direct-to-consumer and wholesale companies. The consensus estimate for EMEA revenues was pegged at $1.09 billion.

Americas revenues rose 2% 12 months over 12 months to $682.8 million, pushed by development within the wholesale enterprise, considerably offset by a decline within the direct-to-consumer enterprise. Wholesale positive factors mirrored the shift of beforehand licensed ladies’s classes in-house, although this was partially offset by final 12 months’s wholesale shipments being extra concentrated within the again half of the 12 months. The consensus estimate for Americas revenues was pegged at $676 million.

APAC revenues decreased 1% 12 months over 12 months to $391.9 million (flat on a constant-currency foundation). In fixed forex, direct-to-consumer development was totally offset by a decline within the wholesale enterprise. The consensus estimate for APAC revenues was pegged at $383 million.

Licensing revenues fell 11% 12 months over 12 months as a result of transition of some beforehand licensed ladies’s product classes in-house.

PVH Corp’s Model Efficiency

Revenues for the Calvin Klein section elevated 2% 12 months over 12 months (flat on a constant-currency foundation).

Revenues for the Tommy Hilfiger model rose 1% 12 months over 12 months (down 2% on a constant-currency foundation).

The Heritage Manufacturers section’s revenues fell 3.1% 12 months over 12 months.

Nearer Have a look at PVH’s Monetary Efficiency

PVH Corp ended the fiscal third quarter with money and money equivalents of $158.2 million, long-term debt of $2.25 billion and stockholders’ fairness of $4.87 billion. Inventories had been up 3% 12 months over 12 months, marking a significant enchancment versus the rise seen within the second quarter of 2025. The present improve additionally features a 2% impression from larger tariffs.

As a part of its plan to return further money to shareholders, the corporate purchased again 5.4 million shares for $561 million within the first quarter utilizing accelerated share repurchase (ASR) applications and open-market purchases. Within the third quarter, these ASR applications had been finalized, and the corporate obtained one other 2.3 million shares. Altogether, PVH repurchased 7.7 million shares within the first 9 months of 2025. The corporate didn’t spend any cash on share buybacks within the second or third quarters.

What to Anticipate From PVH Corp in This autumn & FY25?

For the fiscal fourth quarter, revenues are anticipated to rise modestly, reaching low single-digit development in comparison with the fourth quarter of 2024, although will probably be barely decrease on a constant-currency foundation.

Adjusted earnings per share are anticipated to be $3.20-$3.35 in contrast with the $3.27 earned within the year-ago quarter. This EPS outlook displays an estimated internet destructive impression from present U.S. tariffs, together with an unmitigated impression of roughly $0.60, partially offset by deliberate mitigation actions, in addition to an estimated optimistic impression of about $0.20 from overseas forex translation.

Curiosity bills are projected to extend to $20 million from the $14 million reported within the fourth quarter of fiscal 2024 as a result of impacts of funding the accelerated share repurchase agreements. The adjusted efficient tax price is projected to be 22%.

For fiscal 2025, PVH is narrowing its income outlook to low single-digit development, reaffirming expectations for flat to barely larger revenues on a constant-currency foundation. It anticipates the adjusted working margin to be 8.5%, whereas it reported 10% in fiscal 2024.

Administration envisions an adjusted EPS of $10.85-$11.00, up barely from the earlier vary of $10.75 to $11.00, whereas it delivered $11.74 in fiscal 2024. The EPS steering for fiscal 2025 displays an unfavorable impression of $1.05 from tariffs, partly offset by a positive impression of about 45 cents from foreign-currency translation.

Curiosity bills are projected to extend to $80 million from the $67 million reported in 2024 as a result of impacts of funding the accelerated share repurchase agreements. The adjusted efficient tax price is projected to be 22%.

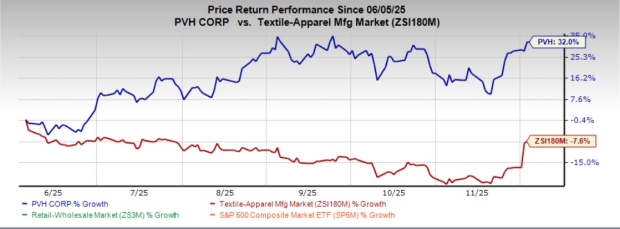

This Zacks Rank #4 (Promote) firm’s inventory has gained 32% previously six months in opposition to the trade‘s 7.6% drop.

PVH Inventory’s Worth Efficiency

Picture Supply: Zacks Funding Analysis

Key Picks

Ralph Lauren Company RL designs, markets and distributes way of life merchandise in North America, Europe, Asia and internationally. It presently carries a Zacks Rank #2 (Purchase). You’ll be able to see the whole record of right now’s Zacks #1 Rank (Sturdy Purchase) shares right here.

The Zacks Consensus Estimate for RL’s present fiscal-year gross sales and earnings signifies development of 9.5% and 24.9%, respectively, from the year-ago reported figures. Ralph Lauren delivered a trailing four-quarter common earnings shock of 9.8%.

Revolve Group, Inc. RVLV operates as an internet vogue retailer for millennial and Technology Z customers in the US and internationally. It carries a Zacks Rank #2 at current. Revolve Group delivered a trailing four-quarter common earnings shock of 61.7%.

The Zacks Consensus Estimate for RVLV’s present fiscal-year revenues implies development of 6.8% from the year-ago actuals.

Kontoor Manufacturers, Inc. KTB, a life-style attire firm, designs, produces, procures, markets, distributes and licenses denim, attire, footwear and equipment. It presently carries a Zacks Rank #2. KTB delivered a trailing four-quarter earnings shock of 14%, on common.

The Zacks Consensus Estimate for Kontoor Manufacturers’ present financial-year gross sales and earnings signifies development of 19.4% and 12.5%, respectively, from the year-ago reported figures.

Zacks’ Analysis Chief Picks Inventory Most More likely to “At Least Double”

Our consultants have revealed their High 5 suggestions with money-doubling potential – and Director of Analysis Sheraz Mian believes one is superior to the others. In fact, all our picks aren’t winners however this one might far surpass earlier suggestions like Hims & Hers Well being, which shot up +209%.

See Our High Inventory to Double (Plus 4 Runners Up) >>

Ralph Lauren Company (RL) : Free Inventory Evaluation Report

PVH Corp. (PVH) : Free Inventory Evaluation Report

Kontoor Manufacturers, Inc. (KTB) : Free Inventory Evaluation Report

Revolve Group, Inc. (RVLV) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.