JPMorgan Chase JPM) as soon as once more reminded Wall Avenue why it stays the gold normal amongst U.S. banks after delivering a stellar Q2 report that impressively topped analyst expectations yesterday.

Pushed by surging buying and selling income, a rebound in funding banking, resilient client spending, and wholesome mortgage progress, the banking large posted one other report quarter whereas elevating key steering metrics.

With JPM hitting an all-time excessive of $351 a share following its earnings launch, buyers could also be questioning whether or not the post-earnings rally has additional room to run or if a lot of the excellent news is already priced in.

Picture Supply: Zacks Funding Analysis

JPMorgan’s Document Q2 Outcomes

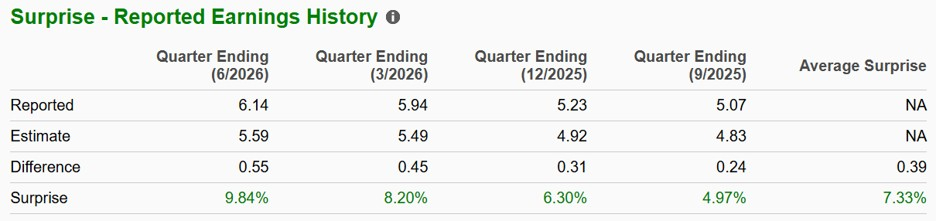

JPMorgan’s second-quarter numbers simply exceeded Wall Avenue estimates throughout the board.

The corporate earned report quarterly adjusted internet earnings of $16.9 billion or $6.14 per share, which was up almost 24% yr over yr, and virtually 10% above EPS expectations of $5.59.

This got here on income of $57.34 billion, which was additionally a quarterly peak and mirrored 27% progress from the prior yr quarter whereas topping estimates of $49.14 billion by almost 17%.

Picture Supply: Zacks Funding Analysis

The energy was broad-based:

- Funding banking charges rebounded sharply as capital markets exercise improved.

- Equities buying and selling income surged because of elevated market volatility and consumer exercise.

- Asset and wealth administration generated report charges.

- Shopper banking remained resilient with continued mortgage and deposit progress.

- Credit score high quality remained wholesome, prompting administration to decrease its anticipated internet charge-off outlook.

CEO Jamie Dimon credited sturdy consumer exercise and resilient client spending for the spectacular quarter whereas noting that the financial institution continues to learn from AI-related financing exercise throughout company America. Nonetheless, Dimon reiterated that geopolitical tensions, elevated authorities deficits, and inflation stay long-term dangers.

JPMorgan’s Optimistic Outlook

Maybe much more encouraging than the quarterly beat was administration’s up to date outlook.

JPMorgan raised its full-year internet curiosity earnings (NII) steering to roughly $105.5 billion from $103 billion, reflecting stronger lending traits and continued enterprise momentum.

The banking large modestly elevated its annual expense outlook to $107.5 billion because it continues to speculate closely in know-how and synthetic intelligence, however buyers largely considered the upper spending as growth-oriented relatively than regarding.

Moreover, JPMorgan lowered its anticipated credit-loss outlook to roughly 3.2% from 3.4%, reinforcing confidence that earnings momentum can proceed by means of the second half of the yr.

JPM Nonetheless Affords Sound Worth

Regardless of buying and selling close to report highs, JPMorgan’s valuation stays removed from extreme.

Massive U.S. banks have usually traded at reductions to the broader market on account of their cyclical nature, and JPMorgan is not any exception. Even after its sturdy rally over the past a number of years, JPM trades at a really affordable ahead earnings a number of of 15X.

That is roughly on par with its Zacks Monetary-Funding Financial institution Trade common and a nice low cost to the benchmark S&P 500’s 23X, whereas being beneath the P/E premiums of many large-cap tech shares.

Contemplating the corporate’s elevated profitability, industry-leading return on tangible frequent fairness, fortress steadiness sheet, and distinctive capital era, buyers should still view JPM’s valuation as a steal.

Picture Supply: Zacks Funding Analysis

In the meantime, JPMorgan continues to reward shareholders by means of a mix of dividend progress and share repurchases.

Providing a decent 1.75% annual dividend yield that exceeds the S&P 500’s 1.03% common and its Zacks {industry} common of 1.64%, JPM has remained interesting to each progress and income-oriented buyers.

Picture Supply: Zacks Funding Analysis

Can JPM Inventory Attain Increased Highs?

A number of catalysts may preserve supporting JPMorgan shares over the approaching quarters.

If capital markets stay energetic, funding banking charges and buying and selling income may keep elevated. On the identical time, stabilization in rates of interest ought to help internet curiosity earnings, whereas bettering credit score situations may scale back future mortgage losses.

Synthetic intelligence additionally represents an more and more vital alternative. JPMorgan has change into one among Wall Avenue’s largest AI buyers, deploying the know-how throughout fraud detection, customer support, software program growth, analysis, and inside productiveness initiatives. The financial institution additionally advantages not directly because it funds lots of the largest AI infrastructure initiatives being undertaken by company purchasers.

Mixed with one of many strongest steadiness sheets in world banking and a confirmed administration staff, JPMorgan seems well-positioned to proceed delivering industry-leading monetary efficiency.

Abstract & Conclusion

JPMorgan as soon as once more demonstrated why it’s broadly considered as one of many premier banking franchises on the planet. The corporate’s spectacular earnings beat, bettering steering, wholesome credit score traits, diversified income streams, and shareholder-friendly capital allocation have strengthened the long-term funding thesis.

Though JPM is buying and selling close to report highs, its valuation nonetheless seems affordable relative to its earnings energy and long-term progress prospects. For buyers in search of publicity to the monetary sector, JPM stays one of many highest-quality names able to reaching increased highs if favorable working traits proceed, with the inventory at the moment sporting a Zacks Rank #2 (Purchase).

Radical New Know-how Might Hand Traders Enormous Beneficial properties

Quantum Computing is the following technological revolution, and it could possibly be much more superior than AI.

Whereas some believed the know-how was years away, it’s already current and transferring quick. Massive hyperscalers, comparable to Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to combine quantum computing into their infrastructure.

Senior Inventory Strategist Kevin Prepare dinner reveals 7 rigorously chosen shares poised to dominate the quantum computing panorama in his report, Past AI: The Quantum Leap in Computing Energy.

Kevin was among the many early consultants who acknowledged NVIDIA’s monumental potential again in 2016. Now, he has keyed in on what could possibly be “the following massive factor” in quantum computing supremacy. Right now, you’ve a uncommon probability to place your portfolio on the forefront of this chance.

See High Quantum Shares Now >>

JPMorgan Chase & Co. (JPM) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.