Peloton Interactive, Inc. PTON and Planet Health, Inc. PLNT signify two very completely different approaches to the trendy health market, one constructed on related at-home tools and digital subscriptions, the opposite on an expansive community of reasonably priced gyms.

Each firms are working to regain momentum after trade disruptions, however their restoration paths and investor expectations fluctuate broadly. As health spending normalizes and competitors intensifies, the large query for shareholders turns into: Which inventory gives the stronger upside from right here?

The Case for PTON

Peloton’s bettering profitability is a key pillar of the bullish argument. The corporate delivered $118 million in adjusted EBITDA in first-quarter fiscal 2026, beating expectations by $18 million, and generated $67 million in free money move, a major enchancment from final 12 months. Administration raised full-year EBITDA steering to $425-$475 million, supported by faster-than-expected value financial savings and tariff advantages.

The corporate can be gaining traction with its largest product refresh so far, together with the brand new Cross Coaching Sequence tools lineup and Peloton IQ AI teaching, which administration says is driving a shift towards premium {hardware} and better engagement ranges. Sturdy product innovation helps reinforce Peloton’s positioning past related biking and right into a broader wellness ecosystem.

Development in distribution channels additional strengthens Peloton’s outlook. The model expanded to 10 micro shops in america and fashioned a brand new retail partnership with Johnson Health & Wellness, broadening its attain throughout 46 states. Its industrial phase, supported by Precor, can be gaining momentum in hospitality and residential markets, creating new income alternatives.

Regardless of operational progress, Peloton faces continued top-line stress. Paid Linked Health subscriptions fell 6% 12 months over 12 months, contributing to a 6% income decline within the fiscal first quarter. Administration expects churn to rise in second-quarter fiscal 2026 following subscription worth will increase earlier than stabilizing later within the 12 months. The corporate additionally notes ongoing softness within the related health tools class, which stays in decline post-pandemic.

Peloton can be managing the influence of one other product recall involving the Unique Sequence Bike+, which resulted in a $16.5 million stock accrual and will briefly have an effect on member sentiment and utilization. Whereas administration expects minimal income disruption, recall-related headlines danger slowing subscriber momentum at a important stage of restoration.

The Case for PLNT

Planet Health continues to learn from sturdy demand developments and an increasing member base. The corporate ended third-quarter 2025 with roughly 20.7 million members and delivered 6.9% system-wide same-club gross sales progress, supported by each pricing and membership will increase. Revenues rose 13% 12 months over 12 months, and administration raised its full-year outlook for revenues, EBITDA and web revenue progress on the again of this sturdy momentum.

The model’s worth proposition is resonating particularly with youthful customers. Participation within the Excessive College Summer season Cross program surged 30% 12 months over 12 months, bringing in 3.7 million teenagers, lots of whom later transformed to paying memberships. That success helps Planet Health strengthen long-term loyalty and model relevance with Gen Z, a key demographic for sustained progress.

Growth stays a robust driver. The corporate opened 35 new golf equipment in third-quarter 2025, bringing the worldwide depend to 2,795 and continues rolling out optimized membership codecs and upgraded energy tools that attracted enthusiastic franchisee funding. Planet Health additionally sees rising actual property availability as a tailwind for accelerated membership growth, with franchisees actively in search of new territories and conversion alternatives.

Whereas be a part of developments are sturdy, attrition stays elevated on a year-over-year foundation because of the rollout of click-to-cancel and administration expects increased churn to proceed by means of fourth-quarter 2025. Though cancellation behaviors are moderating, the membership depend dipped barely versus the second quarter, typical seasonality, however nonetheless a reminder that web provides will not be but on a gradual upward trajectory.

One other danger is reliance on pricing to maintain same-club gross sales progress. Roughly 80% of third-quarter 2025 comp progress got here from increased charges versus quantity. With one other Black Card worth enhance deliberate for 2026, there may be potential for shopper resistance, momentary combine stress or slower conversion to the premium tier, particularly as gym-goers turn into extra value-conscious in a aggressive health panorama.

How Do Estimates Evaluate for PTON & PLNT?

The Zacks Consensus Estimate for Peloton’s fiscal 2026 gross sales and EPS implies virtually flat and progress of 140%, respectively, 12 months over 12 months. Earnings estimate revisions for fiscal 2026 have witnessed upward revisions prior to now 30 days.

Picture Supply: Zacks Funding Analysis

The Zacks Consensus Estimate for PLNT’s 2025 gross sales and EPS implies year-over-year will increase of 10.8% and 15.4%, respectively. Earnings estimates for 2025 have witnessed upward revisions prior to now 30 days.

Picture Supply: Zacks Funding Analysis

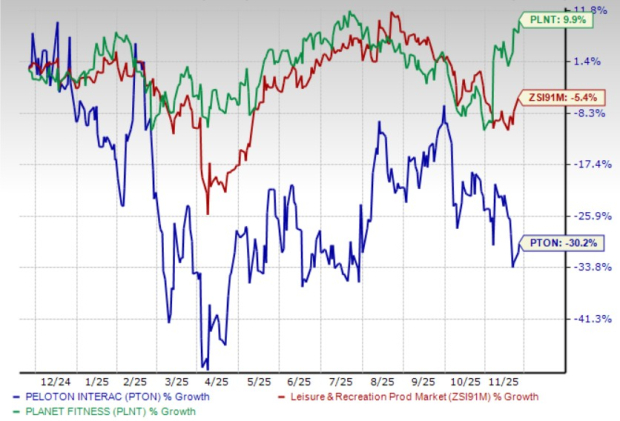

Worth Efficiency & Valuation: PTON vs. PLNT

PTON inventory has tanked 30.2% prior to now 12 months. Nevertheless, PLNT’s shares have gained 9.9% in the identical time-frame.

Worth Efficiency

Picture Supply: Zacks Funding Analysis

PTON is buying and selling at a ahead 12-month price-to-sales ratio of 1.12X, under its median of 1.22X over the past 12 months. PLNT’s ahead gross sales a number of sits at 6.47X, above its median of 5.30X over the identical time-frame.

P/S (F12M)

Picture Supply: Zacks Funding Analysis

Wrapping Up

Each Peloton and Planet Health are making significant progress of their restoration journeys, supported by bettering profitability and renewed strategic focus, making them cheap maintain candidates for buyers. Peloton is displaying encouraging indicators of stabilization by means of innovation, value self-discipline and increasing distribution, nevertheless it nonetheless must show that subscriber developments can return to sustainable progress.

Planet Health, then again, advantages from regular demand for in-person health, sturdy model momentum and rising franchise funding, placing it barely forward at this stage by way of consistency and visibility. Whereas every firm gives a novel path to long-term upside, Planet Health presently seems to have the clearer runway, however Peloton’s turnaround efforts hold it firmly within the recreation for affected person buyers.

Each PTON and PLNT carry a Zacks Rank #3 (Maintain). You may see the whole checklist of right now’s Zacks #1 Rank (Sturdy Purchase) shares right here.

Free Report: Taking advantage of the 2nd Wave of AI Explosion

The subsequent section of the AI explosion is poised to create important wealth for buyers, particularly those that get in early. It is going to add actually trillion of {dollars} to the economic system and revolutionize almost each a part of our lives.

Traders who purchased shares like Nvidia on the proper time have had a shot at enormous good points.

However the rocket experience within the “first wave” of AI shares might quickly come to an finish. The sharp upward trajectory of those shares will start to degree off, leaving exponential progress to a brand new wave of cutting-edge firms.

Zacks’ AI Increase 2.0: The Second Wave report reveals 4 under-the-radar firms that will quickly be shining stars of AI’s subsequent leap ahead.

Entry AI Increase 2.0 now, completely free >>

Planet Health, Inc. (PLNT) : Free Inventory Evaluation Report

Peloton Interactive, Inc. (PTON) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.