Markets confronted a tug-of-war on Wednesday between lingering optimism {that a} US-Iran settlement was imminent and a gentle drumbeat of contradictory indicators that stored merchants from absolutely committing in both course. WTI crude oil bore the deepest losses of the session as conflicting headlines from Washington and Tehran created whipsaw worth motion, whereas equities managed to carry close to document territory and the New Zealand greenback emerged because the standout forex mover following a hawkish RBNZ coverage assertion.

Try the foreign exchange information and financial updates you will have missed within the newest buying and selling session!

Foreign exchange Information Headlines & Knowledge:

Promoted: Day merchants & Scalpers have higher odds of creating nice choices in the event that they’re alerted to market catalysts straight away, like information of a possible US-Iran settlement, straight away. Get the real-time feed that execs use to catch the information.

Be part of FinancialJuice for Free to be taught extra!

Disclosure: We could earn a fee from our companions for those who enroll by means of our hyperlinks, at no further price to you.

Broad Market Worth Motion:

Greenback Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Quicker With TradingView

Wednesday’s session featured clear divergence throughout asset lessons, with WTI crude bearing the day’s deepest losses as conflicting indicators on a possible US-Iran settlement stored oil merchants on edge from the Asian open by means of the New York shut. Equities managed to carry close to document territory, gold slid to what sources described as recent two-month lows, and the greenback ended the day modestly firmer.

WTI crude oil was the session’s hardest-hit asset, settling round $88.40, a decline of roughly 4.12% on the day. Oil had already been drifting steadily decrease by means of the Asian and London periods as hopes for a deal remained intact however unconfirmed, and promoting intensified throughout the US morning as Trump’s feedback solid doubt on near-term progress. The intraday worth motion was sharp and two-directional, with a quick spike towards the decrease finish of the day’s vary showing to coincide with the competing Iranian media experiences earlier than the White Home denial and Trump’s subsequent remarks solidified the bearish tone. An intraday low close to $86.75 was established earlier than costs recovered partially into the shut.

Gold declined roughly 1.23% to shut round $4,452. The dear metallic had been beneath strain since early within the Asian session, with the transfer probably reflecting a broader hawkish repricing in world price expectations because the RBNZ’s up to date OCR projections and BOJ commentary from Governor Ueda each pointed towards tighter financial situations forward. Gold discovered intraday assist close to $4,402 earlier than recovering into the US afternoon, although the general transfer nonetheless represented recent multi-week lows on the day.

The S&P 500 closed little modified, edging up roughly 0.08% to roughly 7,521. US equities had prolonged their latest run into the European open, with futures pointing to further upside, however momentum pale throughout the US morning as Trump’s Iran feedback tempered expectations for an imminent deal. The index pulled again from session highs close to 7,554, briefly examined assist round 7,499, and floor its means again to roughly flat by the shut. Goldman Sachs raised its year-end S&P 500 goal to eight,000 throughout the session, with strategists arguing that AI-driven earnings momentum would assist additional good points. In after-hours buying and selling, Salesforce issued a tepid income outlook whereas Snowflake raised its gross sales forecast and introduced a dedication to spend an extra $6 billion on Amazon Net Providers.

Bitcoin eased roughly 1.39% to round $74,940. The cryptocurrency tracked the gentle pullback in threat urge for food throughout the US session with out an obvious direct catalyst, posting its losses in a comparatively orderly style in comparison with the sharp strikes in crude oil.

The US 10-year Treasury yield declined roughly 0.18% to round 4.50%. Yields traded quietly by means of the Asian and London periods earlier than easing barely across the US open. Regardless of the broadly stronger-than-expected Richmond Fed information and a still-positive weekly ADP employment print, the yield drifted decrease on the day, probably reflecting some safe-haven demand tied to the elevated uncertainty within the Center East.

Promoted: The Prop Agency Constructed for Severe Merchants.

Don’t let your buying and selling technique be held again by capital limitations. Alpha Capital Group gives entry to simulated funded accounts from $5K to $200K, with entry costs beginning as little as $40. They’re distinguished by their options, together with zero commissions, limitless buying and selling days throughout analysis, and an 80% revenue break up. Begin with a professional-sized account and scale your shopping for energy as much as $2M. Be part of 250K+ merchants in 180+ nations right this moment.

Be taught extra about Alpha Capital Group and present low cost codes right here!

Disclosure: We could earn a fee from our companions for those who enroll by means of our hyperlinks, at no further price to you.

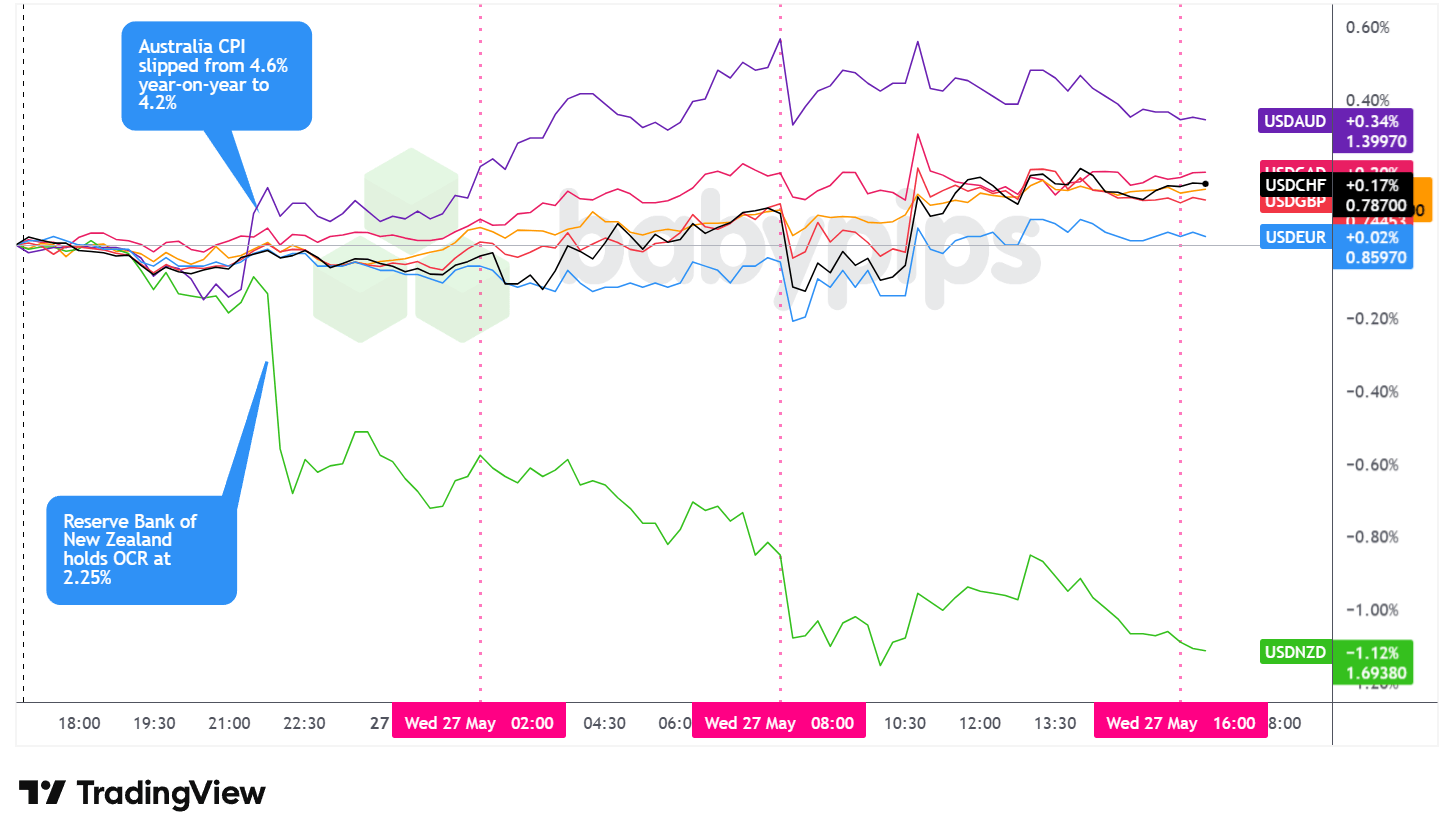

FX Market Conduct: U.S. Greenback vs. Majors

Overlay of USD vs. Majors – Chart Quicker With TradingView

The US greenback traded in a principally sideways, blended vary throughout the Asian session, with the Australian greenback and New Zealand greenback serving because the clear standouts on account of main home catalysts from every nation. From the London open onward, the greenback step by step floor greater in opposition to most main currencies, with a few high-volatility bursts throughout the US session tied to the competing Iran-related headlines. On the Wednesday shut, the greenback posted web good points in opposition to all main currencies besides the New Zealand greenback, which held onto its RBNZ-driven good points by means of the ultimate hour of buying and selling.

Throughout the Asian session, the greenback held a comparatively quiet and directionless vary in opposition to the euro, sterling, yen, Swiss franc, and Canadian greenback, with no vital regional catalysts to drive clear momentum in these pairs. AUD/USD got here beneath strain after the April CPI report printed softer than anticipated at 4.2% year-on-year versus the 4.6% consensus forecast, with the month-to-month studying additionally lacking at 0.4% versus a 0.7% forecast. It’s value noting that the trimmed imply measure of core inflation ticked as much as 3.4% yearly, a 22-month excessive, suggesting the headline miss could owe partly to non permanent elements together with a authorities gasoline excise discount, which leaves the RBA’s June choice genuinely open.

NZD/USD, against this, surged sharply because the RBNZ’s Financial Coverage Assertion delivered what markets interpreted as a hawkish maintain. The OCR was stored at 2.25% by a 3-3 vote resolved by the Governor’s casting vote, however the considerably revised OCR monitor pointing towards a terminal price of three.28% and broad settlement that hikes are coming this yr drove significant NZD demand. NZD/USD pushed sharply greater throughout the Asian session and held most of these good points by means of the rest of the day.

Throughout the London session, the greenback drifted step by step greater in opposition to most majors in a comparatively low-volatility grind. The ECB Monetary Stability Assessment was launched with out new coverage indicators. France’s Client Confidence for Could printed beneath consensus at 82.0 versus a 84.0 forecast, offering a modestly delicate European backdrop. Switzerland’s Financial Sentiment Index beat expectations sharply at -11.1 versus a forecast of -24.0, although the franc’s response appeared restricted relative to the magnitude of the upside shock. The greenback’s gradual appreciation throughout this window could have broadly mirrored the cautious undertone throughout threat belongings as crude oil continued to slip and gold pressed to recent lows on the hawkish world central financial institution repricing narrative.

Throughout the US session, the greenback skilled two notable bouts of elevated volatility. Iranian state TV’s report of a draft MoU probably corresponded with the sharp intraday dip close to the US morning open, one doable rationalization for the temporary spike decrease. The following White Home denial and Trump’s pointed dismissal of deal progress appeared to correlate close to the greenback restoration.

The Richmond Fed information launched throughout the session was broadly constructive, with the composite manufacturing index surging to 13 versus a forecast of 4 and shipments rising to 16 from a previous studying of -2, whereas the weekly ADP employment change got here in at 35.75k, beneath the prior 42.25k however nonetheless pointing to some labor market resilience. The greenback finally held its intraday restoration and closed as a web outperformer, ending greater in opposition to the euro, sterling, Swiss franc, yen, and Canadian greenback whereas sustaining a loss solely in opposition to the New Zealand greenback.

Promoted: The Technique is Half the Battle; Your Mindset is the Relaxation.

Most buying and selling errors aren’t technical—they’re psychological. Within the traditional “Buying and selling within the Zone” by Mark Douglas (⭐ 4.7★ | 10,000+ opinions on Amazon), you’ll discover ways to grasp the probabilistic considering and emotional self-discipline talked about in right this moment’s article. In the event you battle with hesitation or breaking your guidelines, that is your handbook for constant execution.

Disclosure: To assist assist our content material, we could earn a fee from our companions for those who enroll by means of our hyperlinks, at no further price to you.

Upcoming Potential Catalysts on the Financial Calendar

- U.Okay. Automobile Manufacturing for April 2026 at 11:01 pm GMT

- Euro space ECB Lane Speech at 12:00 am GMT

- U.S. Fed Jefferson Speech at 12:00 am GMT

- Australia Family Spending for April 2026 at 1:30 am GMT

- Japan Housing Begins for April 2026 at 5:00 am GMT

- Swiss Non Farm Payrolls for March 31, 2026 at 6:30 am GMT

- ECB Lane Speech at 7:15 am GMT

- ECB President Lagarde Speech at 7:20 am GMT

- Euro space Financial Sentiment for Could 2026 at 9:00 am GMT

- European Central Financial institution Financial Coverage Assembly Accounts at 11:30 am GMT

- U.S. Constructing Permits Remaining for April 2026 at 12:10 pm GMT

- Canada Common Weekly Earnings for March 2026 at 12:30 pm GMT

- U.S. Preliminary Jobless Claims for Could 23, 2026 at 12:30 pm GMT

- U.S. GDP Development Price 2nd Est at 12:30 pm GMT

- U.S. Core PCE Worth Index for April 2026 at 12:30 pm GMT

- U.S. Sturdy Items Orders for April 2026 at 12:30 pm GMT

- U.S. Private Earnings & Spending for April 2026 at 12:30 pm GMT

- U.S. Fed Williams Speech at 12:55 pm GMT

- Financial institution of Canada Monetary Stability Report at 2:00 pm GMT

- U.S. New House Gross sales for April 2026 at 2:00 pm GMT

- ECB Schnabel Speech at 3:45 pm GMT

- U.S. EIA Crude Oil Shares Change for Could 22, 2026 at 4:00 pm GMT

Thursday brings one of many week’s most data-heavy periods, with a dense US 12:30 pm GMT window that features the second estimate of Q1 GDP progress, the Core PCE Worth Index for April, Sturdy Items Orders, Private Earnings and Spending, and the weekly Preliminary Jobless Claims. The Core PCE print will appeal to specific consideration because the Fed’s most well-liked inflation gauge, particularly given ongoing debate about whether or not the disinflation development has stalled.

Earlier within the European session, a number of ECB audio system take the stage together with Chief Economist Lane at 7:15 am GMT, President Lagarde at 7:20 am GMT, and Govt Board member Schnabel at 3:45 pm GMT. The ECB’s Financial Coverage Assembly Accounts at 11:30 am GMT can also appeal to consideration for any nuance on the present coverage path.

The Financial institution of England’s Breeden speaks at 8:05 am GMT. Later within the day, the Financial institution of Canada releases its Monetary Stability Report at 2:00 pm GMT, and the EIA crude oil shares change information at 4:00 pm GMT will likely be watched intently given the session’s sharp oil worth strikes.

Keep frosty on the market, foreign exchange associates!

Wednesday’s market motion exhibits why watching currencies in isolation can depart you blindsided. When crude oil, gold, equities, and the greenback all moved in response to the identical geopolitical headlines and central financial institution repricing, merchants who understood how these belongings join had a large benefit over these watching solely the FX chart.

📖 What Is Intermarket Evaluation?

Studying this helps you perceive find out how to learn shares, bonds, commodities, and currencies collectively, why asset class actions affirm or contradict one another, and find out how to spot divergence earlier than your FX chart ideas you off.

And for those who’re not a Premium subscriber but, take into account becoming a member of to unlock classes that present you the complete image of how markets work collectively.

With Babypips Premium, you get full entry to College of Pipsology classes that aid you perceive not simply remoted forex strikes, however the intermarket indicators that skilled merchants use to anticipate worth motion throughout all asset lessons.

👉 Subscribe to Babypips Premium