The This fall earnings reporting cycle ramps up this week, with greater than 300 corporations on deck to report outcomes, together with 4 of the ‘Magnificent 7’ members and 102 S&P 500 members. We’ve Microsoft MSFT, Meta Platforms META, and Tesla TSLA reporting outcomes the identical day after the market’s shut on Wednesday, January twenty eighth, and Apple AAPL on Thursday, January twenty ninth, after the market’s shut.

The Magazine 7 shares have struggled currently, with the group lagging the broader market over the trailing twelve-month interval, as could be seen by the blue line (+8.9%) within the chart beneath. Whereas all 4 Magazine 7 shares reporting this week have underperformed, Meta and Microsoft have been significantly weak, whereas Apple and Tesla have executed marginally higher.

Picture Supply: Zacks Funding Analysis

The important thing points with Microsoft, Meta, and even Apple are all tied to what these corporations are doing within the AI area. Whereas Microsoft and Meta are among the many huge spenders on AI, Apple has been lacking in motion, making Apple buyers nervous in regards to the firm’s long-term aggressive positioning.

Microsoft was initially seen as a pacesetter within the area, with its relationship with OpenAI including to its credentials. However that management standing has now gone to Alphabet, significantly since regulatory headwinds eased for the search large final yr.

By way of particular expectations, Apple is predicted $2.65 per share in earnings on $137.5 billion in revenues, representing year-over-year beneficial properties of +10.4% and +10.6%, respectively. The revisions pattern has been optimistic, with estimates steadily shifting up.

For Microsoft, the expectation is of $3.88 per share in earnings on $80.2 billion in revenues, representing year-over-year progress charges of +20.1% and +15.2%, respectively. The revisions pattern has been optimistic for Microsoft as nicely, with estimates for each the December quarter and monetary yr 2026 (FY ends in June) going up.

For Meta, the expectation is of $8.15 per share in earnings on $58.4 billion in revenues, representing year-over-year progress charges of +1.6% and +20.7%, respectively. The inventory was down huge following the final quarterly launch on October 29th.

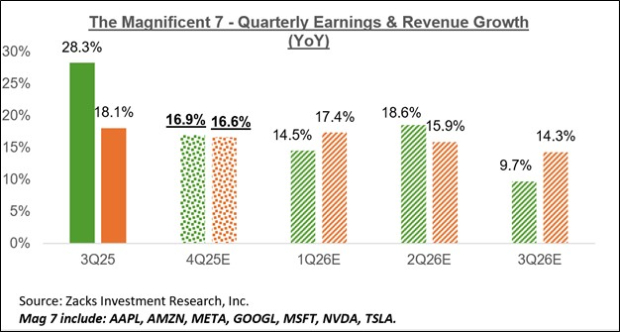

Wanting on the Magazine 7 group as a complete, This fall earnings are anticipated to extend by +16.9% from the identical interval final yr on +16.6% greater revenues. The chart beneath reveals the group’s 2025 This fall earnings and income progress expectations within the context of what was achieved within the previous interval and what’s anticipated within the coming three quarters.

Picture Supply: Zacks Funding Analysis

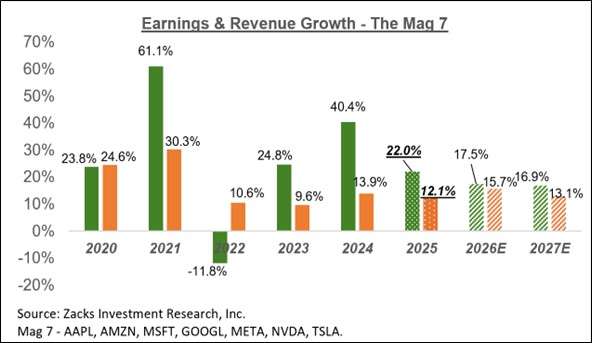

The chart beneath reveals the Magazine 7 group’s earnings and income progress image on an annual foundation.

Picture Supply: Zacks Funding Analysis

The group has been having fun with a steadily enhancing earnings outlook, with analysts elevating their estimates. We noticed that pattern in play forward of the beginning of the Q3 earnings season, and one thing comparable is in place for 2025 This fall as nicely.

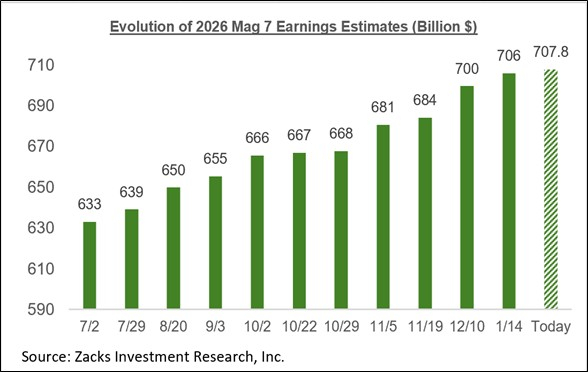

The chart beneath reveals how mixture earnings estimates for the Magazine 7 group have advanced since July 2025.

Picture Supply: Zacks Funding Analysis

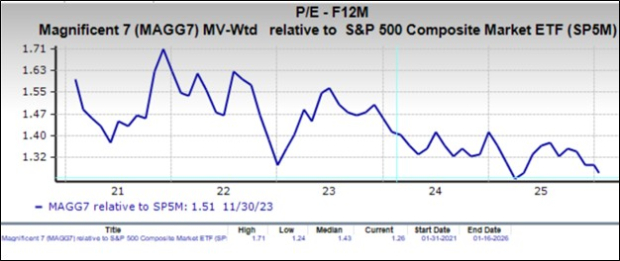

The chart beneath reveals the Magazine 7 group’s valuation on a ahead 12-month P/E foundation during the last 5 years relative to the S&P 500 index.

Picture Supply: Zacks Funding Analysis

The chart beneath reveals the Magazine 7 ahead valuation a number of relative to the market a number of.

Picture Supply: Zacks Funding Analysis

The way in which to interpret the above chart is that the Magazine 7 group is presently buying and selling at 126% of the S&P 500 a number of, or at a 26% premium to the market a number of. During the last 5 years, the Magazine 7 group has traded as excessive as a 71% premium, as little as a 24% premium, with a median premium of 43%.

This fall Earnings Season Scorecard

By means of Friday, January 23rd, we’ve got seen This fall outcomes from 64 S&P 500 members. Complete earnings for these corporations are up +17.5% from the identical interval final yr on +7.8% greater revenues, with 82.8% beating EPS estimates and 68.8% beating income estimates.

As famous earlier, we’ve got 102 index members reporting outcomes this week. The week’s line-up contains, moreover the aforementioned Magazine 7 members, a consultant cross-section of bellwether operators, together with UPS, Boeing, GM, Starbucks, AT&T, IBM, Visa and Mastercard, Caterpillar, Comcast, American Specific, Exxon, Chevron, and others.

The comparability charts beneath examine the expansion charges for these 64 index members with these we noticed from this similar group of corporations in different current intervals.

Picture Supply: Zacks Funding Analysis

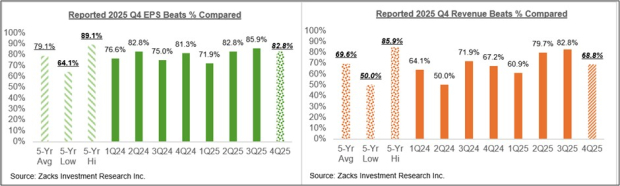

The comparability charts beneath put the This fall EPS and income beats percentages for this group corporations relative to what we had seen from them in different current intervals.

Picture Supply: Zacks Funding Analysis

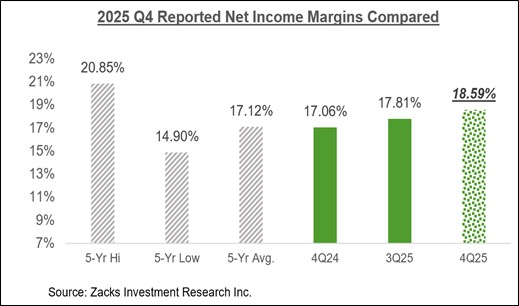

The comparability chart beneath places the This fall internet margins for the 64 corporations which have reported in a historic context.

Picture Supply: Zacks Funding Analysis

As you’ll be able to see above, earnings and income progress stay sturdy, and EPS beats are monitoring above the typical for this group of corporations within the previous 20-quarter interval, although income beats are a tad on the weaker facet.

Loads of outcomes are nonetheless to return. However at this early stage, the income beats share is monitoring beneath the historic common, with all the opposite metrics within the historic vary.

The Earnings Massive Image

The chart beneath reveals the This fall earnings and income progress expectations within the context of the place progress has been within the previous 4 quarters and what’s anticipated within the coming three quarters.

Picture Supply: Zacks Funding Analysis

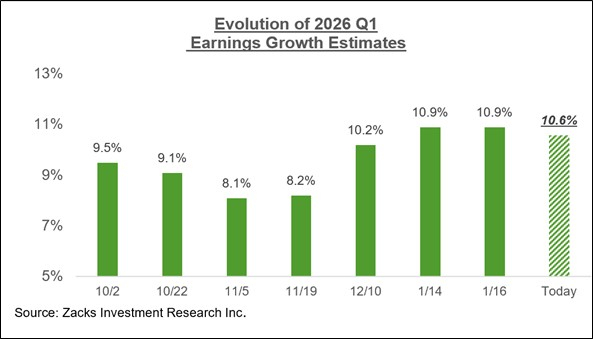

Estimates for the present interval (2026 Q1) have come beneath some strain in current days, because the chart beneath reveals.

Picture Supply: Zacks Funding Analysis

The above downtrend however, estimates have really elevated modestly for 10 of the 16 Zacks sectors because the begin of January, together with Tech, Fundamental Supplies, Autos, Industrials, Transportation, and others. On the detrimental facet, estimates have come down for six of the 16 Zacks sectors, together with Vitality, Medical, Shopper Discretionary, and others.

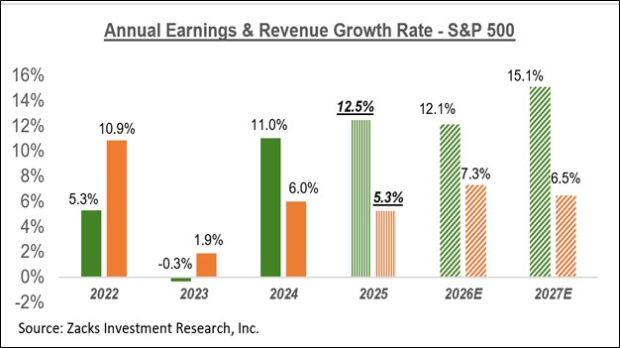

The chart beneath reveals the general earnings image on a calendar-year foundation, with double-digit earnings progress anticipated in 2025 and 2026.

Picture Supply: Zacks Funding Analysis

For an in depth take a look at the general earnings image, together with expectations for the approaching intervals, please try our weekly Earnings Tendencies report >>>> Earnings Estimates Maintain Rising: A Nearer Look

Radical New Expertise Might Hand Traders Enormous Positive aspects

Quantum Computing is the subsequent technological revolution, and it may very well be much more superior than AI.

Whereas some believed the expertise was years away, it’s already current and shifting quick. Massive hyperscalers, akin to Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to combine quantum computing into their infrastructure.

Senior Inventory Strategist Kevin Prepare dinner reveals 7 fastidiously chosen shares poised to dominate the quantum computing panorama in his report, Past AI: The Quantum Leap in Computing Energy.

Kevin was among the many early consultants who acknowledged NVIDIA’s monumental potential again in 2016. Now, he has keyed in on what may very well be “the subsequent huge factor” in quantum computing supremacy. At this time, you could have a uncommon likelihood to place your portfolio on the forefront of this chance.

See High Quantum Shares Now >>

Apple Inc. (AAPL) : Free Inventory Evaluation Report

Microsoft Company (MSFT) : Free Inventory Evaluation Report

Tesla, Inc. (TSLA) : Free Inventory Evaluation Report

Meta Platforms, Inc. (META) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.