")

Newmont Company’s NEM shares have popped 26.2% prior to now three months, buoyed by a surge in gold costs to file highs amid heightened geopolitical tensions and hopes of extra rate of interest cuts. NEM’s forecast-topping earnings efficiency, pushed by its operational effectivity and the energy of its Tier 1 portfolio, additionally contributed to the rally.

NEM inventory has outperformed the Zacks Mining – Gold business’s 17.5% rise and the S&P 500’s enhance of 6%. Amongst its gold mining friends, Barrick Mining Company B, Agnico Eagle Mines Restricted AEM and Kinross Gold Company KGC have gained 46.7%, 12.9% and 29.1%, respectively, over the identical interval.

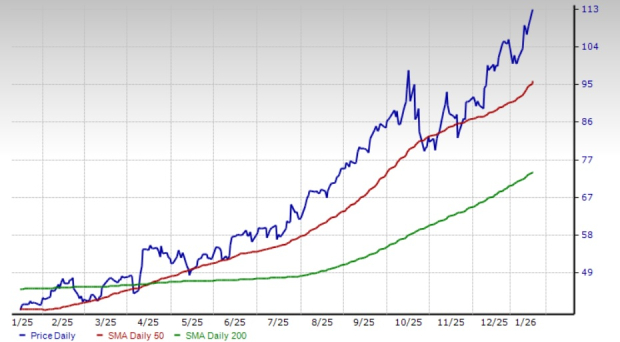

NEM’s 3-month Worth Efficiency

Picture Supply: Zacks Funding Analysis

Technical indicators for NEM present bullish momentum. The NEM inventory has been buying and selling above its 200-day easy transferring common (SMA) since April 9, 2025, suggesting a long-term uptrend. It is usually presently buying and selling above its 50-day SMA. The 50-day SMA can also be studying increased than the 200-day SMA, following a golden crossover on April 16, 2025, indicating a bullish pattern.

NEM Inventory Trades Above 50-Day SMA

Picture Supply: Zacks Funding Analysis

Picture Supply: Zacks Funding Analysis

Is the time proper to purchase NEM’s shares for potential upside? Let’s check out the inventory’s fundamentals.

Initiatives & Asset Streamlining to Drive NEM’s Progress

Newmont continues to put money into development tasks in a calculated method. The corporate is pursuing a number of tasks, together with the Ahafo North enlargement in Ghana and the Cadia Panel Caves and Tanami Enlargement 2 in Australia. These tasks ought to increase manufacturing capability and lengthen mine life, driving revenues and income.

NEM, in October 2025, achieved a big milestone at Ahafo North. It achieved industrial manufacturing on the mission, which adopted the primary gold pour in September 2025. Ahafo North is predicted to provide between 275,000 and 325,000 ounces of gold yearly over an estimated mine lifetime of 13 years. Manufacturing is predicted to be 50,000 ounces this 12 months, with a ramp-up to full capability in 2026.

Newmont has additionally divested non-core companies because it shifts its strategic focus to Tier 1 property. NEM accomplished its non-core divestiture program in April 2025, with the sale of its Akyem operation in Ghana and its Porcupine operation in Canada. NEM has executed agreements to promote its shares in Greatland Sources Restricted and Discovery Silver Corp, for complete money proceeds of round $470 million after taxes and commissions.

Following the sale of those shares, the corporate anticipates producing $3 billion in after-tax money proceeds from its 2025 divestiture program. These funds will assist Newmont’s capital allocation technique, which focuses on reinforcing its steadiness sheet and delivering returns to its shareholders.

Sturdy Monetary Well being Helps NEM’s Capital Allocation

Newmont has a robust liquidity place and generates substantial money flows, which permit it to fund its development tasks, meet short-term debt obligations and drive shareholder worth. On the finish of the third quarter of 2025, Newmont had sturdy liquidity of $9.6 billion, together with money and money equivalents of round $5.6 billion. Its free money movement greater than doubled 12 months over 12 months to a file $1.6 billion, led by a rise in web money from working actions. Internet money from working actions shot up 40% from the prior-year quarter to $2.3 billion.

NEM has distributed greater than $5.7 billion to its shareholders by means of dividends and share repurchases over the previous two years. It additionally stays dedicated to deleveraging, lowering debt by roughly $2 billion within the third quarter, leading to a near-zero web debt place on the finish of the quarter. Newmont has repurchased shares value $2.1 billion this 12 months, executing $3.3 billion from $6 billion of authorization.

Newmont stands to profit from the energy in gold costs, which ought to drive its profitability and money movement technology. Gold costs have seen a record-setting rally final 12 months, primarily attributable to aggressive commerce insurance policies, together with sweeping new import tariffs introduced by President Donald Trump, which have intensified world commerce tensions and heightened investor nervousness. Additionally, central banks worldwide have been accumulating gold reserves, led by dangers arising from Trump’s insurance policies.

Gold costs surged about 65% final 12 months and at the moment are buying and selling above $4,600 per ounce. The rally was additional supported by the Federal Reserve’s fee cuts and expectations of extra easing amid indicators of U.S. financial softening and labor market considerations, which helped propel bullion to file ranges.

Elevated central financial institution shopping for, continued expectations of fee cuts, and chronic safe-haven demand pushed by geopolitical and commerce tensions, in addition to broader macroeconomic uncertainty, are anticipated to underpin gold costs. Rising geopolitical strains, together with these linked to the U.S.-Venezuela battle and the continuing protests in Iran and the potential U.S. intervention, and considerations over the independence of the Federal Reserve have additionally fueled the latest spike in bullion to file ranges. Collectively, these components are prone to maintain situations favorable for additional upside in gold costs.

NEM provides a dividend yield of 0.9% on the present inventory value. Its payout ratio is 17% (a ratio under 60% is an effective indicator that the dividend will probably be sustainable). Backed by sturdy money flows and sound monetary well being, the corporate’s dividend is perceived as protected and dependable.

Falling Gold Manufacturing Weighs on Newmont’s Efficiency

Newmont noticed decrease gold manufacturing for the third quarter of 2025, partly linked to its strategic divestment of non-core property. NEM reported a roughly 15% year-over-year and 4% sequential decline in gold manufacturing for the third quarter, reaching 1.42 million ounces. This marked the third straight quarter of sequential manufacturing decline. The decrease manufacturing was resulting from diminished grades and deliberate shutdowns at Penasquito and Lihir, and the tip of mining operations on the Subika open pit at Ahafo South. NEM’s strategic asset gross sales, aimed toward sharpening give attention to Tier-1 operations, have additionally weighed on manufacturing.

Newmont anticipates sustaining its anticipated gold manufacturing for 2025 at about 5.9 million ounces. For the fourth quarter, the corporate expects attributable manufacturing to be comparatively consistent with the third quarter, as new manufacturing from Ahafo North and elevated output from the Nevada Gold Mines three way partnership are anticipated to be offset by decrease manufacturing at Yanacocha and decrease grades at Ahafo South. NEM expects fourth-quarter manufacturing of 1.415 million ounces, indicating a roughly 25% year-over-year decline. The manufacturing decline may undercut the profitability targets for 2025.

NEM’s Earnings Estimates Northbound

Newmont’s earnings estimates for 2025 have been going up over the previous 60 days. The Zacks Consensus Estimate for 2026 has additionally been revised increased over the identical time-frame.

The Zacks Consensus Estimate for 2025 earnings is presently pegged at $6.32, suggesting year-over-year development of 81.6%. Earnings are anticipated to develop roughly 15.4% in 2026.

Picture Supply: Zacks Funding Analysis

Picture Supply: Zacks Funding Analysis

A Take a look at Newmont Inventory’s Valuation

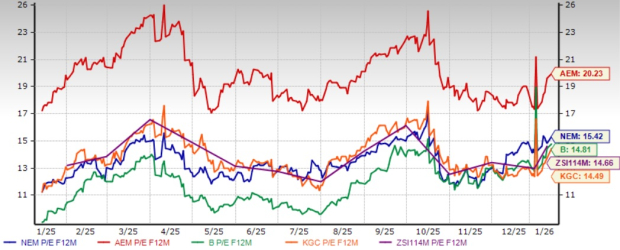

Newmont is presently buying and selling at a ahead value/earnings of 15.42X, a roughly 5.2% premium to the business’s common of 14.66X. NEM is buying and selling at a premium to Barrick and Kinross Gold and at a reduction to Agnico Eagle. Newmont presently has a Worth Rating of C. Barrick and Kinross Gold have a Worth Rating of B, every, whereas Agnico Eagle has a Worth Rating of D.

NEM’s P/E F12M Vs. Business, B, AEM and KGC

Picture Supply: Zacks Funding Analysis

Picture Supply: Zacks Funding Analysis

Closing Ideas: Maintain Onto NEM Shares

Newmont presents a sexy funding case, backed by a strong portfolio of development tasks, the sturdy efficiency of its Tier 1 property and strong monetary well being. The asset streamlining rooted in Newmont’s goal to pay attention capital on high-return, long-life property additionally underpins its long-term sustainability. Different positives embrace rising earnings estimates and a wholesome development trajectory. The energy in bullion costs must also increase NEM’s profitability and drive money movement technology. Nonetheless, weaker manufacturing resulting from divestments and decrease grades could weigh on its efficiency. Retaining this Zacks Rank #3 (Maintain) inventory will probably be prudent for buyers who already personal it.

You possibly can see the entire checklist of as we speak’s Zacks #1 Rank (Sturdy Purchase) shares right here.

(We’re reissuing this text to appropriate a mistake. The unique article, issued on January 13, 2026, ought to not be relied upon.)

Zacks Names #1 Semiconductor Inventory

This under-the-radar firm makes a speciality of semiconductor merchandise that titans like NVIDIA do not construct. It is uniquely positioned to make the most of the following development stage of this market. And it is simply starting to enter the highlight, which is precisely the place you wish to be.

With sturdy earnings development and an increasing buyer base, it is positioned to feed the rampant demand for Synthetic Intelligence, Machine Studying, and Web of Issues. International semiconductor manufacturing is projected to blow up from $452 billion in 2021 to $971 billion by 2028.

See This Inventory Now for Free >>

Newmont Company (NEM) : Free Inventory Evaluation Report

Kinross Gold Company (KGC) : Free Inventory Evaluation Report

Agnico Eagle Mines Restricted (AEM) : Free Inventory Evaluation Report

Barrick Mining Company (B) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.