Howmet Aerospace Inc. HWM and L3Harris Applied sciences, Inc. LHX are each acquainted names working within the aerospace and protection trade. Whereas Howmet is a number one producer of elements and techniques for jet engines and airframes, L3Harris affords built-in applied sciences, together with avionics, digital techniques, and command and management techniques, in the USA and internationally.

Each firms are poised to profit from vital progress alternatives within the aerospace and protection house on account of the enhancing air visitors development and the sturdy U.S. budgetary coverage over the previous a number of years. However which firm is healthier positioned to ship upside in 2026? Let’s evaluate their fundamentals, progress prospects and challenges to see which inventory stands out now.

The Case for Howmet

The strongest driver of Howmet’s enterprise in the intervening time is the industrial aerospace market. With progress in air journey, demand for wide-body plane has elevated, supporting continued OEM spending. Pickup in air journey has been favorable for the corporate because the elevated utilization of plane spurs spending on components and merchandise that it supplies.

Revenues from the industrial aerospace market elevated 15% yr over yr (exceeding $1.1 billion) in third-quarter 2025, constituting 53% of its enterprise. Additionally, within the first and second quarters, revenues from the market elevated 9% and eight% yr over yr, respectively.

The sustained energy was attributed to sturdy demand for engine spares and a report backlog for brand spanking new, extra fuel-efficient plane with decreased carbon emissions. Additionally, wholesome construct charges at Airbus for A320 and A350 plane, together with an anticipated manufacturing restoration within the Boeing 737 MAX plane, maintain promise for HWM’s spare engine demand.

Howmet has additionally been witnessing energy within the protection aerospace trade, cushioned by regular authorities assist. Sturdy orders for engine spares for the F-35 program and spares for legacy fighters just like the F-15 and the F-16 are augmenting HWM’s efficiency. Within the third quarter, revenues from the protection aerospace market surged 24% yr over yr, constituting 17% of the corporate’s revenues.

HWM’s dedication to rewarding its shareholders by means of dividend payouts and share buybacks can also be encouraging. Within the first 9 months of 2025, it paid dividends price $131 million and repurchased shares for $500 million. In August 2025, the corporate hiked its dividend by 20% to 12 cents per share (yearly: 48 cents), marking its second dividend hike in 2025.

The corporate’s wholesome liquidity place additionally provides to its energy. Exiting the third quarter, Howmet’s money equivalents have been $659 million, a lot greater than its short-term maturities and different present liabilities of $251 million. Within the first 9 months of 2025, it generated internet money of $1.23 billion from working actions, whereas its free money move totaled $901 million.

Nevertheless, persistent softness within the industrial transportation market is affecting the corporate’s efficiency. Within the third quarter, revenues from the industrial transportation market declined 3% on a year-over-year foundation, following 14% and 4% declines within the first and second quarters, respectively. Decrease demand within the industrial transportation markets because of decreased OEM builds is predicted to proceed within the close to time period, which is able to probably have an effect on the efficiency of its Cast Wheels section.

The Case for L3Harris

L3Harris is well-positioned to profit from stable U.S. finances funding provisions. The corporate claims that its Hypersonic and Ballistic Monitoring House Sensor satellite tv for pc, often known as HBTSS, launched in February 2024, is the one confirmed on-orbit system able to monitoring the new-range hypersonic missiles. This could present it with a aggressive edge in turning into the first contractor for the Golden Dome program.

The corporate accomplished a $125 million enlargement at its house manufacturing facility in Fort Wayne, IN, in April 2025, to assist the Division of Protection’s pressing want for on-orbit know-how to defend the homeland by constructing the “Golden Dome.”

Whereas the corporate boasts a stable place within the U.S. protection house, its worldwide presence additionally stays vital. Evidently, throughout the third quarter of 2025, its worldwide revenues accounted for roughly 21.5% of its whole revenues.

Notably, L3Harris continues to witness sturdy demand for its defensive options from Asia-Pacific, Latin America and South America, in addition to the NATO allies of the USA. Wanting forward, L3Harris’ progress outlook within the worldwide market stays sturdy, with the NATO members now concentrating on protection spending will increase to five% of GDP.

Just lately, the corporate obtained an award price greater than $2.26 billion from South Korea to ship a fleet of next-generation airborne early warning enterprise jets utilizing the Bombardier International 6500 airplane. Evidently, throughout the third quarter, L3Harris and Joby Aviation introduced an settlement to discover a brand new plane class for protection purposes.

Regardless of the positives, HWM’s extremely leveraged stability sheet stays a significant concern. Exiting third-quarter 2025, L3Harris’ money and money equivalents amounted to $0.34 billion. Alternatively, its long-term debt of $11 billion remained above the money stability. Its present debt of $0.73 billion additionally got here in greater than its money reserve.

Persistent scarcity of labor within the aerospace-defense trade continues to pose a menace. Resulting from such labor shortages, manufacturing firms like L3Harris, which provide vital elements to the aerospace and protection trade, may be unable to ship the completed merchandise throughout the stipulated timeline, which can influence their efficiency.

The Zacks Consensus Estimate for HWM & LHX

The Zacks Consensus Estimate for HWM’s 2026 gross sales and earnings per share (EPS) implies year-over-year progress of 12.2% and 20.3%, respectively. HWM’s EPS estimates for 2026 have elevated over the previous 60 days.

Picture Supply: Zacks Funding Analysis

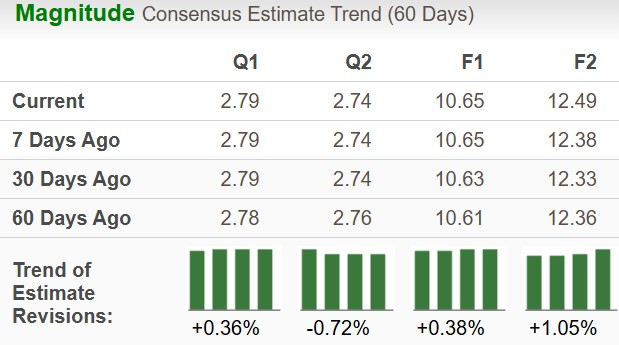

The Zacks Consensus Estimate for LHX’s 2026 gross sales and EPS signifies year-over-year progress of 6.4% and 17.3%, respectively. LHX’s EPS estimates have been trending northward over the previous 60 days for 2026.

Picture Supply: Zacks Funding Analysis

Worth Efficiency and Valuation

Up to now yr, Howmet shares have soared 79.5%, whereas L3Harris inventory has gained 58.8%.

Picture Supply: Zacks Funding Analysis

HWM is buying and selling at a ahead 12-month price-to-earnings ratio of fifty.12X, above its median of 31.79X during the last three years. LHX’s ahead earnings a number of sits at 27.55X, above its median of 16.54X over the identical timeframe.

Picture Supply: Zacks Funding Analysis

Ultimate Tackle HWM & LHX

Howmet and L3Harris at present have a Zacks Rank #3 (Maintain) every, which makes selecting one inventory a tough activity. You possibly can see the whole checklist of as we speak’s Zacks #1 Rank (Robust Purchase) shares right here.

L3Harris’ sturdy foothold in home and worldwide markets, together with a stable pipeline of tasks, is more likely to be useful in the long term. The corporate’s sturdy momentum within the aerospace and protection markets has been dented by the continued supply-chain challenges and labor shortages. Additionally, its excessive debt profile stays a significant constraint.

In distinction, Howmet’s market management place and energy in each industrial and protection aerospace markets present it with a aggressive benefit to leverage the long-term demand prospects within the aerospace market. Regardless of its steeper valuation, HWM holds sturdy prospects because of sturdy estimates, inventory worth appreciation and higher prospects for gross sales and revenue progress. Given these components, HWM appears to be a greater choose for traders than LHX at present.

#1 Semiconductor Inventory to Purchase (Not NVDA)

The unimaginable demand for knowledge is fueling the market’s subsequent digital gold rush. As knowledge facilities proceed to be constructed and always upgraded, the businesses that present the {hardware} for these behemoths will turn into the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to reap the benefits of the following progress stage of this market. It focuses on semiconductor merchandise that titans like NVIDIA do not construct. It is simply starting to enter the highlight, which is strictly the place you wish to be.

See This Inventory Now for Free >>

L3Harris Applied sciences Inc (LHX) : Free Inventory Evaluation Report

Howmet Aerospace Inc. (HWM) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.