The market liked Meta Platforms’ META quarterly outcomes however wasn’t impressed with Microsoft’s MSFT and Tesla’s TSLA December-quarter numbers.

The market’s disappointment with the Microsoft report however, the corporate delivered +28.1% earnings progress on +16.7% top-line beneficial properties for the interval, additionally handily beating estimates. The sticking level for buyers was Azure and different cloud providers income progress of +38% (in fixed forex phrases) and underwhelming steering for the present interval.

Worries about decelerating Azure progress have been weighing on Microsoft’s shares, as has the corporate’s relationship with OpenAI. Azure revenues had been up +39% every in fixed forex phrases in every of the previous two quarters, and the mid-point of steering for the March quarter represents a +37.5% progress tempo. Administration has flagged capability constraints as the first cause for the expansion deceleration, however market individuals don’t appear absolutely on board with that clarification.

Meta’s This autumn progress numbers are lots much less spectacular, with earnings and revenues up +9.3% and +23.8%, respectively, flagging the social-media bellwether’s margin pressures. However what impressed buyers is the corporate’s capacity to make use of AI extra successfully in its promoting enterprise. The notable AI-centric enchancment within the enterprise was the +3.5% improve in click on charges on its advertisements, leading to a +1% improve in conversion charges.

As with Microsoft, Meta claims to be capacity-constrained and unable to execute on all of the concepts it has to streamline their advert enterprise with the assistance of AI. It’s this argument that allowed the corporate to get away with an extra improve to its capex funds. They’re presently focusing on to spend $135 billion in capex this yr, up from $72 billion in 2025 and $39 billion in 2024.

We are going to see how the market reacts to experiences from Amazon AMZN and Alphabet GOOGL this week, with the previous reporting after the market’s shut on Thursday, February fifth, and the latter on Wednesday, February 4th. The expectation is that Amazon’s earnings could be up +5.7% on +12.7% greater revenues, whereas Alphabet’s quarterly earnings and revenues are anticipated to be up +17.5% and +16%, respectively.

The mixture progress numbers for the Magazine 7 group are spectacular, with This autumn earnings on monitor to be up +21.9% from the identical interval final yr on +18.1% greater revenues, following the group’s +28.3% earnings progress on +18.1% income progress in 2025 Q3. Not all members of the elite group are equally contributing to the expansion tempo, starting from Tesla’s -53.4% earnings decline in This autumn and Nvidia’s estimated +67.4% leap.

The chart under reveals the group’s blended This autumn earnings and income progress relative to what was achieved within the previous interval and what’s anticipated within the coming three intervals.

Picture Supply: Zacks Funding Analysis

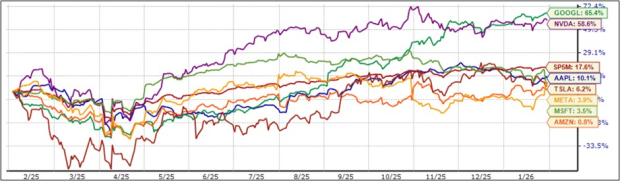

The chart under reveals the one-year efficiency of the Magazine 7 group, with Alphabet and Nvidia outperforming the market, whereas the remainder underperform.

Picture Supply: Zacks Funding Analysis

The chart under reveals the Magazine 7 group’s earnings and income progress image on an annual foundation.

Picture Supply: Zacks Funding Analysis

Please notice that the Magazine 7 group is on monitor to account for 25.2% of all S&P 500 earnings in 2025, up from 23.2% in 2024 and 18.3% in 2023. Concerning market capitalization, the Magazine 7 group presently carries a 34.2% weight within the index.

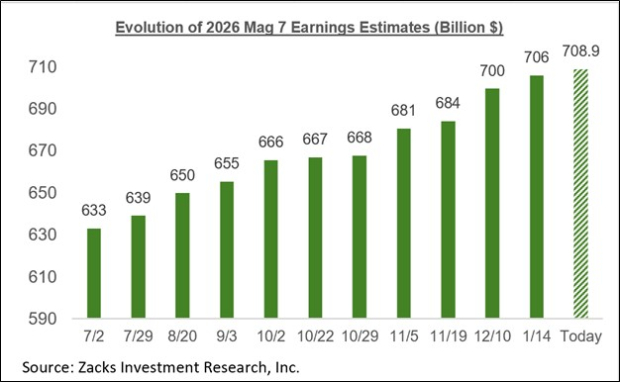

The Magazine 7 group has been having fun with a steadily enhancing earnings outlook, with analysts elevating their estimates. We noticed that development in play forward of the beginning of the Q3 earnings season, and one thing comparable is in place for 2025 This autumn as nicely.

The chart under reveals how combination earnings estimates for the Magazine 7 group have developed since July 2025.

Picture Supply: Zacks Funding Analysis

This autumn Earnings Season Scorecard

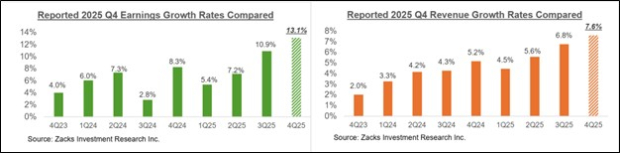

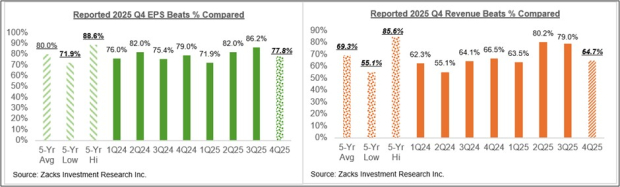

By means of Friday, January 30th, we have now seen This autumn outcomes from 167 S&P 500 members or 33.4% of the index’s complete membership. Whole earnings for these firms are up +13.1% from the identical interval final yr on +7.6% greater revenues, with 77.8% beating EPS estimates and 64.7% beating income estimates.

We’ve got greater than 450 firms on deck to report outcomes this week, together with 127 index members. The week’s lineup consists of, moreover the aforementioned Amazon and Alphabet experiences, a consultant cross-section of bellwether operators, together with Disney, Palantir, Pfizer, Eli Lilly, AMD, Chipotle, Uber, Qualcomm, Ralph Lauren, and others.

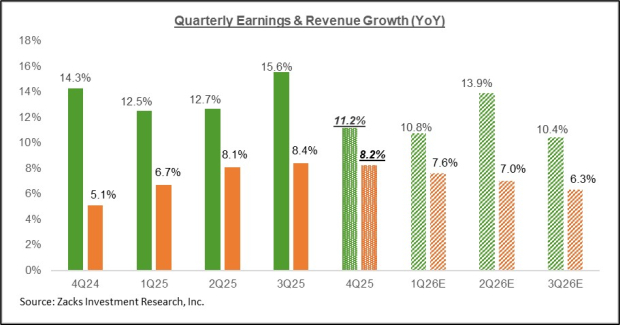

The comparability charts under put the expansion charges for these 167 index members as compared with what we had seen from this identical group of firms in different current intervals.

Picture Supply: Zacks Funding Analysis

The comparability charts under present the This autumn EPS and income beats percentages for this group of firms relative to what we had seen from them in different current intervals.

Picture Supply: Zacks Funding Analysis

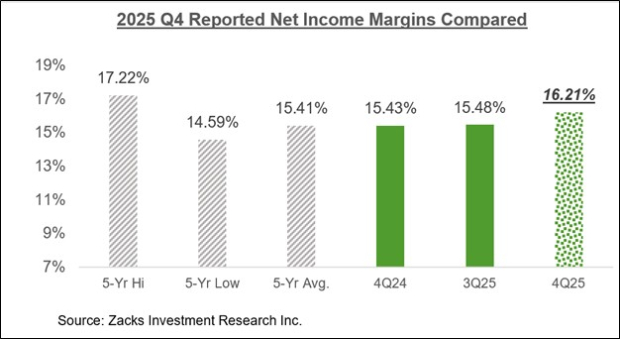

The comparability chart under places the This autumn web margins for the 167 firms which have reported in a historic context.

Picture Supply: Zacks Funding Analysis

As you may see above, earnings and income progress charges stay robust and accelerating, however the EPS and income beats percentages are on the weak aspect.

The Earnings Huge Image

The chart under reveals the This autumn earnings and income progress expectations within the context of the place progress has been within the previous 4 quarters and what’s anticipated within the coming three quarters.

Picture Supply: Zacks Funding Analysis

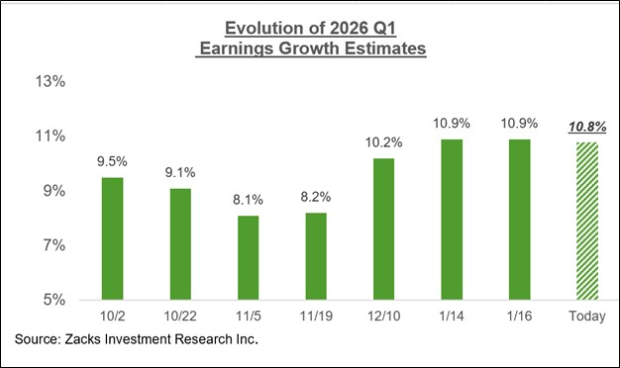

Estimates for the present interval (2026 Q1) have come underneath some strain in current days, because the chart under reveals.

Picture Supply: Zacks Funding Analysis

The above downtrend however, estimates have truly modestly elevated for 10 of the 16 Zacks sectors because the begin of January, together with Tech, Primary Supplies, Autos, Industrials, Transportation, and others. On the adverse aspect, estimates have come down for six of the 16 Zacks sectors, together with Vitality, Medical, Shopper Discretionary, and others.

The chart under reveals the general earnings image on a calendar-year foundation, with double-digit earnings progress anticipated in 2025 and 2026.

Picture Supply: Zacks Funding Analysis

For an in depth have a look at the general earnings image, together with expectations for the approaching intervals, please try our weekly Earnings Traits report >>>>Taking Inventory of the This autumn Earnings Season

5 Shares Set to Double

Every was handpicked by a Zacks professional as the favourite inventory to achieve +100% or extra within the months forward. They embrace

Inventory #1: A Disruptive Power with Notable Progress and Resilience

Inventory #2: Bullish Indicators Signaling to Purchase the Dip

Inventory #3: One of many Most Compelling Investments within the Market

Inventory #4: Chief In a Crimson-Scorching Business Poised for Progress

Inventory #5: Fashionable Omni-Channel Platform Coiled to Spring

A lot of the shares on this report are flying underneath Wall Avenue radar, which offers an incredible alternative to get in on the bottom ground. Whereas not all picks could be winners, earlier suggestions have soared +171%, +209% and +232%.

See Our Latest 5 Shares Set to Double Picks >>

Amazon.com, Inc. (AMZN) : Free Inventory Evaluation Report

Microsoft Company (MSFT) : Free Inventory Evaluation Report

Tesla, Inc. (TSLA) : Free Inventory Evaluation Report

Alphabet Inc. (GOOGL) : Free Inventory Evaluation Report

Meta Platforms, Inc. (META) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.