In a single morning, the U.S. authorities dropped two large items of information: the up to date scorecard for financial progress (GDP) and the Federal Reserve’s absolute favourite inflation gauge (the Core PCE worth index).

The difficult half was that progress regarded mushy, however inflation was nonetheless stubbornly excessive.

Let’s break down what the stories confirmed, how they might form the Fed’s subsequent transfer, and what all of it means on your trades.

The GDP Downshift: Muscle vs. Mirage

The Bureau of Financial Evaluation (BEA) launched its second estimate of Q1 2026 gross home product — the revised model, incorporating extra full information on commerce, companies, and inventories. Actual GDP elevated at an annualized fee of 1.6% in Q1 2026, down from the two.0% advance estimate and under the two.0% market consensus.

A newcomer to macro would possibly see that and assume: financial system slowing, greenback weakening, promote every little thing. Not so quick.

The downward revision was nearly completely a technical story. Corporations drew down current inventories quicker than they restocked, which mechanically dragged the headline decrease. Strip that out and take a look at actual ultimate gross sales to non-public home purchasers — the “muscle” of the financial system, measuring what shoppers and companies are literally spending — and that determine got here in at 2.4%, revised down solely 0.1 proportion level from the earlier estimate.

So, the underlying demand is holding. The headline simply seems to be softer than the truth beneath it.

The Core PCE Thermometer: A Cussed Flame

Whereas GDP was doing its stock shuffle, the April Private Consumption Expenditures (PCE) report confirmed that worth pressures will not be going away quietly.

Headline PCE, which incorporates meals, vitality, lease, and every little thing else, rose to three.8% y/y from 3.5% in March. A part of that bounce got here from Iran conflict-driven vitality costs, which the Fed often tries to look previous.

The actual headache is core PCE, which strips out meals and vitality to point out the underlying inflation pattern. Core PCE rose to three.3% yr over yr in April from 3.2% in March. The Fed desires inflation at 2%, so 3.3% continues to be approach too sizzling. That’s not a hearth that’s nearly out. That’s a hearth that has determined it pays lease now.

There was one little bit of reduction. Month-to-month core PCE got here in at 0.2%, softer than the 0.3% forecast.

The Fed’s Dilemma: Trapped in “Greater for Longer”

Put the 2 stories collectively and the Fed’s downside will get fairly clear.

If GDP had slowed to 1.6% as a result of People stopped spending, the Fed would have a clear case for cuts. However underlying demand continues to be working at 2.4%, so the financial system doesn’t precisely want rescuing. In the meantime, core PCE at 3.3% means reducing now can be like tossing dry wooden onto a hearth that refuses to die.

That helps clarify why the FOMC has held charges at 3.50% to three.75% for 3 straight conferences. April additionally introduced uncommon disagreement, with three members pushing to take away the easing bias and most officers signaling hikes may turn out to be acceptable if inflation stays above 2%.

Markets now see a 57% probability of not less than one hike by December, in keeping with CME FedWatch. In the beginning of 2026, merchants had been pricing in two or three cuts. Humorous what a Strait of Hormuz shock can do.

Then there’s Kevin Warsh. Sworn in as Fed Chair on Might 22, Warsh had argued that AI-driven productiveness features may justify simpler coverage. That case hasn’t aged effectively. His first FOMC assembly is June 16 to 17, and whereas Warsh could favor cuts, his committee is sounding extra hawkish. That conflict factors to coverage uncertainty, which often means choppier currencies and tougher to carry traits.

Promoted: Uneven Fed Weeks Want Extra Than Good Guesses.

Delicate GDP, sticky Core PCE, and a divided Fed can flip even stable commerce concepts right into a stress check. FTMO offers expert merchants entry to bigger simulated capital, to allow them to give attention to execution as an alternative of forcing large outcomes from a small account.

Be taught extra about FTMO!

Disclosure: To assist help our content material, we could earn a fee from our companions for those who join by means of our hyperlinks, at no additional value to you.

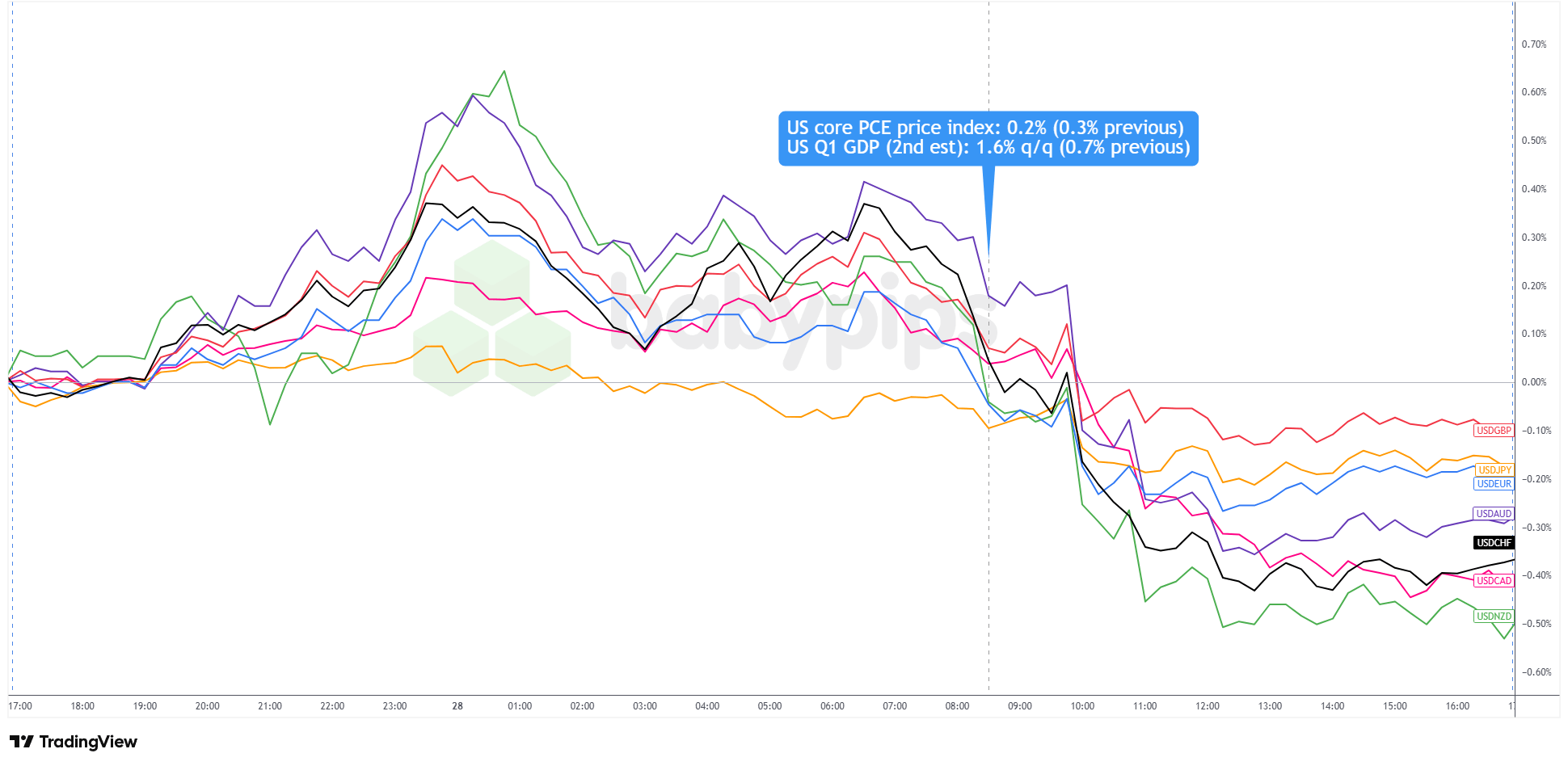

The Greenback’s Divided Response

Thursday’s greenback session confirmed the tug of battle in actual time. The Buck gained floor in Asia after Iran launched missiles and drones at Kuwait and a US air base, triggering basic protected haven demand. However softer month-to-month PCE, together with stories of an Iran ceasefire extension, knocked the greenback again down by the shut.

USD 15-Minute Foreign exchange – Chart Sooner With TradingView

Commodity-linked currencies led the rebound, with AUD, CAD, and NZD benefiting from the improved danger temper. EUR and GBP additionally firmed, whereas Treasury yields fell throughout the curve.

The takeaway is that the greenback was being pulled by three forces without delay. Charge expectations matter for EUR/USD and GBP/USD, danger sentiment issues extra for AUD, NZD, and CAD, and protected haven demand retains USD/JPY and USD/CHF difficult.

Fast Takeaways

- Q1 GDP revised to 1.6%, however underlying home demand held at 2.4% — the headline seems to be weaker than the financial system truly is.

- April core PCE caught at 3.3% y/y, effectively above the Fed’s 2% goal; the month-to-month print of 0.2% was one-tenth softer than forecast, which is what moved markets Thursday.

- The Fed can’t lower — underlying progress doesn’t demand it, and inflation doesn’t allow it. “Greater for longer” is the default setting.

- New Chair Warsh faces his first FOMC check June 16–17. Whether or not the easing bias is formally dropped — and what he says on the press convention — could transfer the greenback advanced greater than the speed determination itself.

- USD weak spot on Thursday was broad however uneven: commodity currencies led, EUR and GBP noticed some demand, and safe-haven pairs stayed caught within the center.

What to Watch Subsequent

- June 5 (Thursday): Might Non-Farm Payrolls — a sizzling quantity reinforces the hike case; a mushy one complicates an already divided Fed.

- June 10 (Tuesday): Might CPI — the final main inflation print earlier than the FOMC, and certain the deciding enter for Warsh’s opening act.

- June 16–17: FOMC determination and Warsh’s first press convention. The assertion language issues as a lot as the speed name itself.

This text digs into the GDP and Core PCE information and what they imply for Fed coverage, but when the mechanics of inflation gauges like PCE are unfamiliar, our lesson covers precisely that. Premium members can learn our lesson:

📖 Inflation: The Drive That Strikes Central Banks

Studying this helps you perceive how CPI, PCE, and PPI measure inflation, why the Fed targets 2%, and the way inflation regimes form foreign money values and buying and selling choices.