Buyers trying to purchase beaten-down tech shares in June with long-term upside may need to take into account Veeva Methods VEEV.

The life sciences-focused cloud software program inventory is down round 45% from its peak, implying roughly 80% upside if it ever returns to its 2021 highs. VEEV studies its Q1 fiscal 12 months 2027 monetary outcomes after the inventory market closes on Wednesday, June 3.

There are authentic issues surrounding Veeva, together with rising competitors, slowing development, and mounting fears that AI will progressively make its pharmaceutical and life sciences enterprise software program choices out of date.

That stated, Veeva inventory jumped 8% on Monday to cross above a doubtlessly key long-term technical stage after discovering help close to the underside of the buying and selling vary it’s been in for the final six years.

Picture Supply: Zacks Funding Analysis

Veeva’s common Zack value goal marks round 45% upside from its present ranges, and it’s projected to submit double-digit earnings and income development this 12 months and subsequent.

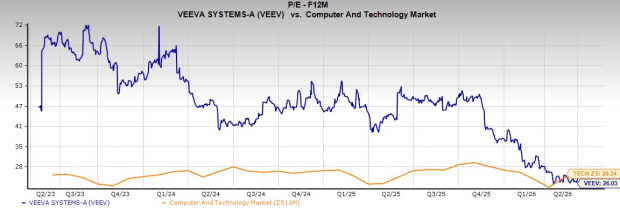

The downturn, combined with its robust earnings development outlook, has it buying and selling in step with the Tech sector and over 80% beneath its highs by way of ahead earnings.

Purchase this Tech Inventory Now for 80% Upside Potential

Veeva is a cloud software program firm targeted totally on the pharmaceutical and life sciences industries. VEEV helps shoppers enhance and streamline vital enterprise capabilities, with software program and providers for analysis and growth, regulatory processes and compliance, security, medical trials, advertising and marketing, and past.

Picture Supply: Zacks Funding Analysis

The corporate steadily expanded its attain during the last decade-plus, serving to its shoppers thrive within the new digital the whole lot world. Veeva in late 2022, introduced that it will transition away from its long-term partnership settlement with Salesforce (CRM) when it expired in 2025.

Extra importantly, Veeva laid out plans emigrate clients from its legacy Veeva CRM (constructed on Salesforce) to its next-generation Vault CRM platform. Veeva can be actively increasing industry-specific AI choices, together with its AI brokers.

That stated, Wall Avenue has punished the inventory as a result of its days of 25% to 35% development resulted in FY22. Wall Avenue has authentic fears that the fast enlargement and evolution of synthetic intelligence may eat away on the complete enterprise software program market.

Picture Supply: Zacks Funding Analysis

Veeva faces head-to-head competitors with Salesforce after its break up. Buyers additionally received spooked when VEEV stated in November 2025 that it expects 14 of the highest 20 international pharmaceutical corporations to undertake its next-generation Vault CRM product, which dissatisfied Wall Avenue because it was fewer than these utilizing the legacy Veeva CRM platform.

Purchase this Inventory for Progress, Worth, and AI Upside?

Nonetheless, the corporate grew its income by 16% for the second straight 12 months in FY26 (interval ended January 31). VEEV is projected to develop its FY27 income by ~13% after which submit ~12% development in FY28 to climb from $3.20 billion final 12 months to $4.01 billion subsequent 12 months.

Picture Supply: Zacks Funding Analysis

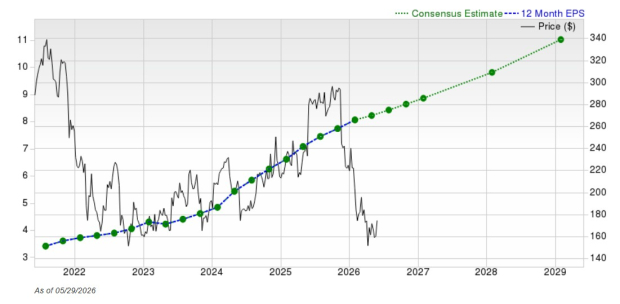

The biopharma software program firm is projected to develop its adjusted earnings by over 9% this 12 months and 11% subsequent 12 months, following 23% enlargement in FY26. VEEV has overwhelmed our bottom-line estimate for 5 years operating. The chart above showcases its robust long-term earnings development outlook

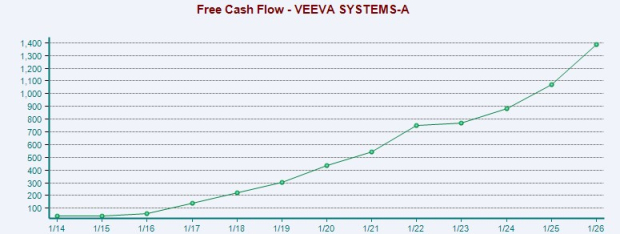

The corporate can be a money cow, producing a ton of free money move, together with 30% YoY development in FY26.

Plus, Veeva’s stability sheet is stellar, with $6.6 billion in money and equivalents and $9 billion in complete property in opposition to zero debt, and $1.8 billion in complete liabilities. This backdrop provides the medical software program firm the flexibility to consistently pursue extra natural development alternatives throughout AI and past, and make strategic acquisitions.

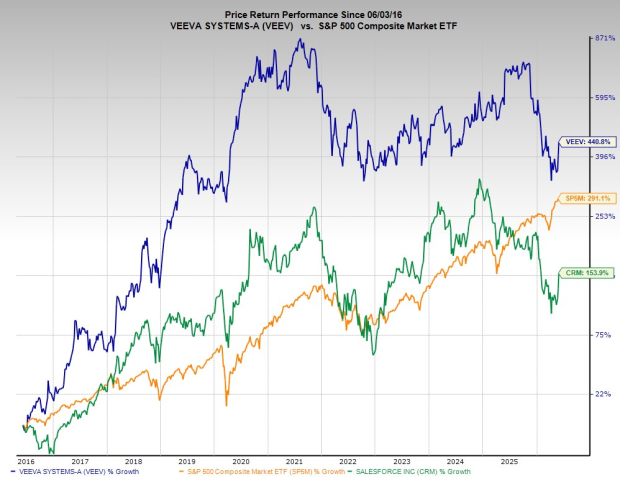

VEEV inventory has climbed 440% up to now decade, lagging Tech’s 540%, however topping the S&P 500’s 290% and crushing Salesforce’s 150%. This market and CRM-beating efficiency consists of its ~45% drop from its 2021 peaks.

Picture Supply: Zacks Funding Analysis

It’s buying and selling round the place it was in April 2020, whereas providing ~80% upside if it have been to ever return to its peaks. Veeva inventory climbed above its 21-week transferring common after Monday’s 8% surge.

Veeva is on the verge of a possible technical breakout. Plus, its downturn combined with is robust earnings development outlook has it buying and selling in step with the Tech sector and over 80% beneath its highs at 26X ahead 12-month earnings.

Radical New Expertise May Hand Buyers Big Beneficial properties

Quantum Computing is the subsequent technological revolution, and it could possibly be much more superior than AI.

Whereas some believed the know-how was years away, it’s already current and transferring quick. Massive hyperscalers, reminiscent of Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to combine quantum computing into their infrastructure.

Senior Inventory Strategist Kevin Cook dinner reveals 7 rigorously chosen shares poised to dominate the quantum computing panorama in his report, Past AI: The Quantum Leap in Computing Energy.

Kevin was among the many early consultants who acknowledged NVIDIA’s huge potential again in 2016. Now, he has keyed in on what could possibly be “the subsequent massive factor” in quantum computing supremacy. At the moment, you might have a uncommon probability to place your portfolio on the forefront of this chance.

See Prime Quantum Shares Now >>

Salesforce, Inc. (CRM) : Free Inventory Evaluation Report

Veeva Methods Inc. (VEEV) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.