Because the Q1 earnings season heats up, two of retail’s greatest names — Goal Company TGT) and Walmart Inc. WMT) — are as soon as once more underneath the highlight.

Each firms dominate the U.S. retail panorama, serve hundreds of thousands of shoppers each day, and supply buyers publicity to defensive client spending tendencies. But regardless of working in the identical sector, the 2 retail giants are heading into earnings with very completely different momentum profiles.

Walmart has emerged as one of many market’s strongest large-cap retail performers over the previous 12 months, fueled by grocery dominance, e-commerce growth, and rising traction amongst higher-income consumers. Goal, in the meantime, continues to work via slowing discretionary demand, stock normalization efforts, and margin pressures which have weighed on investor sentiment.

That stated, their Q1 outcomes will probably be intently watched this week, with Goal set to report on Wednesday, Might 20, and Walmart reporting on Thursday, Might 21.

Goal & Walmart’s Q1 Expectations

The Zacks Consensus requires Goal’s Q1 gross sales to be up 2% 12 months over 12 months to $24.46 billion, with quarterly earnings anticipated to rise 5% to $1.37 per share.

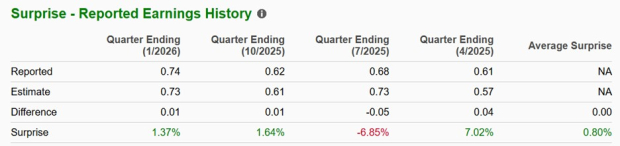

Nonetheless, Goal has missed top-line expectations in three of its final 4 quarterly reviews with a mean gross sales shock of -0.23%. Whereas Goal has put collectively a string of consecutive earnings beats, the corporate has posted a mean EPS shock of -2.02% over the past 4 quarters.

Picture Supply: Zacks Funding Analysis

Pivoting to Walmart, Q1 gross sales are thought to have elevated 5% to $174.56 billion, with quarterly EPS anticipated to be up 6% to $0.65.

Walmart has exceeded top-line estimates for twenty-four consecutive quarters with a mean gross sales shock of 0.68% over the past 4 quarters. Moreover, Walmart has exceeded earnings expectations in three of its final 4 quarterly reviews, with a mean EPS shock of 0.8%.

Picture Supply: Zacks Funding Analysis

Walmart Continues to Win on Stability and Scale

Coming into the earnings season from a place of energy, Walmart has persistently delivered strong comparable-sales progress, benefiting from shoppers prioritizing necessities and value-oriented buying amid persistent financial uncertainty.

Its grocery enterprise stays a significant aggressive benefit. Since meals purchases are non-discretionary, Walmart has loved regular visitors at the same time as shoppers reduce in different retail classes. The corporate has additionally efficiently expanded its enchantment past lower-income households, attracting center and upper-income shoppers searching for affordability.

As well as, Walmart’s digital transformation continues to achieve momentum. E-commerce gross sales progress, promoting income, and membership packages like Walmart+ have grow to be more and more vital drivers of revenue. These higher-margin companies are offsetting stress from its historically low-margin retail operations.

Analysts are additionally optimistic about Walmart’s capability to navigate inflationary environments. The retailer’s huge scale provides it pricing leverage with suppliers, whereas its operational effectivity helps protect margins higher than many opponents.

From a stock-performance perspective, Walmart has rewarded shareholders with stronger beneficial properties in recent times, considerably outperforming Goal and far of the broader retail sector.

Picture Supply: Zacks Funding Analysis

Goal Faces a Extra Difficult Setup

As for Goal, its storyline heading into its Q1 report is extra difficult.

Not like Walmart, Goal generates a bigger portion of income from discretionary classes reminiscent of residence items, attire, and electronics — areas the place client spending has softened significantly. As inflation and better rates of interest proceed to stress family budgets, consumers have more and more shifted spending towards requirements and away from discretionary purchases.

That pattern has created a troublesome working atmosphere for Goal over the previous a number of quarters.

Whereas Goal has made progress on stock administration after main overstock points damage profitability in prior years, gross sales progress stays sluggish in comparison with Walmart, and buyers proceed to query how shortly Goal can reignite constant visitors and discretionary demand.

Goal has additionally confronted margin volatility as a result of elevated promotional exercise and ongoing investments in retailer operations and supply-chain enhancements.

Nonetheless, there are causes for optimism as Goal’s model stays extremely differentiated inside retail. Its partnerships, private-label portfolio, and robust buyer loyalty present long-term benefits which might be onerous to miss.

If client spending tendencies stabilize later this 12 months, Goal may doubtlessly see stronger recovery-driven upside than Walmart.

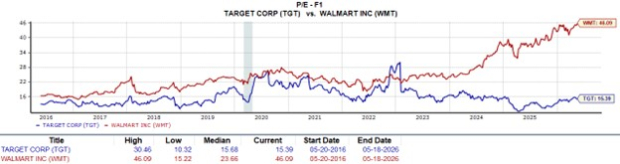

Valuation May Change into the Key Differentiator

When deciding between these two retail giants, the most important debate for buyers proper now might heart on valuation. This will actually tip the scales, as Goal’s valuation seems considerably extra enticing relative to Walmart’s premium a number of.

Walmart’s operational execution has been glorious, however a lot of that energy might already be mirrored within the inventory worth. Shares presently commerce at a notably increased ahead earnings a number of than historic averages at 46X, suggesting buyers are already pricing in continued progress and defensive resilience.

Goal, then again, trades at a a lot decrease ahead P/E valuation of 15X as a result of weaker operational efficiency and diminished investor confidence.

For value-oriented buyers, that creates an attention-grabbing setup. If Goal can ship even modest upside surprises in visitors tendencies, margins, or ahead steerage, its inventory may have extra room for a number of growth.

Protecting this state of affairs in thoughts, Walmart should still be the safer funding, however Goal arguably presents the larger rebound potential.

Picture Supply: Zacks Funding Analysis

Including to Goal’s worth and making up for its subpar inventory efficiency is a really attractive 3.7% annual dividend yield in comparison with Walmart’s 0.74%.

Picture Supply: Zacks Funding Analysis

Underlying Metrics Buyers Ought to Watch This Earnings Season

As Q1 outcomes method, a number of metrics will doubtless decide investor response for each firms:

Walmart

- Comparable-store gross sales progress

- Grocery market-share beneficial properties

- E-commerce progress tendencies

- Walmart+ membership momentum

- Working margin stability

- Shopper spending commentary

Goal

- Comparable-sales efficiency

- Stock ranges

- Gross-margin restoration

- Discretionary class demand

- Site visitors and transaction tendencies

- Full-year steerage updates

Administration commentary about client habits might show particularly vital this quarter, as buyers seek for clues in regards to the well being of the U.S. client and broader retail atmosphere.

Which Inventory Seems to be Just like the Higher Funding?

For conservative, long-term buyers searching for stability, Walmart presently seems to be the stronger alternative heading into earnings. Walmart’s scale, grocery dominance, digital growth, and defensive enterprise mannequin proceed to assist constant progress even in unsure financial circumstances.

Nonetheless, for buyers prepared to just accept extra danger in trade for potential upside, Goal might supply the extra intriguing alternative. To that time, Goal’s discounted valuation and restoration potential may create enticing returns if discretionary spending tendencies enhance and administration executes successfully.

As Q1 earnings close to, each shares land a Zacks Rank #3 (Maintain) and will probably be intently watched bellwethers for the retail sector — and for the well being of the American client total.

Past Nvidia: AI’s Second Wave Is Right here

The AI revolution has already minted millionaires. However the shares everybody is aware of about aren’t more likely to maintain delivering the most important income. AI’s second wave is shifting from infrastructure to implementation and these firms are on the forefront of this transition, positioned to grow to be what Amazon and Google had been to the web period.

Goal Company (TGT) : Free Inventory Evaluation Report

Walmart Inc. (WMT) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.