The 2025 This autumn earnings season is quickly flying by, with all Magnificent 7 members already delivering their outcomes outdoors of beloved NVIDIA. The interval has up to now been optimistic, with progress remaining sturdy and a stable variety of firms exceeding quarterly expectations.

Regarding some winners of the cycle up to now, Boot Barn BOOT and Cardinal Well being CAH each raised steerage in a technique or one other, with every additionally seeing favorable post-earnings reactions.

Boot Barn Sees Sturdy Margin Efficiency

Boot Barn posted sturdy ends in its launch, with gross sales climbing 16% year-over-year alongside a 5.7% cost increased in similar retailer gross sales. The identical retailer gross sales progress is especially notable, telling us that its present shops are seeing sturdy efficiency whereas it additionally continues to open new areas.

Beneath is a chart illustrating Boot Barn’s gross sales on a quarterly foundation, with the latest $705.6 million print reflecting a quarterly report.

Picture Supply: Zacks Funding Analysis

Regarding retailer openings, the corporate opened 25 new areas all through the intervals, bringing its total tally as much as 514 at quarter finish. BOOT additionally loved an improved profitability image, with its gross margin rising to 39.9% vs. a 39.3% print in the identical interval final yr. Client-focused shares, significantly retail, are sometimes extremely delicate to margin efficiency, serving to clarify the sturdy post-earnings response and information increased.

BOOT’s margins image has remained optimistic for a number of intervals now, seeing good enlargement off 2023 lows. Please notice that the chart under is on a trailing twelve-month foundation.

Picture Supply: Zacks Funding Analysis

Boot Barn now expects to open 70 new shops in its FY26, with gross sales additionally anticipated to succeed in a band of $2.24 – $2.25 billion. Identical retailer gross sales progress is forecasted to be in a variety of 6.5% – 7.5%, persevering with its latest streak of momentum properly.

And to prime it off, the inventory sports activities the highly-coveted Zacks Rank #1 (Sturdy Purchase), with EPS expectations notably bullish for the above-mentioned FY26.

Picture Supply: Zacks Funding Analysis

Cardinal Well being Sees Broad Power

Cardinal Well being posted a double-beat relative to our consensus expectations, with gross sales hovering 18.8% from the year-ago interval alongside a large 36.3% year-over-year progress fee in adjusted EPS.

Cardinal Well being’s gross sales have seen nice progress over latest intervals after some stagnation all through 2024, as proven under within the chart that illustrates CAH’s gross sales on a quarterly foundation.

Picture Supply: Zacks Funding Analysis

Power was primarily broad-based throughout its segments, with gross sales in Prescribed drugs and Specialty Options climbing 19% year-over-year. Its World Medical Merchandise and Distribution noticed its gross sales develop 3% YoY, whereas its ‘Different’ phase (contains at-home options, OptiFreight Logistics, and Nuclear and Precision Well being Options) noticed a powerful 34% year-over-year climb. It’s value noting that its Prescribed drugs and Specialty Options accounts for the overwhelming majority of its gross sales, contributing roughly 90%.

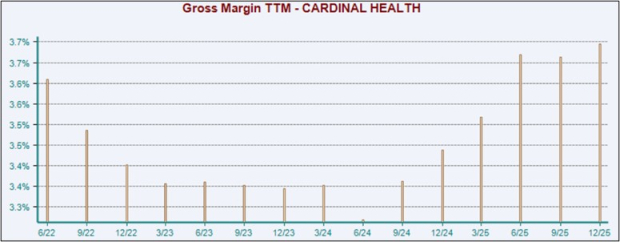

Just like BOOT above, Cardinal Well being has seen its margins recuperate properly over latest intervals, as proven under. Please notice that the chart tracks margins on a trailing twelve-month foundation.

Picture Supply: Zacks Funding Analysis

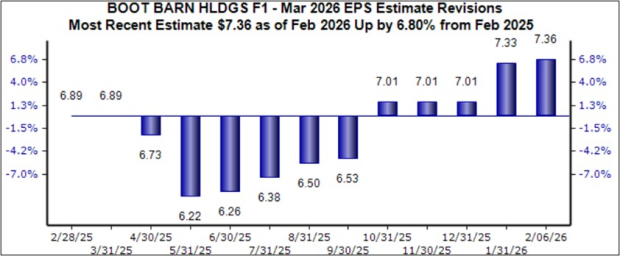

Cardinal Well being raised its FY26 outlook following the sturdy quarter, now anticipating adjusted EPS in a band of $10.15 – $10.35, with the midpoint suggesting 24.5% year-over-year progress. The up to date outlook is mirrored in optimistic earnings estimate revisions, as proven under. The inventory sports activities a positive Zacks Rank #2 (Purchase).

Picture Supply: Zacks Funding Analysis

Placing All the pieces Collectively

Steering upgrades are a typical signal of near-term outperformance, significantly when a positive Zacks Rank is concerned. Each shares above – Boot Barn BOOT and Cardinal Well being CAH – have skilled simply that, posting sturdy quarterly outcomes and having fun with optimistic post-earnings earnings estimate revisions along with their sturdy post-earnings reactions.

Zacks Names #1 Semiconductor Inventory

This under-the-radar firm makes a speciality of semiconductor merchandise that titans like NVIDIA do not construct. It is uniquely positioned to benefit from the following progress stage of this market. And it is simply starting to enter the highlight, which is strictly the place you wish to be.

With sturdy earnings progress and an increasing buyer base, it is positioned to feed the rampant demand for Synthetic Intelligence, Machine Studying, and Web of Issues. World semiconductor manufacturing is projected to blow up from $452 billion in 2021 to $971 billion by 2028.

See This Inventory Now for Free >>

Cardinal Well being, Inc. (CAH) : Free Inventory Evaluation Report

Boot Barn Holdings, Inc. (BOOT) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.