Dycom Industries, Inc. DY is at present buying and selling above the Constructing Merchandise – Heavy Development business friends and the broader Development sector, with a ahead 12-month price-to-earnings (P/E) ratio of 24.66. The business’s common at present is 22.68, whereas the sector’s valuation is nineteen.9.

Though the traders’ judgment is clouded by the premium valuation of the DY inventory for the close to time period, the mid- and long-term prospects of the agency look promising amid the continued market tailwinds. Dycom is primarily benefiting from the rising demand for fiber and digital infrastructure, pushed by elevated information heart initiatives. Other than this, the continued optimism in regards to the Broadband Fairness, Entry and Deployment (BEAD) funding initiatives, declining borrowing charges and accretive buyouts are pushing the sail additional amid the difficult macroeconomic tide.

Picture Supply: Zacks Funding Analysis

Previously three months, shares of this specialty contracting agency working within the telecom business have gained 19.1%, outperforming the business, the sector and the S&P 500 Index.

DY’s Worth Efficiency

Picture Supply: Zacks Funding Analysis

Let’s decode the components which are driving Dycom inventory’s momentum.

Strong Demand For Fiber

The telecommunications infrastructure surroundings is increasing as hyperscalers and huge expertise corporations spend money on long-haul and middle-mile fiber networks to help rising information utilization and new compute necessities. Dycom is extensively benefiting from this favorable development and is well-positioned to proceed benefiting within the mid and long run as properly. As of October 2025, DY’s complete backlog grew 4.7% yr over yr to $8.22 billion, with the subsequent 12-month backlog rising 11.4%.

The corporate believes that the market is within the early levels of a generational deployment of digital infrastructure, with the development of latest outdoors plant information heart networks to ramp up in calendar yr 2026. These prospects favor its long-term progress (continued growth into 2027 and past), given its experience in dealing with extremely complicated and large-scale builds. Through the first 9 months of fiscal 2026, Dycom’s contract revenues grew 13% yr over yr to $4.09 billion, pushed by strong demand for telecommunications and digital infrastructure, fueled by accelerating fiber builds and a large ramp-up in information heart wants.

Market Tailwinds Bode Effectively

The optimism surrounding the BEAD program and declining Fed rates of interest bode properly for Dycom. The BEAD program represents a big multi-year catalyst, with $29.5 billion in anticipated state and territory spending and roughly $26 billion directed particularly towards fiber or HFC infrastructure, an space straight aligned with Dycom’s core capabilities. About two-thirds of all BEAD-funded areas shall be served utilizing these applied sciences, increasing DY’s addressable market over the subsequent four-plus years. With deep relationships throughout carriers and long-standing engagement with states on deployment planning, the corporate is properly located to seize a significant share of BEAD-driven rural broadband building.

Furthermore, the three back-to-back Fed price cuts are appearing as a catalyst in boosting prospects additional. On Dec. 10, 2025, the Federal Reserve slashed its rates of interest by one other 0.25 proportion factors, setting the benchmark between 3.5% and three.75%. The declining borrowing charges catalyze extra undertaking funding in an already-booming public infrastructure spending state of affairs.

Upbeat This fall & Fiscal 2026 View

As a consequence of strong digital infrastructure progress and long-term demand drivers, Dycom laid out an upbeat fourth-quarter and financial 2026 outlook. For the fiscal fourth quarter, it expects contract revenues between $1.26 billion and $1.34 billion, up from $1.085 billion reported within the year-ago quarter. Adjusted EBITDA is anticipated to be between $140 million and $155 million, implying progress from $116.4 million reported a yr in the past. Additionally, adjusted earnings per share (EPS) for the fiscal fourth quarter are anticipated within the vary of $1.62-$1.97, up from $1.17 reported within the prior-year quarter.

For fiscal 2026, Dycom now expects complete contract revenues within the vary of $5.350-$5.425 billion (prior expectation was $5.290-$5.425 billion), suggesting a 13.8-15.4% year-over-year improve.

Earnings Estimate Development Favors DY

Dycom’s earnings estimates for fiscal 2026 and financial 2027 have trended upward over the previous 30 days. The estimated figures for fiscal 2026 and financial 2027 indicate year-over-year progress of 26.9% and 35%, respectively.

Picture Supply: Zacks Funding Analysis

The strong market fundamentals and DY’s strategic in-house capabilities doubtless induced bullish sentiments amongst analysts.

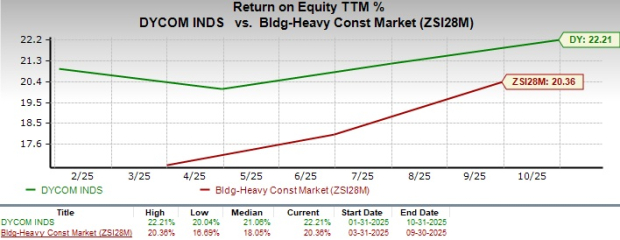

ROE for Dycom Inventory

Dycom’s trailing 12-month return on fairness (ROE) of twenty-two.2% considerably exceeds the business’s common, underscoring its effectivity in producing shareholder returns.

Picture Supply: Zacks Funding Analysis

Dycom’s Aggressive Place

Dycom is rising as some of the direct beneficiaries of the subsequent multi-year U.S. fiber and digital infrastructure construct cycle. Nevertheless, this doesn’t alter the aggressive facet on this huge market with key gamers, together with EMCOR Group, Inc. EME, Quanta Providers, Inc. PWR and MasTec, Inc. MTZ.

EMCOR is strongest inside the info heart footprint, notably in mechanical and electrical techniques, however has restricted publicity to outside-plant fiber networks and BEAD-funded rural broadband. Contrastingly, Quanta affords a broader scale and deeper publicity to energy transmission, renewable vitality and long-haul infrastructure. Quanta’s benefit is resilience throughout cycles, however its upside from BEAD and last-mile fiber is much less concentrated than Dycom’s.

MasTec competes carefully with Dycom in communications infrastructure and has significant fiber publicity, notably by massive nationwide provider applications. Nevertheless, MasTec’s earnings volatility, capital depth and publicity to vitality building dilute the purity of its fiber and information heart thesis relative to Dycom’s more and more centered technique.

Summing up, Dycom stands out as probably the most leveraged pure-play on U.S. fiber growth, BEAD funding and hyperscaler-driven information heart networking. Alternatively, the friends EMCRO, Quanta and MasTec supply broader, however much less focused, infrastructure publicity.

Ought to You Purchase the Premium-Valued DY Inventory Now?

Dycom continues to profit from highly effective secular tailwinds tied to U.S. fiber deployment, hyperscaler-driven information heart networking and government-backed broadband growth. Rising demand for long-haul, middle-mile and last-mile fiber has pushed backlog progress, with the next-12-month backlog up double digits yr over yr. This backdrop underpins Dycom’s upbeat fourth-quarter and financial 2026 steerage, pointing to stable top-line progress and increasing EBITDA. Additionally, the multi-year BEAD funding program and declining rates of interest additional improve undertaking funding visibility.

Though the DY inventory at present trades at a premium in comparison with the business and the development sector, its accelerating progress outlook and bettering earnings visibility help a bullish stance. Notably, a powerful ROE highlights disciplined execution and capital effectivity.

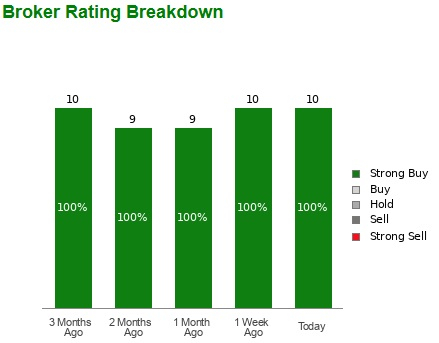

Analysts’ optimism relating to DY inventory is mirrored in 10 suggestions pointing to a “Sturdy Purchase”, representing 100% of all suggestions.

Picture Supply: Zacks Funding Analysis

Dangers embody execution complexity on massive initiatives and a premium valuation. Nonetheless, centered publicity to fiber and digital infrastructure, mixed with robust earnings momentum, makes this present Zacks Rank #1 (Sturdy Purchase) inventory enticing for traders looking for long-term progress. You possibly can see the whole checklist of at present’s Zacks #1 Rank shares right here.

#1 Semiconductor Inventory to Purchase (Not NVDA)

The unbelievable demand for information is fueling the market’s subsequent digital gold rush. As information facilities proceed to be constructed and continually upgraded, the businesses that present the {hardware} for these behemoths will turn out to be the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to make the most of the subsequent progress stage of this market. It focuses on semiconductor merchandise that titans like NVIDIA do not construct. It is simply starting to enter the highlight, which is strictly the place you wish to be.

See This Inventory Now for Free >>

Quanta Providers, Inc. (PWR) : Free Inventory Evaluation Report

EMCOR Group, Inc. (EME) : Free Inventory Evaluation Report

Dycom Industries, Inc. (DY) : Free Inventory Evaluation Report

MasTec, Inc. (MTZ) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.