Costco is about to shut out one other busy week of retail earnings when it experiences fiscal third-quarter outcomes on Thursday after the market closes. Not like most of its friends, the Issaquah-based warehouse membership walks into the print with the majority of the quarter’s narrative already written.

The corporate’s April gross sales launch on Might 6th disclosed internet gross sales of $23.92 billion for the 4 weeks ended Might 3rd, up 13.0% year-over-year, with comparable gross sales rising 11.6% on a reported foundation and seven.8% excluding gasoline and overseas change results.

That follows a March print of +9.4% whole comparable gross sales (+6.2% ex-gas/FX), giving traders a near-complete image of the 12-week quarter earlier than administration ever takes the stage on the earnings name. With the inventory pulling again from a latest 52-week excessive, the setup stays compelling.

Picture Supply: StockCharts

Digging Deeper into Costco’s Upcoming Announcement

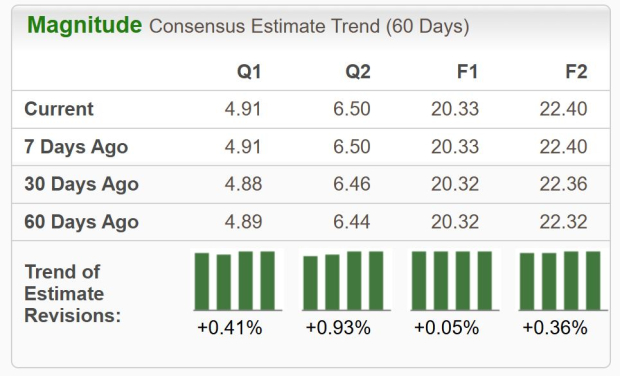

The Zacks Consensus Estimate for the quarter is at the moment pegged at $4.91 in EPS and roughly $69.5 billion in income, implying year-over-year progress of round 15% on the underside line and roughly 10% on the highest line versus the prior-year interval. The consensus pattern reveals estimates have risen barely over the previous 60 days.

Picture Supply: Zacks Funding Analysis

Importantly, Costco has now overwhelmed Zacks Consensus EPS estimates in a majority of its trailing quarters, although administration’s conservative steerage philosophy means surprises are typically measured relatively than dramatic.

The competitor read-through into this print is especially informative. Walmart’s fiscal first-quarter launch final week confirmed Sam’s Membership U.S. comparable gross sales of +3.9% excluding gas — a significant deceleration from the +6.7% posted within the prior-year interval — with transactions up 6.2% however common ticket really declining 2.2%. That sample at Sam’s issues as a result of it’s the closest direct analogue to Costco’s enterprise mannequin: membership-based warehouse retail, heavy grocery combine, related pack sizes, and overlapping geographic footprint.

The ticket compression at Sam’s probably displays combine shift towards consumables and away from higher-margin basic merchandise, a dynamic that bears watching when Costco discusses its personal basket composition Thursday night. In the meantime, House Depot and Lowe’s each posted comparable gross sales of simply +0.6%, underscoring as soon as once more that the patron is plainly prioritizing necessities over discretionary big-ticket initiatives — a setup that ought to proceed to favor Costco’s grocery-and-staples-weighted assortment.

Costco Buyers Eyeing Membership Renewals

The buyer-trends narrative round Costco has been remarkably constant for the higher a part of two years, and the upcoming print is unlikely to disrupt it. Inflation-weary customers proceed emigrate towards bulk-format worth, and Costco has captured a disproportionate share of that site visitors. Digitally-enabled comparable gross sales — the metric that has maybe stunned the bulls most over the previous 12 months — ran at +18.8% in April and +23.3% in March, suggesting that Costco’s long-standing digital weak point is meaningfully behind it.

The corporate is now mixing warehouse-fulfilled e-commerce, the Costco Logistics big-and-bulky supply community, and an increasing market presence in a manner that’s lastly transferring the needle. On the membership aspect, traders will probably be paying shut consideration to the worldwide renewal charge, which has traditionally hovered above 90% and serves as the only finest proxy for the sturdiness of the whole enterprise mannequin. Any slip towards the high-80s would dent the bull case meaningfully; a steady learn within the low-90s successfully validates the present premium a number of.

That premium a number of is, in fact, the elephant within the room. Costco COST shares have climbed roughly 16% year-to-date and commerce at a ahead P/E within the neighborhood of 50x, effectively above the broader retail group and richer than some other large-cap mass merchandiser.

The danger for shareholders heading into Thursday is subsequently a “good-but-not-great” end result — the kind of clear beat that has traditionally been met with a muted or unfavourable tape response as a result of expectations have been already so elevated. We noticed an identical dynamic play out at Walmart final Thursday, when a beat on each income and EPS nonetheless produced a notable decline.

Backside Line

There are additionally two wildcards that would materially transfer shares in both route. The primary is a possible particular dividend; Costco has traditionally paid one each three to 5 years, with the final sizeable distribution recorded in late 2023, placing the corporate squarely inside the window the place one other is perhaps introduced. The second is any commentary or quantification of potential tariff-related refunds, which some analysts imagine may finally translate into a large non-recurring revenue increase.

Neither is factored into consensus estimates, and both disclosure may create the form of clear upside catalyst that will justify a optimistic post-print response even at present valuations. Conversely, any softening in renewal charges, or commentary suggesting that tariff value pressures will strain the gross margin line within the second half, would probably be punished sharply.

General, Costco enters Thursday’s report able that few retailers can declare: month-to-month gross sales knowledge already pointing to a clear operational quarter, a buyer base that continues to lean in regardless of a wobbly broader client backdrop, and best-in-class execution in opposition to a peer set that has largely been treading water. The query is whether or not the print can clear the very excessive bar that the inventory’s year-to-date run has set.

Past Nvidia: AI’s Second Wave Is Right here

The AI revolution has already minted millionaires. However the shares everybody is aware of about aren’t prone to maintain delivering the most important earnings. AI’s second wave is transferring from infrastructure to implementation and these firms are on the forefront of this transition, positioned to turn out to be what Amazon and Google have been to the web period.

Costco Wholesale Company (COST) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.