The declining Fed rates of interest and a good public spending surroundings are boding effectively for the infrastructure firms of the US, together with names like Consolation Programs USA FIX and Quanta Providers, Inc. PWR. The booming tendencies towards AI-related services and products are primarily driving the expansion prospects of such companies within the economic system.

On Dec. 10, 2025, the Federal Reserve slashed its rates of interest by one other 0.25 share factors, setting the benchmark between 3.5% and three.75%. The discount within the borrowing price catalyzes the continuing favorable market tendencies, boosting extra challenge initiations, resulting in a promising future.

Consolation Programs affords set up and contracting companies throughout the HVAC market and is at the moment targeted on in search of alternatives for large-scale initiatives and investing further capital in inorganic progress initiatives. Conversely, Quanta’s enterprise surrounds large-scale electrical and utility infrastructure initiatives, with its focus primarily focused on margin enchancment efforts and the self-perform mannequin.

Let’s dive deep and intently examine the basics of the 2 shares to find out which one is a greater funding now.

The Case for Consolation Programs Inventory

Consolation Programs is realizing advantages from the sturdy demand tendencies throughout the Know-how sector, primarily due to robust information heart and chip manufacturing-related actions. Thus far in 2025, the Know-how sector contributed 42% of the entire revenues, reflecting progress from 32% a 12 months in the past, due to hyperscalers and associated infrastructure builders persevering with to take a position aggressively, regardless of ongoing macro headwinds. As of Sept. 30, 2025, the corporate had a file backlog of $9.38 billion, with a same-store backlog of $9.2 billion, indicating year-over-year will increase of 65.1% and 62%, respectively.

FIX is benefiting from clients committing earlier and reserving initiatives additional out, with significant parts of the backlog now extending into 2026 and 2027. Past information facilities, industrial and institutional markets stay supportive. Industrial clients symbolize roughly two-thirds of revenues, whereas institutional verticals comparable to healthcare, training and authorities proceed to indicate regular exercise, together with new hospital builds and expansions.

The corporate additionally ensures its shareholders are glad by means of share repurchases and dividend funds. Throughout the first 9 months of 2025, it repurchased 0.3 million shares for roughly $125.4 million beneath the buyback program. Additionally, on Oct. 23, 2025, Consolation Programs’ board of administrators hiked the quarterly dividend fee by 20% to 60 cents per share ($2.40 per share yearly).

Nevertheless, FIX’s rising publicity to hyperscale information facilities is a double-edged sword. Any slowdown in AI-driven capital expenditures, challenge deferrals by cloud suppliers, or energy availability constraints may compress backlog progress and utilization. In addition to, challenge delays, scope adjustments, buyer funding points or cancellations, notably in giant and sophisticated initiatives, may end in backlog conversion failure. Consolation Programs can be involved about shortages of expert labor and rising wage strain within the present market dynamics. In addition to, publicity to aggressive pricing, challenge combine shifts and normalization from peak situations may disturb its present margin ranges and cut back profitability.

The Case for Quanta Inventory

Being a specialty contracting companies supplier, Quanta is capitalizing on the booming tendencies surrounding electrical transmission, grid modernization and energy era tied to AI, information facilities, electrification and reshoring. The administration indicated that accelerating demand within the Electrical section and broad exercise throughout key finish markets are reinforcing these tendencies and strengthening general challenge momentum. As of the third quarter of 2025, PWR’s backlog reached a file $39.2 billion, up from $33.96 billion a 12 months in the past, underscoring sturdy demand visibility.

Furthermore, disciplined bidding, efficient danger administration and a good challenge combine are primarily driving PWR’s margin growth and consistency. Not like many friends, Quanta self-performs 80–85% of its work. This strategy offers higher management over prices, schedules and high quality, mitigating dangers related to subcontracting. Within the first 9 months of 2025, working margin elevated to five.5% from 5.2% on a year-over-year foundation. Throughout the identical time-frame, gross margin expanded 50 foundation factors 12 months over 12 months to 14.8%.

Quanta persistently focuses on decreasing leverage whereas sustaining capability for selective acquisitions, natural funding and shareholder returns. Throughout the first 9 months of 2025, PWR repurchased 538,559 shares for $134.6 million, with $365.1 million remaining beneath its buyback program. The steadiness between reinvestment and shareholder returns demonstrates disciplined capital administration, enhancing long-term worth creation. For 2025, the corporate expects free money move of $1.3-$1.7 billion. It had reported $1.55 billion in 2024.

Though demand visibility is robust, execution danger stays elevated as a result of rising measurement and complexity of infrastructure initiatives. Giant transmission, era and information center-related applications typically face allowing delays, interconnection bottlenecks and regulatory approvals that may push Quanta’s income recognition to the south. Moreover, whereas renewable and battery initiatives stay energetic, the tempo of progress is moderating in contrast with prior years, creating variability in quarterly combine.

Inventory Efficiency & Valuation

As witnessed from the chart beneath, up to now six months, Consolation Programs’ share value efficiency stands considerably above Quanta and the broader Building sector.

Picture Supply: Zacks Funding Analysis

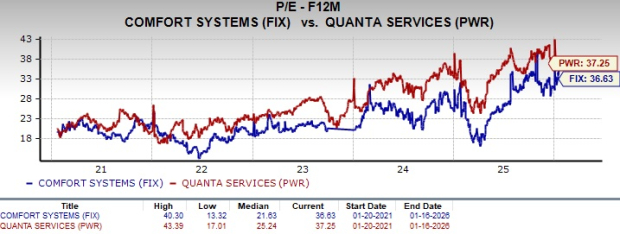

Contemplating valuation, during the last 5 years, Consolation Programs has been buying and selling beneath Quanta on a ahead 12-month price-to-earnings (P/E) ratio foundation.

Picture Supply: Zacks Funding Analysis

Total, from these technical indicators, it may be deduced that FIX inventory affords an incremental progress pattern with a reduced valuation, whereas PWR inventory affords a diminishing progress pattern with a premium valuation.

Evaluating EPS Estimate Developments: FIX vs. PWR

The Zacks Consensus Estimate for FIX’s 2025 EPS signifies 80.2% year-over-year progress, with the 2026 estimate indicating a rise of 16.4%. The 2025 and 2026 EPS estimates have remained secure over the previous 60 days.

FIX’s EPS Development

Picture Supply: Zacks Funding Analysis

The Zacks Consensus Estimate for PWR’s 2025 earnings implies a year-over-year enchancment of 18.1%, whereas the identical for 2026 signifies progress of 17.2%. The EPS estimates for 2025 and 2026 have trended upward up to now 60 and 30 days, respectively.

PWR’s EPS Development

Picture Supply: Zacks Funding Analysis

Return on Fairness (ROE) of FIX & PWR Shares

Consolation Programs’ trailing 12-month ROE of 43.6% considerably exceeds Quanta’s common, underscoring its effectivity in producing shareholder returns.

Picture Supply: Zacks Funding Analysis

Is It FIX Inventory or PWR Inventory?

Easing rates of interest, robust public infrastructure spending and AI-driven funding are making a supportive backdrop for U.S. infrastructure contractors. Consolation Programs is benefiting from outsized publicity to information facilities, semiconductor services and different technology-driven initiatives. A file backlog extending into 2026-2027, robust pricing self-discipline and superior return on fairness spotlight FIX’s execution power. Nevertheless, FIX’s heavy reliance on hyperscale information heart spending introduces cyclicality danger if AI-related capital expenditures gradual or giant initiatives face delays.

However, Quanta affords broader publicity to regulated utility and energy infrastructure spending, offering extra secure multi-year visibility. Its file backlog, self-perform mannequin and disciplined bidding have pushed regular margin enchancment and powerful free money move era. That mentioned, large-scale transmission and era initiatives carry execution and allowing dangers, whereas moderating progress in renewables may add volatility. PWR additionally trades at a relative valuation premium.

As each shares at the moment carry a Zacks Rank #3 (Maintain), given FIX inventory’s near-term progress and superior profitability, it’s a comparatively higher funding choice now than PWR inventory. You may see the entire listing of at the moment’s Zacks #1 (Robust Purchase) Rank shares right here.

#1 Semiconductor Inventory to Purchase (Not NVDA)

The unbelievable demand for information is fueling the market’s subsequent digital gold rush. As information facilities proceed to be constructed and always upgraded, the businesses that present the {hardware} for these behemoths will turn into the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to benefit from the following progress stage of this market. It makes a speciality of semiconductor merchandise that titans like NVIDIA do not construct. It is simply starting to enter the highlight, which is precisely the place you need to be.

See This Inventory Now for Free >>

Quanta Providers, Inc. (PWR) : Free Inventory Evaluation Report

Consolation Programs USA, Inc. (FIX) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.