Getty Photographs

Market Overview

At occasions, the inventory market’s climb brings to thoughts the trek to Everest Base Camp: although the vacation spot is increased than the start line, the trail shouldn’t be a easy regular climb. In Nepal, trekkers acquire elevation, descend into valleys, after which climb once more. They repeat this sample many occasions, which is why the full vertical climb is nearly double the distinction in elevation between the trailhead and Base Camp.

Markets work in an analogous approach, with a journey increased that always consists of pullbacks, rallies and pauses alongside the way in which. Simply as a trekker should settle for the switchbacks, descents and acclimatization stops required to achieve Base Camp, buyers too should acknowledge that volatility shouldn’t be an interruption of the journey however a part of the trail ahead.

Encouragingly, the market seems to have already begun an acclimatization interval, with the S&P 500 Index holding roughly flat over the previous six weeks. Even so, the index delivered a 14.9% worth return for the quarter, its twelfth strongest quarterly acquire since 1950. The market has sometimes superior additional following previous equally sharp rallies, averaging positive factors of 5.5% over the subsequent three months and 10.4% over the subsequent six. Though markets usually pause to digest and even right after massive positive factors, historical past suggests these episodes often show fleeting, that means that main indexes might transfer increased within the second half of 2026, bolstered by the easing of a number of financial overhangs in current weeks (Exhibit 1).

Exhibit 1: Energy Begets Energy: Prime 15 S&P 500 Quarters Since 1950

Information as of June 30, 2026. Sources: FactSet, S&P.

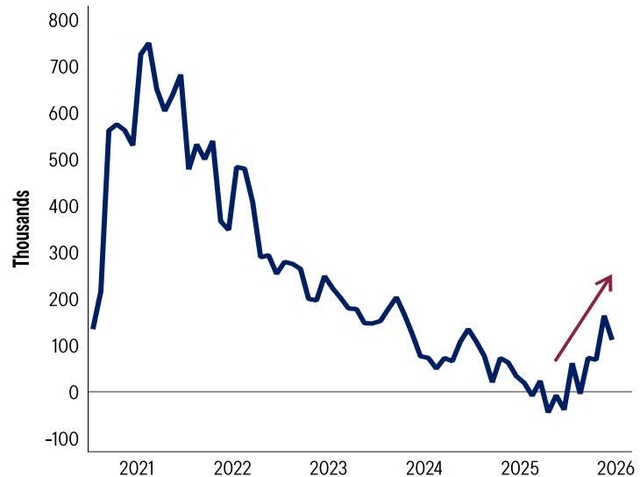

The primary overhang that has eased is the labor market, which seems to have turned a nook (Exhibit 2). Final 12 months’s labor market was gentle, creating a complete of simply 116k jobs. Against this, the financial system averaged 111k per thirty days within the second quarter of 2026, an acceleration from the primary quarter’s 73k month-to-month common. The job market seems to have stabilized, going from zero to hero in 2026, and giving the financial growth firmer footing because it heads onward into the second half of the 12 months.

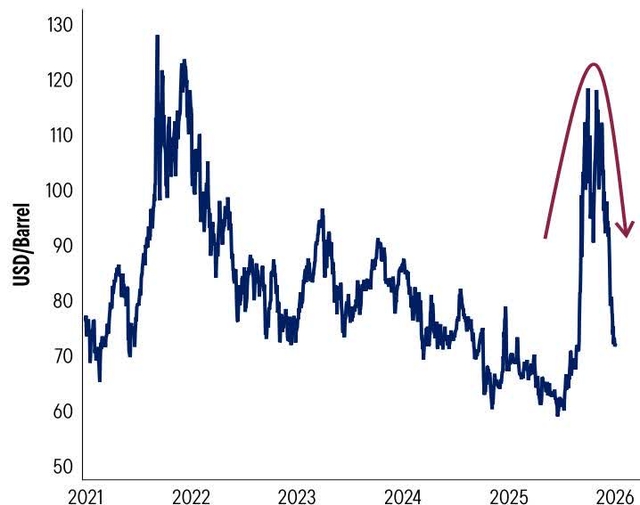

A second space of current enchancment within the financial backdrop comes from falling oil costs. Excessive vitality prices had posed a menace to the well being of the U.S. financial system, though it was one we believed was manageable given the financial system’s well being earlier than the battle between the U.S. and Iran broke out. The current Memorandum of Understanding has helped push crude costs again to pre-conflict ranges, whereas costs on the pump have slipped under $4/gallon on a nationwide common foundation and will proceed to float decrease within the coming weeks.

Exhibit 2: Labor Market: Zero to Hero: Month-to-month Change in Nonfarm Payrolls (3 Month Shifting Common)

Sources: U.S. Bureau of Labor Statistics (BLS), Macrobond. Information as of June 5, 2026, newest accessible as of June 30, 2026.

This decline comes at an vital time because the enhance from bigger One Huge Lovely Invoice tax refunds fades, with much less of a headwind from increased fuel costs being a constructive for the consumption outlook (Exhibit 3). On the similar time, tentative indicators from financial institution credit score/debit card information recommend resilience within the decrease half of the “Okay” client. Job positive factors have broadened into areas similar to building, manufacturing {and professional}/enterprise providers, which ought to assist to raise this cohort. In the end, we imagine combination actual incomes ought to see enchancment because of the mixture of a stronger labor market and fewer of an oil drag, which ought to help consumption within the again half of the 12 months.

Exhibit 3: Aid on the Pump: Brent Crude Oil

Sources: Intercontinental Trade (ICE), Macrobond. Information as of July 3, 2026.

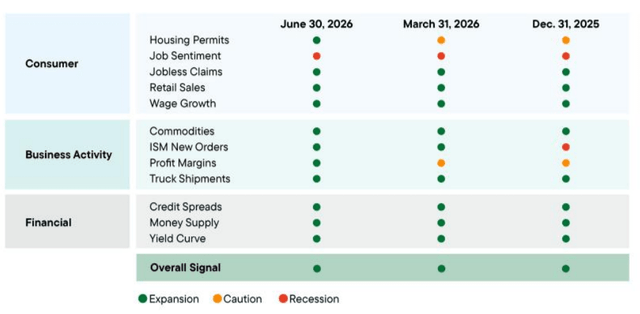

With a number of financial clouds receding, we imagine the U.S. financial system ought to stay resilient, a view per the robust total inexperienced sign from the ClearBridge Recession Dashboard (Exhibit 4). For buyers, the dashboard serves very similar to a climate report on the mountain: not a assure of clear skies, however a helpful information concerning the situations forward. At current, the dashboard is sort of all inexperienced, with 11 of 12 indicators at present in growth territory and no adjustments final month.

Exhibit 4: ClearBridge Recession Dashboard

Information as of June 30, 2026. Sources: BLS, Federal Reserve, Census Bureau, ISM, BEA, American Chemistry Council, American Trucking Affiliation, Convention Board, Bloomberg, CME Group, FactSet and Macrobond. The ClearBridge Recession Dashboard was created in January 2016. References to the alerts it will have despatched within the years previous to January 2016 are primarily based on how the underlying information was mirrored within the element indicators on the time.

Decrease oil costs might do extra than simply take away an financial overhang; they’ll additionally set the stage for decrease rates of interest. Traditionally, headline inflation strain usually eases following the height in oil costs, bringing inflation expectations decrease. Buyers start to anticipate a much less aggressive financial coverage path, which brings down intermediate and long-term rates of interest. Since 1990, 10-year Treasury yields have fallen by a mean of 28 bps, 67 bps and 81 bps, respectively, over the three, six and 12 months following main Brent crude peaks (Exhibit 5).

Though 10-year yields stay modestly elevated as we speak because the Fed works to convey inflation to the two% inflation goal, which has now been overshoot for greater than 5 years, the drop in oil costs might assist inflation reasonable quicker than anticipated. If inflation does reasonable and a re-pricing happens throughout the yield curve, decrease yields might present help for fairness valuations and returns.

Exhibit 5: Peak Oil, Decrease Yields: Change in 10-Yr US Treasury Yield Following Historic Peaks in Brent Crude Oil

Information as of June 30, 2026. Sources: ICE, Federal Reserve, Bloomberg.

Fairness valuations are intently tied to rates of interest, however that relationship has shifted traditionally alongside differing macroeconomic regimes. Within the Nineteen Eighties and Nineteen Nineties, inflation remained the first concern following the runaway worth spirals of the Nineteen Seventies, which led to a unfavourable relationship between the S&P 500 and 10-year Treasury yields. In that period, increased inflation went hand-in-hand with a extra hawkish Fed, increased charges and strain on company earnings.

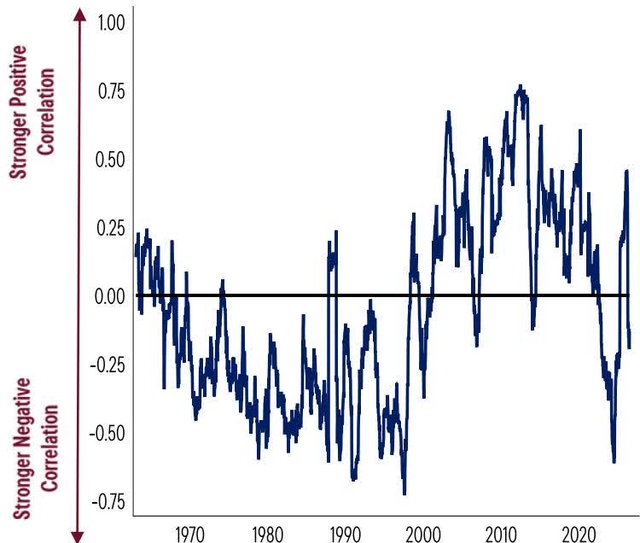

Nevertheless, a brand new regime took maintain within the new millennium, as deflationary fears overtook inflationary ones, and the connection between shares and bonds shifted to at least one demonstrating constructive correlation. Since 2022, nonetheless, inflation has as soon as once more develop into the first scourge for U.S. buyers, and stock-bond correlations have turned unfavourable as soon as once more (Exhibit 6).

Exhibit 6: Destructive Correlation is Again: Rolling 1-Yr Weekly S&P 500 and US 10-Yr Treasury Yield Correlation

Sources: U.S. Division of Treasury, S&P World, Macrobond. Information as of July 2, 2026.

How lengthy this unfavourable correlation relationship persists is more likely to depend upon the long run path of inflation. Like shifting climate patterns within the Himalayas, macro regimes can persist for prolonged intervals (measured in a long time) and require buyers to regulate their route accordingly. The present unfavourable stock-bond correlation regime might endure given the secular nature of those shifts up to now. Traditionally, rising market and infrastructure equities have carried out finest in periods of unfavourable stock-bond correlation, delivering common returns of 24% and 20%, respectively (Exhibit 7).

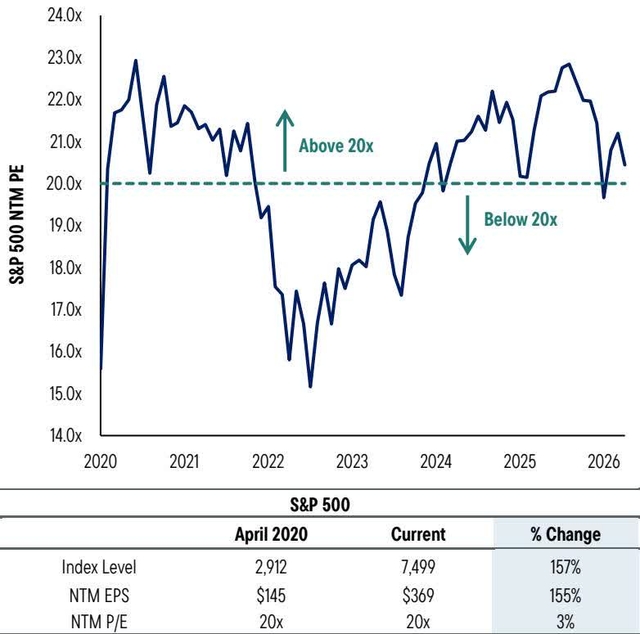

Whereas the trail ahead for stock-bond correlations could also be up for debate, one factor that is not is that fairness market valuations are elevated, with the S&P 500 buying and selling above 20x ahead (anticipated next-12-month) earnings. Increased valuations are the market equal of climbing at altitude: progress remains to be doable, however there may be much less room for missteps. Nevertheless, wealthy multiples have develop into the “new regular” for the reason that pandemic, with the index buying and selling above 20x 64% of the time since first crossing that degree in April 2020.

Importantly, elevated P/Es haven’t derailed returns, with the S&P 500 rising 157% over these 74 months, or 16.6% annualized — roughly twice the long-term common. Robust earnings have been the oxygen tank powering the market’s climb within the face of lofty valuations, with next-12-month earnings expectations up 155% cumulatively over the identical interval (Exhibit 8). Merely put, the S&P 500 seems to be in a better valuation regime, with earnings doing the entire heavy lifting behind the market’s climb increased — a dynamic we anticipate to proceed within the second half.

Exhibit 7: Destructive Correlation, What Now: Fairness Asset Class Returns Throughout Historic Destructive Inventory-Bond Correlation Durations

Observe: Durations of unfavourable stock-bond correlation primarily based on S&P 500 and 10-Yr US Treasury Yield. Sources: Macrobond, Federal Reserve, FactSet, S&P, FTSE Russell, and MSCI.

Exhibit 8: Increased Valuation Regime: S&P 500

Information as of June 30, 2026. Sources: FactSet, S&P.

Over the course of the summer season, we anticipate investor consideration to shift towards this fall’s midterm elections, which traditionally have been a supply of volatility. Midterm years will be difficult for fairness markets as a result of they introduce political uncertainty: which celebration has management of

Congress (and by what margin) has implications for taxes, regulation, authorities spending and sector-specific insurance policies.

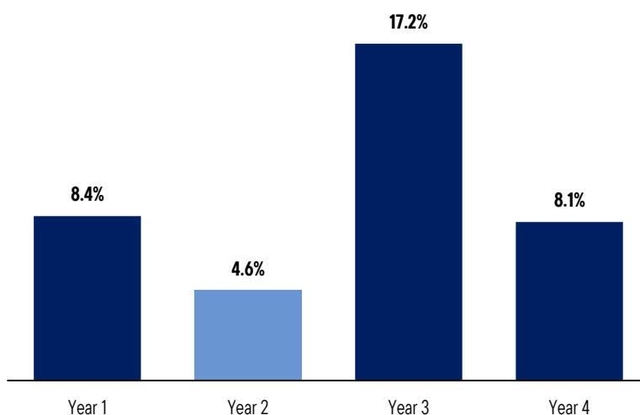

Traditionally, the incumbent president’s celebration loses seats within the midterm, rising the chance of gridlock or slowing the president’s coverage agenda. This uncertainty has weighed on market returns up to now, with midterm election years delivering the weakest common efficiency of the four-year presidential cycle at simply 4.6% (Exhibit 9). However political uncertainty, like mountain climate, is simply a part of the story in figuring out how navigable the trail ahead could also be.

Exhibit 9: The Midterm Yr Lull: Common S&P 500 Return by Presidential Cycle Yr, 1950 – Current

Information as of June 30, 2026. Sources: FactSet, S&P.

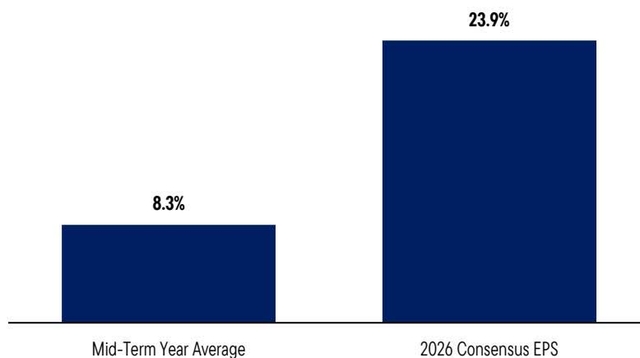

Though equities have traditionally posted decrease annualized returns within the second 12 months of presidential cycles, the business-cycle backdrop finally issues greater than the coverage calendar. At this time’s earnings outlook is way stronger than the everyday midterm 12 months precedent; sell-side consensus expects 2026 EPS progress of 23.9%, which is sort of 3 times the historic midterm 12 months common of 8.3% (Exhibit 10). In our view, that earnings energy is a robust tailwind that would assist show 2026 to be the exception to the rule.

Exhibit 10: EPS >Mid-term Seasonality? Historic Mid-Time period Yr S&P 500 EPS Development since 1950 vs. At this time

Information as of June 30, 2026. Sources: S&P, FactSet, Shiller.

With the financial system on stable footing and several other headwinds fading, the market’s current interval of digestion seems to be much less like a warning signal and extra like a traditional a part of the climb increased. After a traditionally robust second quarter, a interval of consolidation shouldn’t be atypical; it’s the market’s model of catching its breath earlier than embarking on the subsequent ascent. Most significantly, the bettering basic backdrop ought to enhance company earnings, which we imagine will proceed to be the first driver of the fairness market’s advance. The potential for decrease Treasury yields is a doable tailwind, significantly with the market buying and selling at lofty valuations, however not a requirement for additional upside in our view. With the financial system bolstered by the strengthening labor market, earnings sturdy and inflationary pressures easing as a consequence of decrease oil, we imagine the market is positioned to maintain climbing within the second half of 2026.