Simon Property Group’s SPG) inventory has surged again close to its 52-week highs after delivering robust Q1 outcomes on Monday night that strengthened its place because the premier mall REIT within the U.S.

The inventory has rallied above $200, supported by resilient client spending, excessive occupancy ranges, and bettering working metrics.

The important thing query for a lot of traders is whether or not SPG nonetheless affords upside at these elevated ranges or if the inventory is price holding onto due to its juicy dividend.

Picture Supply: Zacks Funding Analysis

SPG’s Q1 Outcomes Present Continued Energy

SPG posted stronger-than-expected Q1 2026 outcomes, with earnings and income each comfortably forward of Wall Road expectations. The corporate reported adjusted EPS of $3.17, which was up 7% from $2.95 per share a 12 months in the past and beat expectations of $2.98.

This got here on Q1 gross sales of $1.75 billion, a 19% improve from the prior 12 months quarter, whereas impressively exceeding estimates of $1.56 billion.

Moreover, SPG’s robust Q1 outcomes highlighted a number of encouraging tendencies: robust leasing demand throughout premium retail properties, wholesome occupancy charges and tenant gross sales, continued pricing energy on rents, and strong money circulation era regardless of financial uncertainty.

Most significantly, administration maintained a assured tone in regards to the retail setting and the long-term power of high-quality malls as SPG’s portfolio continues to outperform lower-tier retail facilities as a result of luxurious manufacturers and experiential tenants nonetheless need entry to its premium areas.

Picture Supply: Zacks Funding Analysis

SPG’s Valuation is Nonetheless Cheap

Regardless of an intensive rally in recent times, particularly for a REIT inventory, SPG doesn’t seem excessively costly relative to its earnings energy and asset high quality.

Primarily based on present valuation metrics, SPG trades at an inexpensive 15X ahead earnings a number of in comparison with its Zacks REIT and Fairness Belief-Retail Business’s common of 17X and the benchmark S&P 500’s 23X.

Picture Supply: Zacks Funding Analysis

Moreover, Simon Property Group owns a few of the highest-quality retail actual property on this planet. Its portfolio contains Class A malls, outlet facilities, and mixed-use locations that appeal to foot visitors at the same time as weaker malls battle.

This offers SPG stronger pricing energy and extra resilient occupancy than many retail REIT friends. In contrast to many cyclical retail names, SPG generates extremely steady rental earnings. Plus, long-term leases and diversified tenants assist clean earnings by means of financial cycles.

What could also be most interesting is that even after the inventory’s robust run, SPG nonetheless affords an above-market dividend yield (4.36%), which stays engaging for income-focused traders. The mix of yield plus reasonable progress makes SPG interesting in a higher-rate setting.

Picture Supply: Zacks Funding Analysis

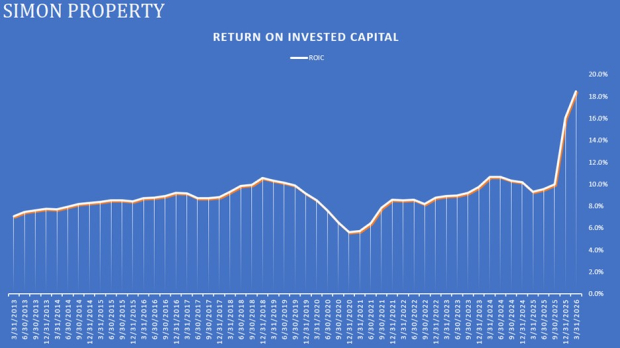

SPG’s ROIC Suggests Sturdy Capital Allocation

One of many extra compelling elements of Simon Property Group is its constantly strong return on invested capital (ROIC).

Latest knowledge reveals SPG producing ROIC of round 18.5% when excluding dividends, which could be very robust for a REIT and above many friends in business actual property.

A REIT or any firm for that matter with an ROIC close to 20% or greater is necessary as a result of it signifies SPG is deploying capital effectively, with it noteworthy that administration has traditionally made disciplined acquisitions and redevelopment investments whereas incomes robust returns on its premium properties.

Notably, SPG’s ROIC has remained comparatively steady over lengthy intervals, even throughout troublesome retail cycles. That consistency suggests the enterprise has sturdy aggressive benefits.

For REIT traders, ROIC is very precious as a result of it helps distinguish high-quality property house owners from corporations merely counting on leverage and asset appreciation.

Picture Supply: Zacks Funding Analysis

Dangers Buyers Ought to Watch

Even high-quality REITs face challenges, and beneath are the potential challenges that traders ought to look ahead to:

Curiosity Charges

Increased rates of interest can strain REIT valuations as a result of financing prices rise and income-oriented traders acquire alternate options in bonds.

Client Spending Slowdown

If the economic system weakens materially, discretionary retail spending might soften, hurting tenant gross sales and leasing exercise.

E-Commerce Competitors

Whereas Simon’s premium malls have confirmed resilient, the long-term shift towards on-line buying stays a structural headwind for retail actual property.

Nonetheless, Simon has tailored higher than most rivals by emphasizing luxurious retail, eating, leisure, and mixed-use redevelopment.

Is SPG a Purchase Close to 52-Week Highs?

For long-term traders, Simon Property Group nonetheless appears engaging regardless of buying and selling close to file ranges. On this regard, SPG has robust working momentum, high-quality belongings, dependable dividends, strong ROIC, and affordable valuation metrics.

Buyers looking for a mix of earnings, stability, and reasonable long-term appreciation should still discover Simon Property Group’s inventory interesting. For now, SPG sports activities a Zacks Rank #2 (Purchase).

Radical New Know-how Might Hand Buyers Enormous Beneficial properties

Quantum Computing is the following technological revolution, and it could possibly be much more superior than AI.

Whereas some believed the know-how was years away, it’s already current and shifting quick. Giant hyperscalers, similar to Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to combine quantum computing into their infrastructure.

Senior Inventory Strategist Kevin Prepare dinner reveals 7 rigorously chosen shares poised to dominate the quantum computing panorama in his report, Past AI: The Quantum Leap in Computing Energy.

Kevin was among the many early specialists who acknowledged NVIDIA’s monumental potential again in 2016. Now, he has keyed in on what could possibly be “the following large factor” in quantum computing supremacy. At this time, you may have a uncommon likelihood to place your portfolio on the forefront of this chance.

See Prime Quantum Shares Now >>

Simon Property Group, Inc. (SPG) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.