")

Nonetheless flying considerably beneath the radar, Micron Know-how MU has change into a frontrunner within the AI infrastructure increase as a result of sturdy demand for its high-bandwidth reminiscence (HBM) options.

With HBM being important to powering generative AI fashions, Micron’s inventory has began to rebound towards its 52-week highs of $129 a share, with some analysts’ value targets calling for brand new all-time peaks.

Contemplating such, and in correlation with a development of very optimistic earnings estimate revisions, Micron inventory sports activities a Zacks Rank #1 (Robust Purchase) and lands the Bull of the Day.

Micron’s AI Infrastructure Benefit

Attributing to its AI infrastructure dominance, Micron is a key provider for Nvidia’s NVDA Blackwell GB200 and AMD’s AMD Intuition MI350 GPUs, which require large reminiscence bandwidth.

Extra intriguing, and resulting in Micron’s AI Infrastructure benefit, is its pricing energy as HBM merchandise are complicated to fabricate and wafer-intensive, making provide tight. Notably, Micron has offered out its HBM output for 2025 and is seeing sturdy demand into 2026, with the shortage boosting its margins.

Micron’s Stellar Development

Primarily based on Zacks’ estimates, Micron’s complete gross sales are actually anticipated to spike 47% in fiscal 2025 to $36.91 billion in comparison with $25.11 billion final yr. Plus, FY26 gross sales are projected to climb one other 34% to $49.43 billion.

Picture Supply: Zacks Funding Analysis

Much more charming is Micron’s elevated profitability, with annual earnings presently slated to skyrocket over 500% this yr to $8.04 per share versus EPS of $1.30 in 2024. Higher nonetheless, FY26 EPS is forecasted to pop one other 62% to $13.05.

Resulting in bullish sentiment for Micron inventory is that FY25 and FY26 EPS estimates have soared 16% and 23% over the past 60 days, respectively, as proven under.

Picture Supply: Zacks Funding Analysis

Micron’s Enticing Valuation & Analyst Upgrades

Contemplating the excessive premiums AI-infrastructure associated shares are commanding, MU shares nonetheless commerce at a really affordable 14.5X ahead earnings a number of and at 3.5X ahead gross sales, that are each vital reductions to the S&P 500’s averages.

Picture Supply: Zacks Funding Analysis

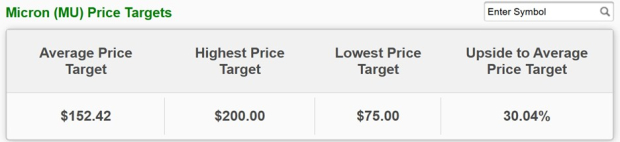

The fruits of Micron’s execution, together with its affordable valuation, has led to analysts elevating their value targets for MU. It’s noteworthy that JPMorgan JPM raised its value goal for MU from $165 to $185, citing stronger DRAM (Dynamic Random-Entry Reminiscence) pricing.

In the meantime, different corporations like Mizuho and Needham have remained bullish on Micron’s HBM upside. For the time being, the Common Zacks Value Goal of $152.42 suggests 30% upside in Micron inventory, which is roughly on par with its all-time excessive.

Picture Supply: Zacks Funding Analysis

Backside Line

Dominating the AI reminiscence house, now seems to be a great time to spend money on Micron Know-how inventory, with MU shaping as much as be a viable funding for 2025 and past.

One Massive Acquire, Each Buying and selling Day

That will help you take full benefit of this market, you’re invited to entry each inventory advice in all our personal portfolios – for simply $1.

Zacks personal portfolio companies that closed 256 double and triple-digit winners in 2024 alone. That’s about one massive acquire every single day the market was open. In fact, not all our picks are winners, however members have seen latest features as excessive as +627% +1,340%, and +1,708%.

Think about how a lot you could possibly revenue with a gradual stream of real-time picks from all our companies that cowl a lot of methods to swimsuit quite a lot of investing and buying and selling kinds.

Micron Know-how, Inc. (MU) : Free Inventory Evaluation Report

JPMorgan Chase & Co. (JPM) : Free Inventory Evaluation Report

Superior Micro Units, Inc. (AMD) : Free Inventory Evaluation Report

NVIDIA Company (NVDA) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.