Amazon AMZN missed EPS estimates in its December-quarter report, however the enterprise is in any other case actually firing on all cylinders.

The market’s adverse response to the Amazon report wasn’t because of the EPS miss, however moderately to administration’s eye-popping capital spending funds for 2026, which coincided with renewed worries concerning the broader AI house and rising fears that this new know-how might critically erode the earnings energy of legacy know-how companies like software program.

The market’s response to Amazon is broadly in the identical class as Alphabet’s GOOGL after its quarterly launch, with the severity of Amazon’s ‘punishment’ reflecting traders’ shock at studying of administration’s AI plans. Amazon plans to spend $200 billion in capital expenditures in 2026, up from $132 billion in 2025 and $83 billion in 2024. Amazon’s working money flows modestly exceeded its $132 billion capex outlays in 2025, however the firm’s 2026 capex funds will probably exceed its working money flows.

Earlier than we learnt of those lofty spending plans, many out there anticipated 2026 to be the capex peak for Amazon (Alphabet and others). However administration’s commentary concerning the mission-critical nature of those outlays possible signifies that it could be untimely to declare peak capex. Amazon shares at the moment are down -8.8% over the previous 12 months, lagging the broader market’s +15.8% achieve and Alphabet’s spectacular +74.1% rise.

Amazon is doing nice in its core companies, with its cloud unit having fun with accelerating progress and popping out with the very best progress in three years. Revenues in Amazon Internet Providers (AWS) elevated +24% in 2025 This autumn, which compares to year-over-year progress charges of +20% in Q3, +19% in Q2, and +17% in Q1. Backlog for the enterprise elevated +40% from the identical interval final 12 months to $244 billion, with administration describing a strong demand setting.

Whereas Amazon stays the cloud chief, the Alphabet report confirmed accelerating momentum on the search big’s Google Cloud enterprise. Revenues for Google Cloud elevated +48% from the identical interval final 12 months in 2025 This autumn, which compares to progress charges of +35%, +32%, and +28% in Q3, Q2, and Q1, respectively. The sturdy cloud positive aspects at Amazon and Alphabet put the highlight on Microsoft’s lack of momentum on this key enterprise space.

At this stage within the This autumn reporting cycle, Nvidia NVDA is the one Magazine 7 member that has but to report December-quarter outcomes. Nvidia is scheduled to report This autumn outcomes on February 25th, with EPS and revenues for the interval anticipated to be up +70.8% and +66.7% from the identical interval final 12 months, respectively.

Combining the precise outcomes for the 6 Magnificent 7 members which have reported already with estimates for Nvidia, complete This autumn earnings for the group are anticipated to be up +24.2% from the identical interval final 12 months on +18.9% greater revenues, which might comply with the group’s +28.3% earnings progress on +18.1% income progress in 2025 Q3.

The chart beneath reveals the group’s blended This autumn earnings and income progress relative to what was achieved within the previous interval and what’s anticipated within the coming three intervals.

Picture Supply: Zacks Funding Analysis

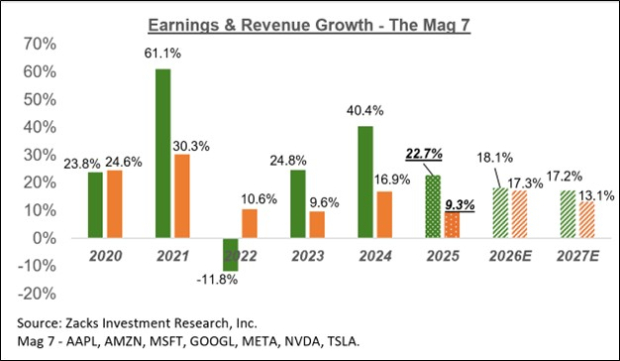

The chart beneath reveals the Magazine 7 group’s earnings and income progress image on an annual foundation.

Picture Supply: Zacks Funding Analysis

Please observe that the Magazine 7 group is on monitor to usher in 26.6% of all S&P 500 earnings in 2026 and account for 33.5% of the index’s market capitalization.

The Magazine 7 group has been having fun with a steadily enhancing earnings outlook, with analysts elevating their estimates. We noticed that development in play forward of the beginning of the Q3 earnings season, and one thing related is in place for the 2025 This autumn interval as nicely.

The chart beneath reveals how combination earnings estimates for the Magazine 7 group have advanced since July 2025.

Picture Supply: Zacks Funding Analysis

This autumn Earnings Season Scorecard

By means of Friday, February 6th, we have now seen This autumn outcomes from 293 S&P 500 members or 58.6% of the index’s complete membership. Whole earnings for these firms are up +14.1% from the identical interval final 12 months on +9.2% greater revenues, with 77.5% beating EPS estimates and 72% beating income estimates.

We now have greater than 500 firms on deck to report outcomes this week, together with 77 index members. The week’s lineup features a mix of Tech operators like Spotify, Lyft, and Cisco, and conventional bellwethers like DuPont, Ford, Coca-Cola, BP, and others.

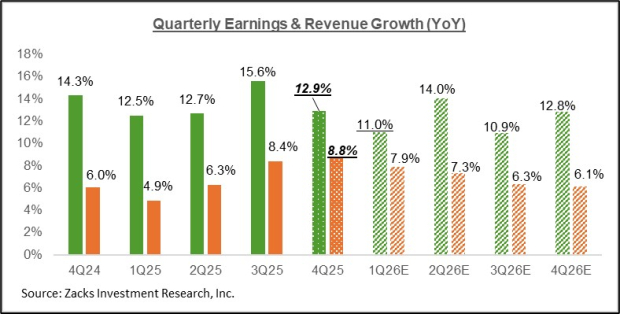

The comparability charts beneath put the expansion charges for these 293 index members with what we had seen from this identical group of firms in different current intervals.

Picture Supply: Zacks Funding Analysis

The comparability charts beneath put the This autumn EPS and income beats percentages for this group firms relative to what we had seen from them in different current intervals.

Picture Supply: Zacks Funding Analysis

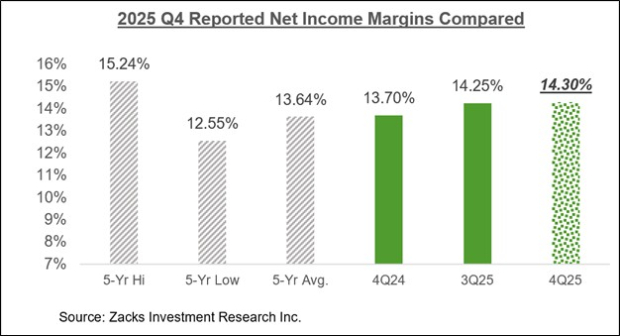

The comparability chart beneath places the This autumn internet margins for the 293 firms which have reported in a historic context.

Picture Supply: Zacks Funding Analysis

The Earnings Huge Image

The chart beneath reveals the This autumn earnings and income progress expectations within the context of the place progress has been within the previous 4 quarters and what’s anticipated within the coming 4 quarters.

Picture Supply: Zacks Funding Analysis

Estimates for the present interval (2026 Q1) have modestly moved up in current days, because the chart beneath reveals.

Picture Supply: Zacks Funding Analysis

2026 Q1 estimates have elevated modestly for five of the 16 Zacks sectors because the begin of January, together with Tech, Industrials, Retail, Utilities, and Enterprise Providers. On the adverse facet, Q1 estimates have come down for 10 of the 16 Zacks sectors, with the largest declines on the Power, Medical, and Client Discretionary sectors.

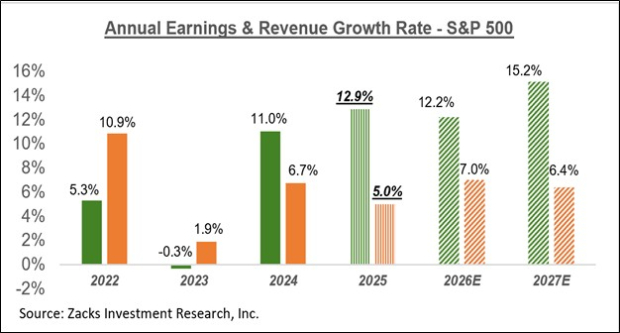

The chart beneath reveals the general earnings image on a calendar-year foundation, with double-digit earnings progress anticipated in 2025 and 2026.

Picture Supply: Zacks Funding Analysis

For an in depth have a look at the general earnings image, together with expectations for the approaching intervals, please take a look at our weekly Earnings Developments report >>>>Earnings Outlook Improves: A Nearer Look

5 Shares Set to Double

Every was handpicked by a Zacks knowledgeable because the #1 favourite inventory to achieve +100% or extra within the coming 12 months. Whereas not all picks might be winners, earlier suggestions have soared +112%, +171%, +209% and +232%.

A lot of the shares on this report are flying underneath Wall Road radar, which offers a fantastic alternative to get in on the bottom ground.

As we speak, See These 5 Potential Residence Runs >>

Amazon.com, Inc. (AMZN) : Free Inventory Evaluation Report

NVIDIA Company (NVDA) : Free Inventory Evaluation Report

Alphabet Inc. (GOOGL) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.