")

Pizza big, Papa John’s Worldwide, Inc. PZZA, has seen its earnings estimates steadily fall off a cliff over the past a number of years, pushed by declining comparable gross sales, value pressures, and heavy competitors from its rivals resembling Domino’s.

PZZA’s most up-to-date wave of downward earnings revisions earn it a Zacks Rank #5 (Robust Promote).

PZZA Inventory is Down 70%: It’s Not Time to Purchase the Dip But

Papa John’s boasts that it’s the third-largest pizza supply firm on the planet, with greater than 6,000 eating places in roughly 50 international locations and territories. The agency operates throughout 4 important segments: Home Firm-Owned Eating places, North America Franchised Eating places, North America Eating places, and Worldwide Eating places.

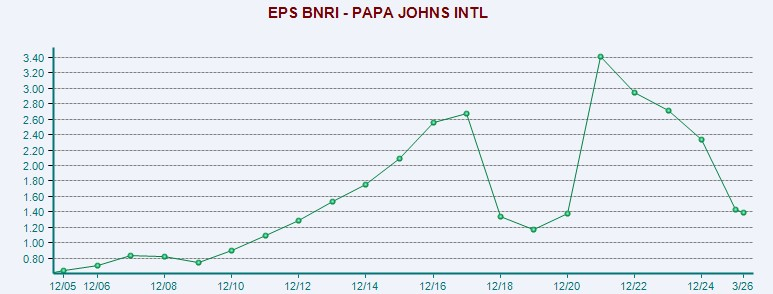

Picture Supply: Zacks Funding Analysis

PZZA income dropped 3.6% in FY24 and slipped barely in 2025. Its North America comparable gross sales fell 2% in FY25, with Home Firm-owned eating places down 3% and North America franchised eating places down 2%. Worst nonetheless, its GAAP earnings tanked 64% YoY and its adjusted EPS fell 39%.

Most not too long ago, its first-quarter 2026 income fell 7.7% YoY, with North America comparable gross sales down 6.4%. “In North America, outcomes have been in keeping with our expectations as we navigate the cautious client surroundings and promotional QSR market,” CEO and President Todd Penegor stated in ready remarks.

Picture Supply: Zacks Funding Analysis

Its adjusted EPS additionally slipped 11% YoY, falling 20% in need of our estimate. Papa John’s earnings outlook has dropped considerably over the past 90 days, and its most correct estimate for FY27 got here in 9% under the already beaten-down consensus.

This backdrop earns PZZA a Zacks Rank #5 (Robust Promote) and has extended its string of damaging EPS revisions over the past a number of years.

Picture Supply: Zacks Funding Analysis

Papa John’s faces intense competitors from Domino’s DPZ, Pizza Hut, and different chains, forcing discounting and promotions. The corporate can also be struggling, alongside many others, with slower client spending as customers across the U.S. pull again on non-essentials as inflation continues.

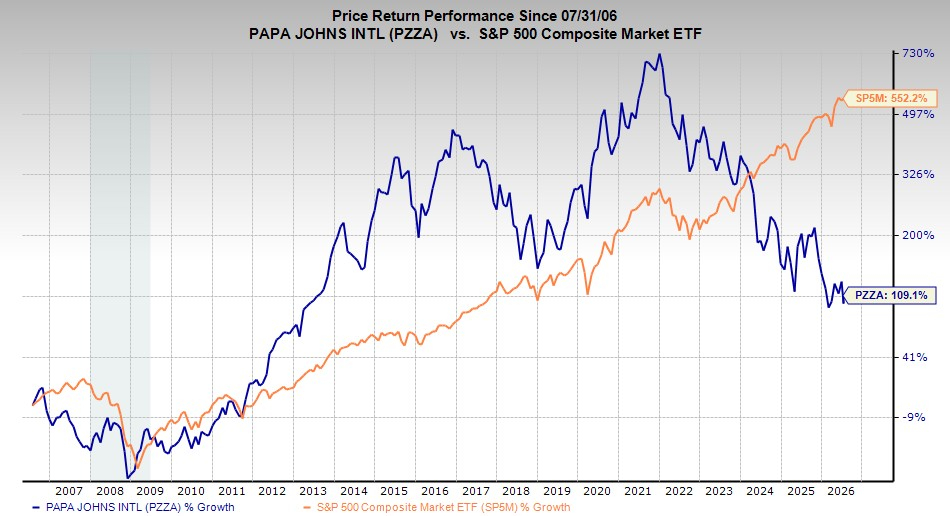

Some buyers would possibly take into account taking a chew out of Papa John’s inventory since it’s already down 70% over the previous 5 years. However it could possibly be greatest for buyers to keep away from Papa John’s shares, at the least for now.

7 Greatest Shares for the Subsequent 30 Days

Simply launched: Specialists distill 7 elite shares from the present listing of 220 Zacks Rank #1 Robust Buys. They deem these tickers “Most Seemingly for Early Value Pops.”

Since 1988, the total listing has overwhelmed the market greater than 2X over with a mean acquire of +23.9% per 12 months. So make sure to give these hand picked 7 your instant consideration.

Domino’s Pizza Inc (DPZ) : Free Inventory Evaluation Report

Papa John’s Worldwide, Inc. (PZZA) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.