Generic medicines stay probably the most vital pillars of worldwide healthcare, however the {industry}’s progress drivers are altering. Whereas conventional small-molecule generics proceed to account for substantial prescription volumes, intense competitors and ongoing worth erosion have decreased their potential to generate significant revenue progress. In consequence, success within the generic drug {industry} more and more depends upon product differentiation fairly than scale alone.

Throughout the sector, producers are investing in areas with greater boundaries to entry, together with biosimilars, complicated generics, specialty injectables and different difficult-to-develop therapies. These classes provide longer progress runways, extra sturdy aggressive positions and stronger margin potential than typical generics. On the identical time, corporations are streamlining operations, optimizing portfolios and allocating capital to merchandise that may assist sustainable progress past the normal commodity-generic mannequin.

Right here, we spotlight three generic drugmakers — Sandoz SDZNY, Teva Prescription drugs TEVA and Viatris VTRS — that seem well-positioned to capitalize on this evolution throughout the {industry}.

Business Description

The Medical – Generic Medication {industry} includes corporations that develop and market chemically/biologically equivalent variations of a brand-name drug as soon as the patents offering exclusivity to branded medication expire. These medication might be divided into generic and biosimilar classes based mostly on their composition. The generic section is managed by a number of massive drugmakers and the generic items of enormous pharma corporations. A number of smaller corporations additionally develop generic variations of branded medication, that are considerably cheaper than the originals. Competitors on this section is stiff, leading to skinny margins for manufacturing corporations. A couple of corporations on this {industry} have some branded medication of their portfolio, serving to them faucet a higher-margin market.

3 Traits Shaping the Way forward for the Generic Medication Business

Lack of Patent Exclusivity Creates New Alternatives: Generic drugmakers rely on the lack of patent exclusivity of branded medicines to deliver lower-cost alternate options to market. An organization might launch a licensed generic model of a branded product, gaining exclusivity over competing generic variations for a number of months. Such alternatives might be notably enticing in complicated generics, which usually require better growth experience and funding than conventional generics. Drugmakers additionally continuously interact in patent litigation to safe earlier entry into the marketplace for generic merchandise.

Past conventional generics, the {industry}’s alternative set is increasing as extra blockbuster biologic medication lose exclusivity. Latest high-profile launches included biosimilars of J&J’s Stelara, Amgen’s Prolia/Xgeva and Regeneron’s Eylea. Drugmakers are additionally advancing biosimilar candidates for Merck’s blockbuster oncology drug Keytruda, which is predicted to lose patent safety in 2028.

Competitors Is Driving a Shift Past Conventional Generics: Competitors stays intense throughout the generic drug market. As soon as a branded drug loses exclusivity, a number of producers usually enter the market, main to cost competitors and margin strain. To achieve a bonus, drugmakers search first-to-file (FTF) standing, which might present a interval of exclusivity earlier than further generic opponents enter. Regardless of these alternatives, the generic market stays crowded, with quite a few filings pending earlier than the FDA and several other generic and biosimilar launches anticipated over the subsequent few years.

In response to persistent pricing strain, corporations are more and more shifting past commodity generics and investing in differentiated merchandise comparable to complicated generics, specialty injectables and biosimilars. These merchandise sometimes require better growth experience and funding, however face fewer opponents and provide stronger margins and extra sturdy income alternatives than conventional generics.

Operational Effectivity & Portfolio Optimization Stay Key Priorities: With pricing strain persisting throughout many generic drug classes, producers are inserting better emphasis on operational effectivity and disciplined capital allocation. Corporations are streamlining product portfolios, discontinuing lower-return packages and focusing sources on merchandise and markets with stronger progress potential. Many drugmakers are additionally investing in manufacturing productiveness, supply-chain optimization and cost-control initiatives to guard profitability. These efforts are serving to corporations offset pricing headwinds in mature generic markets whereas creating monetary flexibility to spend money on higher-growth areas comparable to biosimilars, complicated generics and specialty medicines.

Zacks Business Rank Signifies Gloomy Prospects

The Zacks Medical – Generic Medication {industry} is a small 12-stock group housed throughout the broader Zacks Medical sector.

The group’s Zacks Business Rank is the typical of the Zacks Rank of all of the member shares. The Zacks Medical – Generic Medication {industry} at present carries a Zacks Business Rank #174, inserting it within the backside 29% of the 246 Zacks industries. Our analysis exhibits that the highest 50% of the Zacks-ranked industries outperform the underside 50% by an element of greater than 2 to 1.

Towards this backdrop, we’ll current a number of noteworthy shares. However earlier than that, allow us to have a look at the {industry}’s inventory market efficiency and present valuation.

Business Versus Sector & S&P 500

The Zacks Medical – Generic Medication {industry} has outperformed each the broader Zacks Medical and the S&P 500 Index prior to now yr.

The {industry} has surged about 44% over this era in contrast with the broader sector’s almost 1% progress. In the meantime, the S&P 500 has risen over 29%.

One-Yr Worth Efficiency

Picture Supply: Zacks Funding Analysis

Business’s Present Valuation

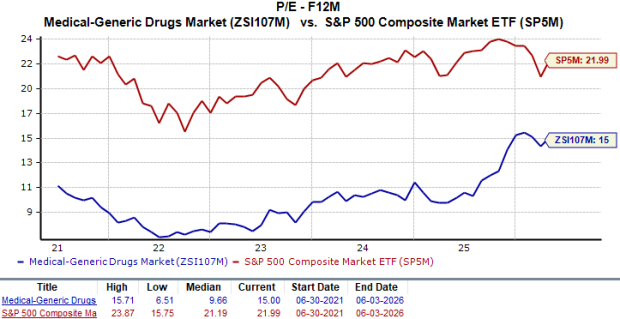

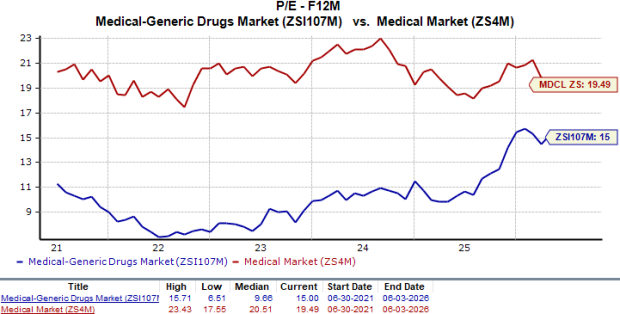

Based mostly on the ahead 12-month price-to-earnings (P/E F12M), a generally used a number of for valuing generic corporations, the {industry} is at present buying and selling at 15X in contrast with the S&P 500’s 21.99X and the Zacks Medical sector’s 19.49X.

Over the previous 5 years, the {industry} has traded as excessive as 15.71X, as little as 6.51X and on the median of 9.66X, because the charts under present.

P/E F12M Ratio

Picture Supply: Zacks Funding Analysis

Picture Supply: Zacks Funding Analysis

3 Generic Drug Shares to Hold an Eye On

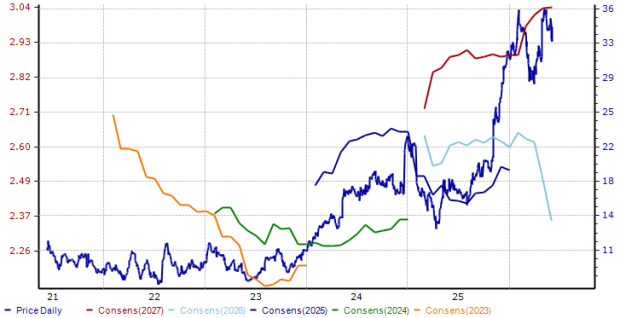

Sandoz: This Swiss-based generic drugmaker was spun off from Novartis in 2023. Throughout the first quarter of 2026, Sandoz achieved web gross sales of $2.76 billion, up 3% yr over yr (excluding Fx). Development was primarily pushed by its biosimilars enterprise, which grew 18%, led by sturdy demand for Afqlir (biosimilar to Eylea), Pyzchiva (biosimilar to Stelara), Jubbonti (biosimilar to Amgen’s Prolia) and Wyost (biosimilar to Amgen’s Xgeva). Biosimilars now account for almost one-third of the corporate’s complete revenues and stay Sandoz’s major progress driver.

Sandoz expects 2026 gross sales to develop at a mid- to high-single-digit charge, supported by current product launches and continued enlargement of its biosimilars portfolio. In March, the corporate expanded its partnership with Samsung Bioepis to develop as much as 5 biosimilars, together with a biosimilar model of Takeda’s Entyvio (vedolizumab). The settlement additional strengthens what administration describes as an industry-leading biosimilars pipeline and positions the corporate to capitalize on a major wave of upcoming biologic patent expirations.

Up to now yr, the inventory has surged 51%. The consensus estimate for 2026 EPS has elevated from $4.11 to $4.13 prior to now 30 days.

Sandoz carries a Zacks Rank #2 (Purchase) at current.

Worth & Consensus: SDZNY

Picture Supply: Zacks Funding Analysis

Teva: This Israel-based firm is the world’s largest generic drug firm, when it comes to each complete and new prescriptions. Teva enjoys a number one place in the US, the world’s largest generic market, the place it instructions a share of greater than 6%. The corporate frequently pursues FTF and first-to-market alternatives and seeks approval for complicated generics, that are more likely to face much less competitors.

The corporate has a rising biosimilars pipeline, with some merchandise being developed in partnership with Alvotech. These embrace Simlandi and Selarsdi, the primary two biosimilars launched in the US below the Teva-Alvotech strategic partnership, which incorporates seven biosimilar candidates. The corporate expects its biosimilars enterprise to generate $800 million in revenues by 2027.

The corporate can also be benefiting from continued progress in its branded medicines portfolio, which incorporates Austedo, Ajovy and Uzedy. These merchandise assist Teva’s ongoing transformation right into a extra diversified biopharmaceutical firm.

The consensus estimate for 2026 EPS has declined from $2.50 to $2.39 prior to now 30 days. The inventory has surged almost 100% prior to now yr. Teva at present carries a Zacks Rank #3 (Maintain).

Worth & Consensus: TEVA

Picture Supply: Zacks Funding Analysis

Viatris: It presents a broad mixture of generics, together with oral solids, injectables and topicals. The corporate’s generic enterprise delivered sturdy efficiency in North America throughout the first quarter of 2026, supported by elevated demand for estradiol, continued momentum from Breyna (generic model of Symbicort) and contributions from lately launched complicated generic merchandise. Viatris additionally benefited from new product launches, comparable to iron sucrose and octreotide, and expects further progress from the deliberate U.S. launch of generic Abilify Maintena later this yr.

Viatris’ branded enterprise, which includes two-thirds of its portfolio, additionally carried out properly. Key merchandise comparable to Creon and Amitiza, together with different established manufacturers, continued to assist income progress.

The inventory has surged 88% prior to now yr. The consensus estimate for 2026 EPS has elevated from $2.44 to $2.47 prior to now 30 days. Viatris carries a Zacks Rank #3 at current.

Worth & Consensus: VTRS

Picture Supply: Zacks Funding Analysis

Radical New Know-how Might Hand Buyers Large Positive factors

Quantum Computing is the subsequent technological revolution, and it might be much more superior than AI.

Whereas some believed the know-how was years away, it’s already current and shifting quick. Massive hyperscalers, comparable to Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to combine quantum computing into their infrastructure.

Senior Inventory Strategist Kevin Prepare dinner reveals 7 fastidiously chosen shares poised to dominate the quantum computing panorama in his report, Past AI: The Quantum Leap in Computing Energy.

Kevin was among the many early consultants who acknowledged NVIDIA’s monumental potential again in 2016. Now, he has keyed in on what might be “the subsequent massive factor” in quantum computing supremacy. At this time, you’ve a uncommon probability to place your portfolio on the forefront of this chance.

See Prime Quantum Shares Now >>

Teva Pharmaceutical Industries Ltd. (TEVA) : Free Inventory Evaluation Report

Viatris Inc. (VTRS) : Free Inventory Evaluation Report

Sandoz Group AG Sponsored ADR (SDZNY) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.