Rebounding additional off its multi-year lows, Lululemon LULU inventory spiked as a lot as +14% in Friday’s buying and selling session after delivering stronger-than-expected Q3 outcomes yesterday night and offering favorable steering.

Nonetheless buying and selling greater than 50% from a 52-week excessive of $423 a share, Lululemon’s Q3 report helped to calm fears of slower demand in its core U.S. market, together with tariff and inflation-related pressures which have squeezed margins.

Additional boosting investor confidence relating to its long-term worth, the retail attire chief licensed a $1 billion inventory repurchase plan. Lululemon additionally introduced its present CEO, Calvin McDonald, will step down by January, with the succession plan being welcomed after a difficult 12 months.

Picture Supply: Zacks Funding Analysis

Worldwide Growth Drives Robust Q3 Outcomes

Pushed by robust worldwide development, Lululemon’s Q3 gross sales elevated 7% 12 months over 12 months to $2.56 billion, exceeding estimates of $2.48 billion by 3%. Asia and Europe fueled the expansion specifically, displaying Lululemon’s model energy exterior North America, with worldwide markets income rising 33% whereas seeing 18% comparable retailer gross sales development.

Americas section gross sales dipped 2%, with comparable retailer gross sales down 5%. Nonetheless, one other optimistic spotlight included world digital gross sales of $1.1 billion, a 13% improve from Q3 2024, and contributing to 42% of whole income for the quarter.

On the underside line, Q3 EPS of $2.59 got here in 16% above expectations of $2.22 regardless of declining from $2.87 per share a 12 months in the past.

Lululemon’s Raised Steerage

Elevating its full-year steering, Lululemon now expects annual gross sales at $10.96-$11.05 billion, up from prior forecasts of $10.85-$11 billion and above the present Zacks Consensus of $10.95 billion or 3% development. EPS targets had been elevated to a spread of $12.92-$13.02, from earlier steering of $12.77-$12.97 and above consensus estimates of $12.91, or a 12% lower.

Monitoring Lululemon’s Operational Effectivity

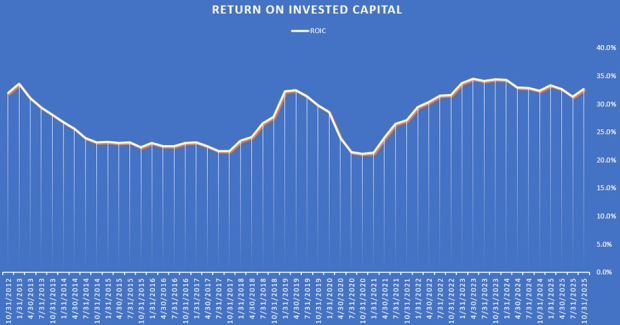

Lululemon’s working margins slipped to 17%, down from 20.5% within the comparative quarter. That stated, Lululemon’s retailer growth correlates with its excessive return on invested capital (ROIC) of 32%. Lululemon opened 14 new shops throughout Q3, bringing its whole retailer depend to 730 globally.

Lululemon’s ROIC has wavered in recent times, however the general uptick from a 20% ROIC in 2021 additionally signifies the corporate has continued to make use of its capital very effectively to generate earnings.

Picture Supply: Zacks Funding Analysis

You will need to be aware, although, that Lululemon’s free money circulation conversion charge has fallen under the popular vary of 80% or greater (72.9%), making its money technology look weak relative to its internet revenue. The decrease FCF conversion indicators that reported earnings aren’t totally translating into money and is usually seen in corporations which are increasing quickly and have money tied up in receivables, stock, or capital expenditures.

Picture Supply: Zacks Funding Analysis

Conclusion & Last Ideas

Following its stronger-than-expected Q3 report, Lululemon’s inventory lands a Zacks Rank #3 (Maintain). Whereas Lululemon hasn’t set the alarm off relating to liquidity issues and has a comparatively robust steadiness sheet, the attire chief is now not within the high tier of high quality corporations by way of operatinal effectivity.

Nonetheless, the rising ROIC is promising, and hopefully, Lululemon’s worldwide and digital gross sales growth will assist the corporate get again on monitor to the stellar development that captivated traders prior to now. At present ranges, Lululemon’s affordable valuation of 14X ahead earnings is enticing to long-term traders as effectively, even when higher shopping for alternatives are forward after the post-earnings rally.

Zacks’ Analysis Chief Picks Inventory Most Prone to “At Least Double”

Our consultants have revealed their High 5 suggestions with money-doubling potential – and Director of Analysis Sheraz Mian believes one is superior to the others. After all, all our picks aren’t winners however this one might far surpass earlier suggestions like Hims & Hers Well being, which shot up +209%.

See Our High Inventory to Double (Plus 4 Runners Up) >>

lululemon athletica inc. (LULU) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.