Inventory After Black Friday")

With Black Friday gross sales setting a brand new document within the U.S., Dillard’s DDS is a retail inventory to think about that at present holds a spot on the coveted Zacks Rank #1 (Sturdy Purchase) listing.

As a number one division retailer chain that focuses on vogue attire and residential furnishings, Dillard’s inventory is up over +50% 12 months thus far because of stellar earnings which have exceeded analyst expectations and broader optimism tied to Federal Reserve price cuts.

Though DDS trades at a lofty price ticket of over $600 a share, Dillard’s immense profitability and digital presence might result in much more upside. To that time, Dillard’s operates a full e-commerce web site and cell app whereas having one of the environment friendly brick-and-mortar operations of any retail chain.

Picture Supply: Zacks Funding Analysis

Dillard’s Distinctive Enterprise Mannequin

For individuals who are questioning, the main motive Dillard’s is exceptionally worthwhile in comparison with different division retailer chains is that it owns most of its shops somewhat than leasing them. This possession construction reduces ongoing lease bills, stabilizes prices, and offers the corporate priceless belongings on the steadiness sheet. Notably, Dillard’s has been in a position to purchase most of its malls somewhat than leasing as a result of it pursued a long-term, debt-averse enlargement technique that emphasised actual property possession from its very beginnings when founder William T. Dillard opened his first retailer in 1938.

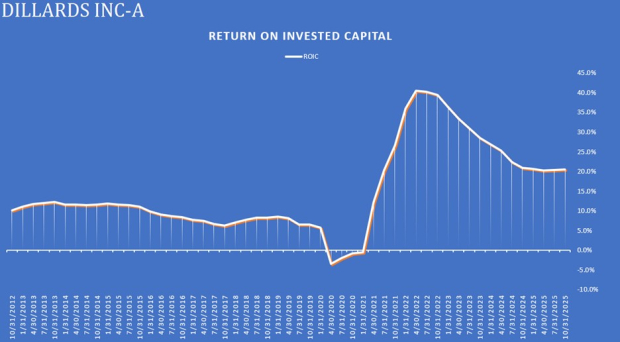

As you may think about, Dillard’s effectivity metrics are very admirable. That is highlighted by a 20% ROIC, a really excessive return on invested capital for a division retailer chain, and above the customarily most well-liked vary of 10-15%. Moreover, Dillard’s has a superb free money stream conversion price of 108%, with an FCF conversion price of 80% or larger illustrating an organization’s means to show its accounting income into precise money out there for reinvestment, debt compensation, or shareholder returns.

Picture Supply: Zacks Funding Analysis

Constructive EPS Revisions

Indicating that now could also be an excellent time to purchase Dillard’s inventory is that EPS revisions for its present fiscal 2026 have risen 5% within the final 30 days from estimates of $30.92 to $32.61. Whereas Dillard’s sturdy backside line is projected to contract in its subsequent fiscal 12 months, FY27 EPS estimates are up over 6% within the final month from estimates of $28.10 to $29.93.

Picture Supply: Zacks Funding Analysis

Dillard’s Modest P/E Valuation

Making the development of rising EPS revisions extra interesting is that Dillard’s inventory nonetheless trades at an affordable 20X ahead earnings a number of. Regardless of being one of the worthwhile firms within the broader retail sector, DDS is at a slight P/E low cost to Kohl’s KSS and isn’t at a stretched premium to Macy’s M 11X.

Picture Supply: Zacks Funding Analysis

Backside Line

Dillard’s has remained a unicorn amongst retail shares and has actually been a portfolio chief for a lot of traders. Optimistically, this may occasionally proceed as Black Friday gave extra solidification to what’s anticipated to be a record-breaking vacation purchasing season, and Dillard’s is prone to capitalize.

Analysis Chief Names “Single Greatest Decide to Double”

From 1000’s of shares, 5 Zacks consultants every have chosen their favourite to skyrocket +100% or extra in months to return. From these 5, Director of Analysis Sheraz Mian hand-picks one to have probably the most explosive upside of all.

This firm targets millennial and Gen Z audiences, producing practically $1 billion in income final quarter alone. A current pullback makes now an excellent time to leap aboard. After all, all our elite picks aren’t winners however this one might far surpass earlier Zacks’ Shares Set to Double like Nano-X Imaging which shot up +129.6% in little greater than 9 months.

Free: See Our High Inventory And 4 Runners Up

Dillard’s, Inc. (DDS) : Free Inventory Evaluation Report

Macy’s, Inc. (M) : Free Inventory Evaluation Report

Kohl’s Company (KSS) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.