SoundHound AI, Inc. SOUN has seen its momentum stall sharply in current weeks. After a risky yr formed by fast AI adoption, high-profile buyer wins and main product enlargement, the inventory has now plunged 22.8% over the previous month, lowering to about $11.78 as of Dec. 3. This slide stands in stark distinction to the broader market. Throughout the identical interval, the Zacks Computer systems – IT Providers {industry} gained 0.3%, the Zacks Laptop and Know-how sector rose 1.2%, and the S&P 500 gained 1.6%.

SOUN Inventory’s 1-Month Efficiency

Picture Supply: Zacks Funding Analysis

SOUN shares at the moment are sitting effectively off its 52-week excessive of $24.98 and modestly above its $6.52 low. The inventory can be buying and selling under each the 50-day shifting common (round $15.75) and the 200-day shifting common (about $12.09) — a technically bearish setup. The downtrend within the shorter-term common slipping beneath the long-term common suggests sellers stay in management. The value trajectory on the chart additionally reveals that earlier momentum in September and October has light, leaving the shares in a weaker technical posture with potential for additional strain until fundamentals reassert themselves.

Picture Supply: Zacks Funding Analysis

SOUN’s Development Momentum Strengthens Regardless of the Pullback

The elemental story behind SoundHound stays one in every of fast enlargement. In accordance with its third-quarter 2025 monetary outcomes, the corporate delivered $42 million in revenues throughout the quarter, rising 68% yr over yr. Throughout the primary three quarters of 2025, the cumulative income hit a report $114 million, representing 127% progress. This surge underscores rising adoption of conversational AI throughout industries that embrace automotive, eating places, monetary companies, IoT gadgets, healthcare, telecom and enterprise buyer help.

Administration’s confidence within the demand trajectory is clear in its upward revision of full-year expectations. The corporate now anticipates $165 million to $180 million in 2025 revenues, a rise from prior projections and a sign that deployments and expansions throughout buyer accounts stay strong.

Tailwinds Supporting SoundHound’s Lengthy-Time period Story

Some of the necessary tailwinds for SoundHound is its broadening buyer attain throughout industries that lend themselves to voice and agentic AI. Latest wins mirror robust momentum. In IoT and robotics, SoundHound signed a significant deal to combine its Chat AI into double-digit hundreds of thousands of gadgets for a big China-based expertise firm. This settlement will prolong its presence into the quickly increasing smart-device market in India. The automotive vertical, regardless of short-term macro strain, continues to undertake its options, with Jeep rolling out SoundHound’s Chat AI voice assistant throughout Europe and a significant world sports-car producer working with the corporate to craft a branded voice persona.

The restaurant section stays an anchor of regular demand. Through the quarter, new deployments included Firehouse Subs, 5 Guys, McAlister’s Deli and full rollouts at Behavior Burger, Pink Lobster and different chains, reinforcing the corporate’s place as a pacesetter in automated voice ordering. Further good points in healthcare and monetary companies, the place organizations adopted or expanded enterprise AI options, additional show the breadth of its business traction.

One other robust tailwind is the expertise basis itself. SoundHound’s platform is constructed round improvements comparable to Speech-to-Which means, Deep Which means Understanding, the multimodal Polaris basis mannequin and the Agentic+ enterprise framework, all of that are designed to execute conversational, generative and deterministic capabilities with excessive velocity and accuracy. The corporate additionally continues to combine and exchange third-party applied sciences inside acquired companies, decreasing price buildings and bettering buyer experiences by internally developed speech fashions and agentic instruments.

The steadiness sheet offers further help. As of the third quarter, SoundHound held $269 million in money and carried no debt, providing monetary flexibility for continued innovation and go-to-market enlargement whereas navigating near-term losses.

Difficult Components That Nonetheless Cloud the Funding Outlook

Even with its spectacular income enlargement, SoundHound additionally faces significant headwinds. The clearest problem is its ongoing battle with profitability. Through the third quarter of 2025, the corporate reported a GAAP web lack of $109.3 million, which was widened partly by non-cash changes associated to acquisition liabilities. On a non-GAAP foundation, the web loss was $13 million, and adjusted EBITDA got here in at a lack of $14.5 million. Whereas the CFO emphasised that scale efficiencies and acquisition synergies ought to enhance margins as the corporate approaches 2026, losses stay large and money utilization is materials.

Money circulate tendencies reinforce the priority. By means of the primary 9 months of the yr, working money outflow totaled greater than $76 million, a stage that highlights the corporate’s must steadiness progress investments with prudent capital allocation because it strikes towards its acknowledged objective of breakeven.

The automotive enterprise introduces further complexity. Administration famous that world tariffs and broader {industry} softness proceed to weigh on automotive income, although it expects enchancment as voice commerce and next-generation deployments scale in 2026. Automotive cycles are usually lengthy and delicate to macro swings, making near-term progress much less predictable than in subscription-based enterprise segments.

SoundHound’s acquisition technique, highlighted most just lately by the acquisition of Interactions, brings each upside and danger. Whereas the acquired enterprise expands workflow orchestration capabilities inside the enterprise agentic suite, integration can pressure near-term bills, and the corporate should show that price synergies and cross-selling alternatives can materialize on the tempo of administration tasks.

Valuation additionally stays a sticking level. SoundHound trades at roughly 21.5X ahead 12-month gross sales, above the {industry}’s 16.54X and above its personal three-year median. Though the market might justify a premium for an rising AI platform with robust progress momentum, the mismatch between the valuation a number of and the corporate’s loss profile raises issues about draw back publicity if income momentum slows.

SOUN’s P/S Ratio (Ahead 12-Month) vs. Business

Picture Supply: Zacks Funding Analysis

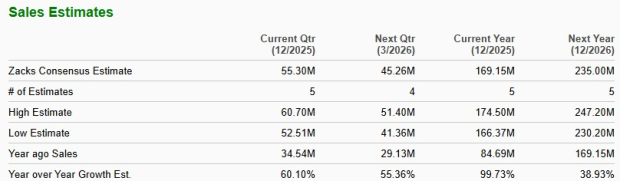

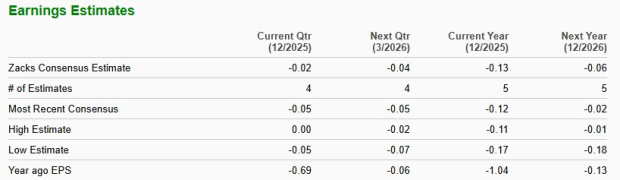

Analyst estimates revisions supply a combined however cautious image. The Zacks Consensus Estimate for SOUN’s loss per share for 2025 stays unchanged, whereas 2026 loss estimates have widened barely, at the same time as income projections proceed to rise nearly 100% for 2025 and almost 39% for 2026. This mixture of stable gross sales forecasts and softening earnings expectations underscores the funding stress — the highest line is accelerating, however the backside line has but to observe.

SOUN’s Gross sales Estimate

Picture Supply: Zacks Funding Analysis

SOUN’s EPS Estimate

Picture Supply: Zacks Funding Analysis

Competitors Intensifies as Voice and Agentic AI Markets Develop

Competitors in voice and agentic AI is tightening, including strain to SoundHound’s current inventory efficiency. Nuance Communications — owned by Microsoft MSFT — stays a strong rival, and Nuance dominates healthcare and contact-center deployments. Nuance constantly units {industry} requirements round accuracy and conversational high quality, conserving aggressive strain excessive. Cerence CRNC is one other main contender, and it continues to guide automotive voice methods with robust OEM partnerships. Cerence nonetheless shapes the embedded voice market SoundHound goals to disrupt. LivePerson LPSN additionally challenges SoundHound, and it competes aggressively in enterprise automation. LivePerson more and more positions itself as a full-stack agentic AI supplier, intensifying the rivalry.

Discount or Pink Flag?

The current selloff displays an uneasy steadiness between SoundHound’s extraordinary progress and its persistent monetary dangers. On the upside, the corporate is scaling quickly throughout numerous industries, elevating expectations for the present yr and reinforcing its management in superior conversational AI. Its basis in proprietary speech fashions, quickly increasing enterprise partnerships and strengthened cross-industry deployments type a compelling long-term narrative.

But the cautionary view is equally grounded. The inventory’s technical breakdown, mixed with widening working losses, heavy money utilization, acquisition-related complexity and a valuation premium, suggests the trail ahead could also be risky. The Zacks Rank #4 (Promote) captures this discomfort, highlighting unfavorable earnings momentum regardless of SoundHound’s robust income outlook.

You’ll be able to see the entire record of right now’s Zacks #1 Rank (Sturdy Purchase) shares right here.

Zacks’ Analysis Chief Picks Inventory Most Prone to “At Least Double”

Our specialists have revealed their Prime 5 suggestions with money-doubling potential – and Director of Analysis Sheraz Mian believes one is superior to the others. In fact, all our picks aren’t winners however this one might far surpass earlier suggestions like Hims & Hers Well being, which shot up +209%.

See Our Prime Inventory to Double (Plus 4 Runners Up) >>

Microsoft Company (MSFT) : Free Inventory Evaluation Report

LivePerson, Inc. (LPSN) : Free Inventory Evaluation Report

Cerence Inc. (CRNC) : Free Inventory Evaluation Report

SoundHound AI, Inc. (SOUN) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.