Regardless of exceeding earnings expectations, Broadcom AVGO and Oracle ORCL inventory have now fallen greater than 15% since their much-anticipated quarterly outcomes final week.

The selloff comes as traders have been spooked by rising prices, margin pressures, and issues about their AI-related spending, though these tech giants have stable steadiness sheets.

Whereas each firms are deeply tied to AI infrastructure, which has been the most popular commerce of the 12 months, the market is now scrutinizing whether or not their elevated spending on information facilities and AI clusters will really ship worthwhile returns.

Picture Supply: Zacks Funding Analysis

Broadcom’s Margin Warning & Lofty Expectations

Reporting blockbuster outcomes for its fiscal fourth quarter final Thursday, Broadcom’s quarterly gross sales had been up 28% to $18.01 billion, with EPS hovering 37% to $1.95 in comparison with $1.42 per share within the comparative quarter. Broadcom additionally beat consensus gross sales and earnings estimates by 2.94% and 4.28% respectively.

Nonetheless, contemplating Broadcom inventory had vastly outperformed the broader market going into its This fall report, this wasn’t sufficient to fulfill traders’ lofty urge for food, particularly with the chip big warning that pricey infrastructure buildouts would decrease gross margins regardless of its surging AI gross sales. It’s noteworthy that AI now accounts for greater than half of Broadcom’s semiconductor income, with the corporate highlighting that AI semiconductor income spiked 74% 12 months over 12 months.

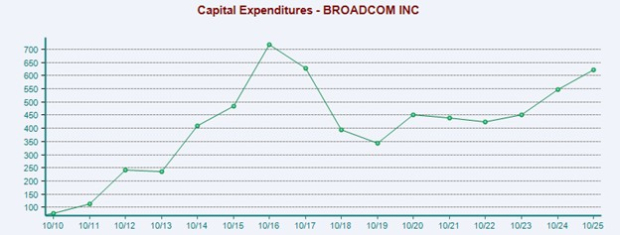

Broadcom has not disclosed a certain amount for its anticipated capital expenditures on AI infrastructure, and its trailing 12-month CapEx of $623 million has been comparatively according to historic averages whereas being far beneath the tens of billions that Oracle and Nvidia NVDA plan to spend. Nonetheless, the dearth of CapEx steerage additionally led to the market’s disappointment, even with Broadcom having profitable multi-billion greenback contracts with AI analysis and improvement firms Anthropic and OpenAI.

Picture Supply: Zacks Funding Analysis

Oracle’s Income Miss & Debt-Fueled AI Spending

Posting combined outcomes for its fiscal second quarter final Wednesday, Oracle’s earnings climbed 54% 12 months over 12 months to $2.26 per share and blasted expectations of $1.63 by 38%. That mentioned, Q2 gross sales of $16.05 billion missed estimates of $16.14 billion regardless of growing 14% from $14.05 billion a 12 months in the past.

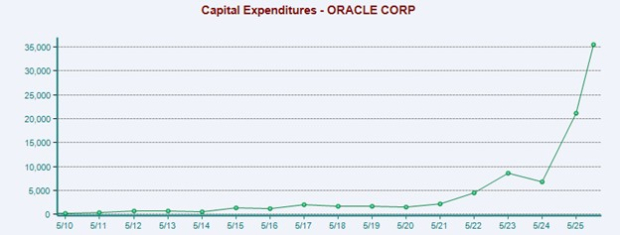

Oracle’s income shortfall has raised some doubts about execution, and this was compounded by the announcement that its CapEx will probably be about $15 billion greater than initially anticipated subsequent 12 months at round $50 billion. Though Oracle has robust cloud and AI deal pipelines, traders are beginning to query whether or not the spending spree is sustainable and if the debt financing could have a future affect on profitability.

Picture Supply: Zacks Funding Analysis

Monitoring Broadcom & Oracle’s Valuation

With Broadcom’s margin stress warning and Oracle’s aggressive spending overshadowing their favorable near-term income steerage and expansive progress trajectories, valuations are as soon as once more the main target as investor sentiment shifts.

Bubble fears aren’t overly regarding concerning their ahead P/E multiples, and the pullback has maybe served as a wholesome correction. To that time, Broadcom’s 39X and Oracle’s 27X are roughly on par with their respective Zacks business averages after not too long ago hitting decade-long highs of 68X and 57X ahead earnings, respectively.

When it comes to price-to-forward gross sales, their valuations are extra worrisome, particularly for Broadcom at 26X in comparison with its Zacks Electronics-Semiconductors Trade common of 5X. Compared, Oracle’s ahead P/S a number of of 8X will not be a far stretch from its Zacks Laptop-Software program Trade common of 4X.

Picture Supply: Zacks Funding Analysis

Optimistically, AVGO and ORCL have hovered close to the popular PEG ratio of lower than 1, which nonetheless suggests they’re on the cusp of being undervalued relative to their progress charges, with Broadcom at the moment beneath this mark.

Picture Supply: Zacks Funding Analysis

Backside Line

Within the grand scheme of issues, traders will nonetheless be compelled at how AI is fueling Broadcom and Oracle’s progress. On the identical time, issues about whether or not they may have the ability to maintain their operational effectivity are comprehensible, contemplating the excessive value of AI infrastructure growth. For now, Broadcom and Oracle inventory each land a Zacks Rank #3 (Maintain).

5 Shares Set to Double

Every was handpicked by a Zacks professional as the favourite inventory to achieve +100% or extra within the months forward. They embody

Inventory #1: A Disruptive Power with Notable Development and Resilience

Inventory #2: Bullish Indicators Signaling to Purchase the Dip

Inventory #3: One of many Most Compelling Investments within the Market

Inventory #4: Chief In a Purple-Scorching Trade Poised for Development

Inventory #5: Trendy Omni-Channel Platform Coiled to Spring

Many of the shares on this report are flying underneath Wall Road radar, which offers an excellent alternative to get in on the bottom ground. Whereas not all picks may be winners, earlier suggestions have soared +171%, +209% and +232%.

Obtain Atomic Alternative: Nuclear Vitality’s Comeback free right now.

Oracle Company (ORCL) : Free Inventory Evaluation Report

Broadcom Inc. (AVGO) : Free Inventory Evaluation Report

NVIDIA Company (NVDA) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.