Power Fuels Inc. UUUU and Cameco Company CCJ are main gamers within the uranium business, every well-positioned to help the worldwide nuclear power provide chain.

Uranium costs lately pulled again to $77 per pound after touching a 14-month excessive of $84 final month, as earlier provide issues eased. Costs are down 3% over the previous 12 months. The long-term outlook for uranium, nonetheless, stays sturdy, pushed by the rising push for clear power. The U.S. Geological Survey’s addition of uranium to its 2025 Essential Minerals Record additional highlights its strategic significance for nationwide safety and home provide chains.

For buyers on this area, lets analyze which uranium inventory is best positioned for upside, Power Fuels or Cameco. A more in-depth have a look at their fundamentals, development drivers and key dangers can provide readability.

The Case for Power Fuels

Power Fuels has been the main U.S. producer of pure uranium focus in recent times, accounting for two-thirds of home manufacturing since 2017. Its White Mesa Mill in Utah is the nation’s solely absolutely licensed and working typical uranium processing facility.

The Pinyon Plain mine in Arizona continues to shine, delivering ore with a mean grade of 1.27% uranium within the third quarter. Per the corporate, it is among the highest-grade uranium mines in U.S. historical past.

Through the quarter, the corporate mined ore containing roughly 465,000 kilos of uranium from its Pinyon Plain and La Sal mines, resulting in a complete of roughly 1,245,000 kilos of contained uranium thus far this 12 months. Pinyon has appreciable exploration upside, with Power Fuels at the moment extracting ore from solely about 25% of the vertical extent of the goal zone.

For full-year 2025, Power Fuels expects to mine 55,000–80,000 tons of ore containing 875,000–1,435,000 kilos of uranium from Pinyon Plain, Pandora and La Sal. Backed by the strong numbers thus far and extra ore anticipated within the fourth quarter, the corporate is positioned to satisfy or exceed the excessive finish of this steering. Completed uranium manufacturing might attain as much as 1,000,000 kilos for the 12 months.

Through the third quarter, Power Fuels bought 240,000 kilos of uranium at a mean value of $72.38 per pound, producing $17.4 million in revenues. Whole revenues have been up 337.6% 12 months over 12 months, pushed by greater uranium gross sales, which offset the decline in costs. Regardless of the income surge, elevated bills resulted in a lack of seven cents per share, unchanged from final 12 months’s third quarter.

Power Fuels ended the third quarter with $298.5 million of working capital, together with $94 million of money and money equivalents, $141.3 million of marketable securities, $12.1 million of commerce and different receivables, $74.4 million of stock and no debt.

The corporate expects to promote 160,000 kilos of uranium within the fourth quarter beneath its present portfolio of long-term utility contracts. In 2026, the corporate expects to promote between 620,000 and 880,000 kilos of uranium beneath its present long-term contracts.

Power Fuels can be advancing heavy uncommon earth aspect (HREE) separation at White Mesa, the place it’s piloting manufacturing of Dy, Tb and different HREE oxides, with business output anticipated in 2026. Its Donald Challenge in Australia is among the richest deposits of HREEs on this planet and is anticipated to begin manufacturing within the second half of 2027. The Toliara Challenge in Madagascar and the Bahia Challenge in Brazil comprise vital portions of sunshine and heavy REE oxides.

Backed by a debt-free stability sheet, Power Fuels is ramping up uranium manufacturing whereas growing vital REE capabilities. Taking present manufacturing ranges and its growth pipeline under consideration, the corporate has the potential to provide 4-6 million kilos of uranium per 12 months.

The Case for Cameco

Cameco, primarily based in Canada, accounted for 16% of world uranium output in 2024 and operates throughout all the nuclear gas cycle, from exploration to gas providers.

Cameco reported a 2% enhance in uranium manufacturing to 4.4 million kilos within the third quarter of 2025. The corporate bought 6.1 million kilos of uranium, 16% decrease than within the third quarter of 2024. This decline, considerably offset by 4% uptick within the Canadian greenback common realized value as a result of affect of fixed-price contracts on the portfolio, led to a 12.8% drop in uranium revenues to CAD 523 million ($379 million). The Gasoline Providers phase witnessed a 24% drop in revenues to CAD 91 million (CAD 66 million), as positive factors from a 42% enhance in common realized costs have been offset by decrease volumes.

General, Cameco’s complete revenues have been down 14.7% 12 months over 12 months to CAD 615 million ($446 million) as a result of quantity declines in each segments. Cameco’s adjusted earnings gained 17% 12 months over 12 months to 5 cents per share within the third quarter.

The corporate’s share of uranium manufacturing is as much as 20 million kilos of uranium (100% foundation) from McArthur River/Key Lake and Cigar Lake in 2025. It had lowered its expectations for the McArthur River mine because of growth delays. Nevertheless, backed by the strong efficiency of the Cigar Lake mine and the McClean Lake mill thus far, the corporate expects to exceed its goal by as much as 1 million kilos and assist offset a number of the manufacturing shortfall at McArthur River.

Cameco revised its full-year goal of uranium deliveries to 32–34 million kilos, from its prior said 31-34 million kilos. In 2024, CCJ delivered 33.6 million kilos of uranium. The corporate has delivered 21.8 million kilos of uranium thus far in 2025. CCJ plans to provide between 13 million and 14 million kgU in its gas providers phase in 2025.

On the finish of the third quarter, CCJ had C$779 million ($565 million) in money and money equivalents, and C$1 billion ($725 million) in long-term debt and a $1 billion ($725 million) undrawn revolving credit score facility. The corporate’s complete debt to complete capital was 0.13 as of Sept. 30, 2025.

Cameco plans to keep up the monetary power and adaptability essential to spice up manufacturing and capitalize on market alternatives. Work is underway to increase the mine life at Cigar Lake to 2036. CCJ can be rising manufacturing at McArthur River and Key Lake to its licensed annual capability of 25 million kilos (100% foundation).

How do Estimates Evaluate for Power Fuels & Cameco?

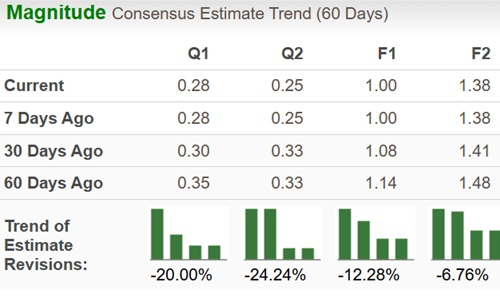

The Zacks Consensus Estimate for Power Gasoline’s 2025 revenues point out a year-over-year drop of 39.8%. The corporate is anticipated to incur a lack of 35 cents per share in 2025, narrower than the lack of 28 cents reported in 2024. The Zacks Consensus Estimate for UUUU’s revenues for 2026 signifies a year-over-year achieve of 85% to $87 million. The estimate for earnings for 2026 is at a lack of six cents per share.

Each the earnings estimates for fiscal 2025 and monetary 2026 for UUUU have moved down over the previous 60 days.

Picture Supply: Zacks Funding Analysis

The Zacks Consensus Estimate for Cameco’s 2025 revenues implies year-over-year development of 6.2%. The consensus mark for earnings of $1.00 per share signifies a year-over-year upsurge of 104%. The Zacks Consensus Estimate for Cameco’s 2026 revenues signifies year-over-year development of 6.5%, with EPS anticipated to realize 38% to $1.38 per share.

Each the EPS estimates for fiscal 2025 and monetary 2026 have been revised downward prior to now 60 days.

Picture Supply: Zacks Funding Analysis

UUUU & CCJ: Value Efficiency & Valuation

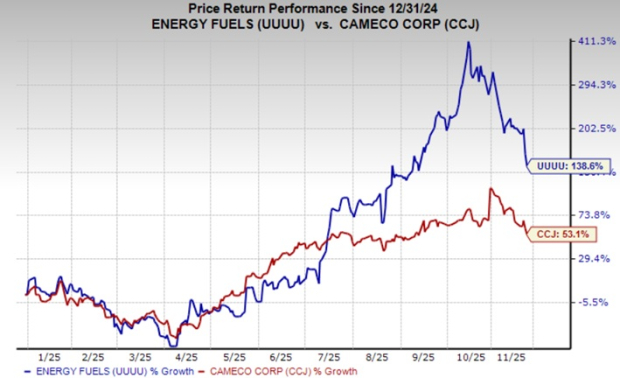

Thus far this 12 months, Power Fuels inventory has appreciated 157.5% outperforming Cameco, which has gained 59.6%.

Picture Supply: Zacks Funding Analysis

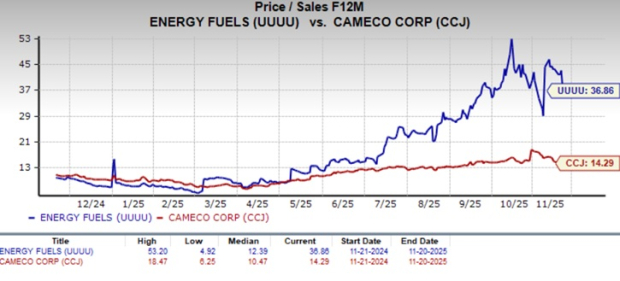

Power Fuels is buying and selling at a ahead price-to-sales a number of of 36.86X, whereas CCJ’s ahead gross sales a number of sits at 14.29X.

Picture Supply: Zacks Funding Analysis

Conclusion

Each corporations face short-term income headwinds from unstable uranium costs. Whereas Cameco advantages from its strong gas providers enterprise and long-term contracts, Power Fuels affords diversification by means of heavy mineral sands and uncommon earths.

With a debt-free stability sheet, sturdy liquidity and distinctive share-price momentum, Power Fuels seems higher positioned for development regardless of its premium valuation. Its diversified asset base and advancing REE tasks improve its long-term potential.

Based mostly on present fundamentals and outlook, Power Fuels, a Zacks Rank #3 (Maintain) affords a extra compelling risk-reward profile than Cameco, which carries a Zacks Rank #4 (Promote).

You may see the whole checklist of at the moment’s Zacks #1 Rank (Robust Purchase) shares right here.

Cameco Company (CCJ) : Free Inventory Evaluation Report

Power Fuels Inc (UUUU) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.