NIKE Inc. NKE is slated to launch second-quarter fiscal 2026 outcomes on Dec. 18. The main sports activities attire retailer is estimated to have witnessed year-over-year declines within the high and backside strains within the fiscal second quarter.

The Zacks Consensus Estimate for fiscal second-quarter revenues is pegged at $12.2 billion, suggesting a 1.7% decline from the year-ago quarter’s reported determine. The Zacks Consensus Estimate for the corporate’s fiscal second-quarter earnings is pegged at 37 cents per share, indicating a decline of 52.6% from the year-ago reported quantity. Earnings estimates for the fiscal second quarter have been unchanged within the final 30 days.

Within the final reported quarter, the corporate delivered an earnings shock of 81.5%. Its backside line beat the consensus estimate by 53.7%, on common, within the trailing 4 quarters.

Earnings Whispers

Our confirmed mannequin doesn’t conclusively predict an earnings beat for NIKE this time round. The mix of a constructive Earnings ESP and a Zacks Rank #1 (Sturdy Purchase), 2 (Purchase) or 3 (Maintain) will increase the chances of an earnings beat. However that’s not the case right here. You possibly can uncover the very best shares to purchase or promote earlier than they’re reported with our Earnings ESP Filter.

NIKE has an Earnings ESP of -3.79% and a Zacks Rank of three. You possibly can see the entire record of immediately’s Zacks #1 Rank shares right here.

What’s in Retailer for NKE in Q2 Earnings?

NIKE has been exhibiting renewed momentum, pushed by disciplined execution of its “Win Now” technique and a gradual restoration in its wholesale order ebook. The “Win Now” initiative represents a fast-track operational reset aimed toward restoring model vitality, cleansing up {the marketplace} and positioning the enterprise for extra sustainable progress following a interval of underperformance.

North America has been NIKE’s strongest area and the early anchor of its turnaround. The area is delivering modest income progress as stock well being improves and shopper demand stabilizes throughout core sports activities classes. Operating, coaching and basketball every posted double-digit good points within the fiscal first quarter, whereas Sportswear is exhibiting early indicators of restoration.

Wholesale progress in North America has been benefiting from normalized cargo timing, expanded distribution and improved sell-through at key companions. Sharper assortments, fewer promotions and upgraded retail presentation have helped strengthen model momentum and engagement. For second-quarter fiscal 2026, our mannequin forecasts North America revenues of $5.2 billion, indicating 0.5% year-over-year progress.

Progress can also be rising internationally. In EMEA, NIKE has largely normalized stock ranges and is shifting towards a extra full-price promoting atmosphere, whilst business promotions stay elevated. Wholesale confidence in EMEA is bettering and the digital enterprise is being refocused on profitability over quantity. Our mannequin initiatives EMEA revenues to rise 1.7% in second-quarter fiscal 2026. In APLA, robust demand for efficiency footwear and tighter stock controls have been supporting more healthy progress developments.

Total, strategic pricing, supply-chain optimization and disciplined stock administration are reinforcing margin restoration. By refining its digital and retail playbook and strengthening wholesale partnerships, NIKE is laying a sturdier basis for worthwhile progress.

NIKE, Inc. Worth and EPS Shock

NIKE, Inc. price-eps-surprise | NIKE, Inc. Quote

Nevertheless, NIKE faces mounting near-term challenges throughout a number of fronts. The Sportswear section, traditionally a key revenue engine, stays underneath strain as the corporate intentionally phases down growing old franchises reminiscent of Air Power 1, Dunk and Jordan 1 underneath its “Win Now” technique. Whereas this portfolio reset is essential for long-term model relevance, it’s creating near-term income softness and quantity strain, probably weighing on ends in the to-be-reported quarter.

Higher China continues to be a significant overhang. Structural weak point throughout digital and bodily channels is anticipated to persist via fiscal 2026, pressuring each gross sales and profitability. Given the area’s outsized contribution to earnings, extended softness poses vital dangers to NIKE’s margin restoration. Our mannequin forecasts second-quarter fiscal 2026 Higher China revenues of $1.5 billion, suggesting a 12.7% year-over-year decline.

Margin pressures stay elevated as a consequence of increased tariffs, elevated promotional exercise and an unfavorable channel combine. Administration expects the gross margin to say no 300-375 bps within the quarter, together with a 175-bps tariff affect. It forecasts SG&A {dollars} to rise within the high-single digits, pushed by increased demand creation investments and a low-single-digit rise in working overhead.

Our mannequin initiatives the gross margin at 40.6%, indicating a 300 bps year-over-year fall, alongside a 6.2% year-over-year enhance in SG&A bills tied to stepped-up demand creation investments. In the meantime, the SG&A price is anticipated to extend 270 bps yr over yr to 35.1%.

NIKE’s Worth Efficiency & Valuation

NKE shares have exhibited a deterioration up to now three months, declining as a lot as 6.2%. The inventory has underperformed the business’s fall of 6% and the S&P 500’s progress of 4.3%. Nevertheless, the inventory has outperformed the broader Shopper Discretionary sector’s decline of seven.9% in the identical interval.

Nevertheless, NIKE’s efficiency is notably weaker than that of its shut competitor, Steven Madden SHOO, which has rallied 35.9% up to now three months. Nonetheless, NKE has outperformed Wolverine World Huge WWW and Adidas’ ADDYY declines of 40.2% and seven.7%, respectively, in the identical interval.

NKE’s 3-Month Inventory Efficiency

Picture Supply: Zacks Funding Analysis

On the present value of $67.78, NIKE trades 29.6% above its 52-week low of $52.28. The present value trades 17.8% beneath the 52-week excessive mark of $82.44.

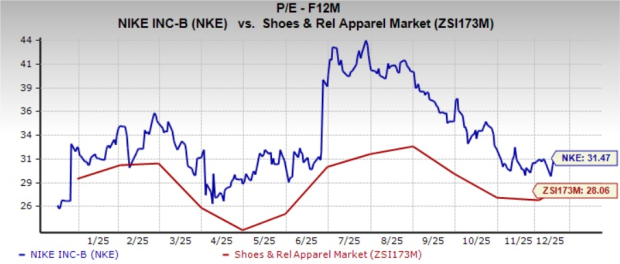

NKE’s valuation seems fairly expensive. The corporate trades at a ahead 12-month P/E a number of of 31.47X, exceeding the business common of 28.06X and the S&P 500’s common of 23.35X.

Picture Supply: Zacks Funding Analysis

Funding Thesis

NIKE’s strategic initiatives are laying a strong basis for long-term progress by reinforcing its aggressive moat, increasing its innovation-led product pipeline and deepening shopper engagement throughout channels. By means of sharper model positioning, a renewed give attention to performance-driven innovation, and improved retail and digital execution, NIKE is adapting to evolving market dynamics whereas preserving its management in world sports activities and way of life attire. The corporate’s “Win Now” technique additional helps this transformation by resetting {the marketplace}, strengthening wholesale partnerships and prioritizing worthwhile progress.

That mentioned, the transition shouldn’t be with out near-term friction. Administration’s delicate steering for second-quarter fiscal 2026 displays ongoing income strain as NIKE phases out legacy way of life franchises and navigates a difficult demand atmosphere. Continued weak point in Higher China and softness in core way of life classes stay key overhangs on the corporate’s near-term efficiency. Whereas these headwinds could weigh on progress within the coming quarters, they seem largely transitional, positioning NIKE for a more healthy, extra sustainable progress trajectory over the long run.

Conclusion

NIKE stands at a essential crossroads. The corporate’s long-term methods, anchored by the “Win Now” initiative, innovation-led product launches, wholesale re-engagement, and a sharper digital and retail focus, are designed to strengthen model fairness, restore progress momentum and seize evolving shopper demand. These initiatives ought to improve NIKE’s aggressive edge, broaden its world attain and drive sustained progress over time.

Nevertheless, the near-term image is much much less encouraging. The corporate faces persistent headwinds from weak demand in way of life classes, a reset in China, elevated SG&A prices and the structural problem of newly imposed U.S. tariffs, which add a major price burden. Administration’s cautious outlook additional underscores the issue of balancing short-term monetary strain with long-term transformation.

Total, whereas NIKE is well-poised for progress, traders ought to stay aware of the cloudy near-term earnings trajectory.

Zacks Naming Prime 10 Shares for 2026

Wish to be tipped off early to our 10 high picks for the whole thing of 2026? Historical past suggests their efficiency may very well be sensational.

From 2012 (when our Director of Analysis Sheraz Mian assumed accountability for the portfolio) via November, 2025, the Zacks Prime 10 Shares gained +2,530.8%, greater than QUADRUPLING the S&P 500’s +570.3%.

Now Sheraz is combing via 4,400 firms to handpick the very best 10 tickers to purchase and maintain in 2026. Don’t miss your likelihood to get in on these shares once they’re launched on January 5.

Be First to New Prime 10 Shares >>

NIKE, Inc. (NKE) : Free Inventory Evaluation Report

Wolverine World Huge, Inc. (WWW) : Free Inventory Evaluation Report

Adidas AG (ADDYY) : Free Inventory Evaluation Report

Steven Madden, Ltd. (SHOO) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.