Each know-how cycle produces a handful of firms that everybody makes use of however few folks can identify.

Within the synthetic intelligence period, Broadcom has quietly turn out to be precisely that — the corporate designing the {custom} silicon and networking cloth that powers the AI ambitions of Google, Meta, OpenAI, and Anthropic. The inventory is broadly outperforming the key indexes this 12 months with a virtually 40% return.

Because the chipmaker prepares to report fiscal second-quarter outcomes after the shut on Wednesday, it is price stepping again and asking a easy query: figuring out the AI infrastructure cycle is actual and sturdy, is there a better-positioned, extra moderately valued solution to personal it than Broadcom?

Picture Supply: StockCharts

What Makes Broadcom Particular?

It is simple to lump Broadcom in with the broader semiconductor crowd and miss the purpose. Broadcom would not compete head-to-head with Nvidia’s general-purpose GPUs; it designs bespoke AI accelerators — XPUs, within the firm’s parlance — for particular person hyperscalers who need chips tuned to their particular workloads.

That {custom} XPU enterprise grew roughly 140% year-over-year within the fiscal first quarter, and Broadcom now works with six main prospects, together with Google, Anthropic, Meta, and OpenAI, to develop and deploy accelerators constructed for big language mannequin workloads.

Business estimates place Broadcom at roughly 70% of the {custom} AI accelerator design market — a dominant place constructed on deep, multi-year engineering relationships which are terribly tough for a buyer to unwind as soon as established. When your engineers are embedded inside a shopper’s design groups over 18-to-24-month cycles, you are not a vendor; you are a accomplice.

Digging Deeper into Broadcom’s Upcoming Outcomes

The setup into earnings is compelling by itself phrases. Broadcom has guided to second-quarter income of roughly $22 billion, indicating about 47% year-over-year development. The Zacks Consensus Estimate for revenues sits simply barely increased at $22.04 billion.

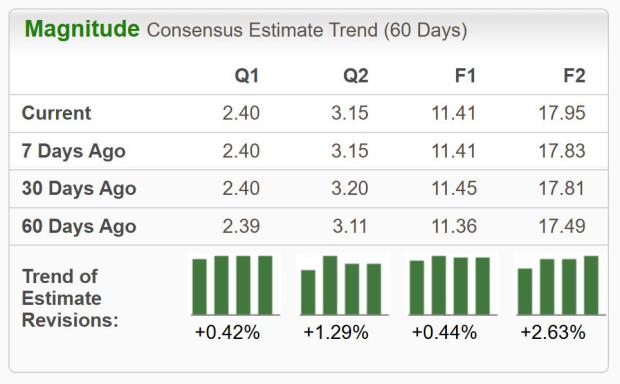

On the underside line, the Zacks Consensus mark for earnings has held regular at $2.40 per share over the previous 30 days, which might characterize roughly 52% development from the year-ago quarter. Earnings rising sooner than an already-torrid income line is strictly what you need to see — it speaks to working leverage and a richening combine.

Picture Supply: Zacks Funding Analysis

And this isn’t an organization that tends to stumble on the end: Broadcom has overwhelmed the Zacks Consensus EPS estimate in every of the trailing 4 quarters, with a mean shock of 1.93%. The beats have been measured slightly than dramatic, which is attribute of a administration crew that guides with self-discipline after which delivers.

Throughout the quarter, the interior combine is the place the AI story actually lives. AI revenues are anticipated to leap roughly 140% year-over-year to $10.7 billion, pushed by {custom} accelerators. The networking aspect — anchored by the 102-terabit Tomahawk 6 swap and 200G SerDes know-how — is capturing hyperscaler demand and is anticipated to characterize round 40% of whole AI income this quarter.

That twin place issues enormously: Broadcom provides each the compute (the XPUs) and the plumbing (the Ethernet switching and optical interconnects) that hyperlink 1000’s of chips inside an AI information middle. Pure-play GPU distributors merely can not replicate that structural breadth.

Then there’s the visibility, which is maybe essentially the most underappreciated factor of the complete thesis. Broadcom is carrying an AI-related backlog reported at roughly $73 billion, and administration has publicly focused AI chip income exceeding $100 billion in 2027. These aren’t hopeful projections pulled from skinny air — they’re underpinned by long-term commitments, together with a provide settlement with Google for future TPU generations that reportedly extends by way of 2031.

When a semiconductor firm can level to a five-year dedicated roadmap with essentially the most refined purchaser of AI silicon on the planet, the same old concern about cyclicality begins to look misplaced. The recurring, high-margin software program franchise acquired by way of VMware provides one other layer of ballast, producing the sort of sturdy money circulate that funds each Broadcom’s dividend and its continued shareholder returns.

Backside Line

The longer-term image is genuinely encouraging: the full-year fiscal 2026 income consensus has climbed above $100 billion, with EPS estimates revised increased to round $11.41, implying annual development charges of roughly 60% and 67%, respectively.

Total, Broadcom AVGO affords one thing uncommon — an organization with Nvidia-like publicity to AI infrastructure spending, a defensible 70% share of a fast-growing custom-silicon market, multi-year contracted visibility, and a high-margin software program money machine.

Wednesday’s print is unlikely to settle the talk by itself, however for affected person traders who imagine the AI build-out has years left to run, Broadcom stays some of the compelling — and most quietly important — methods to personal it.

7 Finest Shares for the Subsequent 30 Days

Simply launched: Consultants distill 7 elite shares from the present listing of 220 Zacks Rank #1 Sturdy Buys. They deem these tickers “Most Seemingly for Early Value Pops.”

Since 1988, the complete listing has overwhelmed the market greater than 2X over with a mean achieve of +23.9% per 12 months. So make sure to give these hand picked 7 your instant consideration.

Broadcom Inc. (AVGO) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.