")

DaVita Inc. DVA inventory has soared over 70% in 2026, pushed by back-to-back beat-and-raise performances.

The well being care supplier centered on kidney illness therapies is projected to double its earnings between 2023 and 2027. DVA broke out above its 2025 peaks to new all-time highs after its spectacular first-quarter report on Could 5.

Regardless of its market-crushing YTD efficiency and its stellar 25-year outperformance of the S&P 500 (+3,000% vs. the benchmark’s 550%), DaVita trades at value-stock ranges and at an almost 50% low cost in opposition to its personal highs when it comes to ahead earnings.

DVA’s worth profile ought to be much more attractive because the broader market appears to be like a bit bloated within the brief run.

The medical care firm’s upward earnings revisions earn it a Zacks Rank #1 (Sturdy Purchase). The dialysis companies firm’s EPS outlook showcases its strong upside, pushed by the truth that persistent kidney illness is on the rise.

Finest Shares to Purchase in June and Maintain Ceaselessly

DaVita is a dialysis companies large within the U.S. that’s increasing its world footprint. The agency goals to serve sufferers affected by persistent kidney illness and past. For reference, dialysis is a therapy that filters waste and extra fluid from an individual’s blood when their kidneys are failing.

Picture Supply: Zacks Funding Analysis

DaVita serves roughly 300K sufferers at over 3.2K outpatient dialysis facilities. A big majority (~82%) of its dialysis facilities are situated within the U.S., with roughly 600 unfold throughout 14 different international locations.

The specialty well being care supplier holds a roughly ~38% share of the U.S. dialysis market, which is rising based mostly on easy demographic developments that don’t present indicators of reversing anytime quickly. DVA is benefiting from each an getting older and an more and more unhealthy U.S. inhabitants.

Picture Supply: Zacks Funding Analysis

Diabetes and hypertension are the main causes of kidney failure, in response to the CDC. Roughly 4 in 10 adults with diabetes have persistent kidney illness, whereas about 1 in 5 adults with hypertension undergo from CKD. Total, greater than 1 in 10 (14%) adults aged 18 or older (37 million individuals) have been estimated to have CKD, in response to the CDC.

The Medical Care Companies Inventory’s Earnings Development Outlook

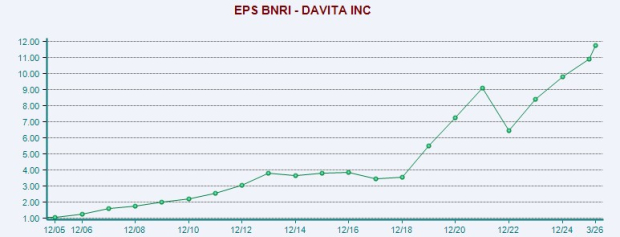

DaVita greater than doubled its adjusted earnings between 2018 and 2021. The corporate has kicked its bottom-line progress again into excessive gear after a 2022 setback, with it projected to greater than double its adjusted EPS from $8.38 a share in 2023 to $18.37 a share in 2027.

The corporate is projected to broaden its adjusted EPS by 40% in 2026 and one other 22% subsequent yr to assist it simply double its 2023 complete. DVA is predicted to develop its income by 5% in 2026 and 4% in 2027.

Picture Supply: Zacks Funding Analysis

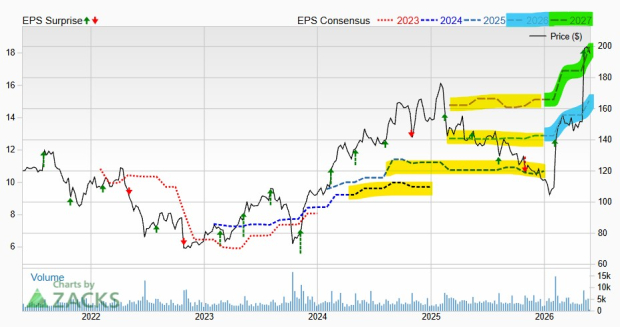

The dialysis firm posted a powerful begin to 2026, topping our Q1 estimate by 19% on Could 5 and offering upbeat steerage.

DVA’s current wave of upward revisions earn it a Zacks Rank #1 (Sturdy Purchase), with its FY27 outlook up 9% since its launch. The post-Q1 positivity extends the upward pattern that started in early 2026, which ended a chronic interval of sideways revisions.

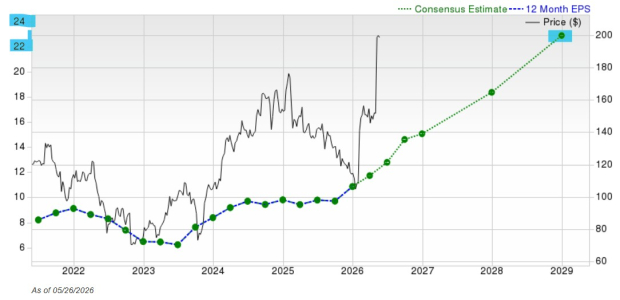

Longer-term traders ought to recognize the chart beneath, highlighting DVA’s spectacular EPS progress pattern.

Picture Supply: Zacks Funding Analysis

Purchase “Sturdy Purchase” Inventory DVA for Worth, Development, and Upside

DVA inventory soared ~3,000% previously 25 years to blow away the S&P 500’s ~550%. It has lagged the benchmark over the previous 10 years, up simply 150%.

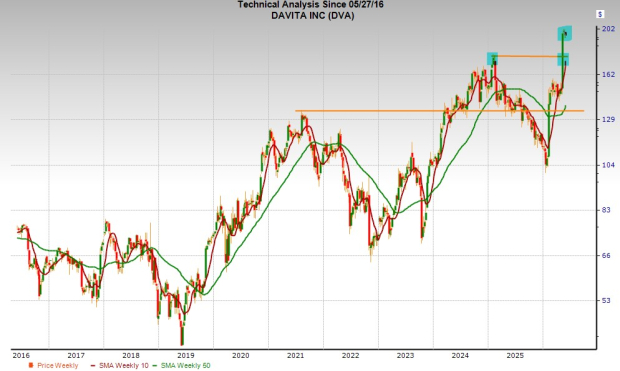

However its 72% YTD run has DaVita buying and selling at new all-time highs, breaking out meaningfully above its early 2025 peaks.

Picture Supply: Zacks Funding Analysis

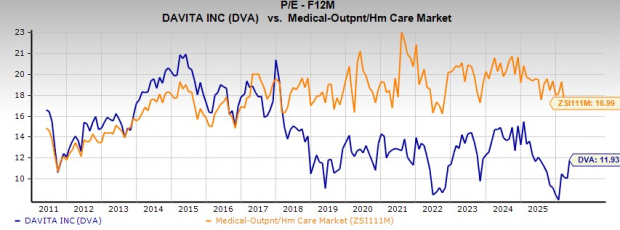

On the valuation entrance, the medical inventory is buying and selling at 45% low cost to its highs and 15% beneath its median at 11.9X ahead 12-month earnings.

DVA’s sturdy earnings outlook is highlighted by the actual fact it trades at a 30% low cost to its highly-ranked Zacks Medical – Outpatient and Residence Healthcare business, regardless that it’s up 360% previously 15 years vs. its business’s 9%.

Picture Supply: Zacks Funding Analysis

The inventory could be a bit overheated from a technical standpoint proper now, and probably due for a cooldown, alongside the remainder of the market.

Any near-term downturn would mark an excellent higher alternative for traders to purchase DaVita inventory.

Radical New Expertise May Hand Traders Enormous Good points

Quantum Computing is the subsequent technological revolution, and it could possibly be much more superior than AI.

Whereas some believed the expertise was years away, it’s already current and transferring quick. Giant hyperscalers, akin to Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to combine quantum computing into their infrastructure.

Senior Inventory Strategist Kevin Prepare dinner reveals 7 fastidiously chosen shares poised to dominate the quantum computing panorama in his report, Past AI: The Quantum Leap in Computing Energy.

Kevin was among the many early consultants who acknowledged NVIDIA’s huge potential again in 2016. Now, he has keyed in on what could possibly be “the subsequent huge factor” in quantum computing supremacy. At the moment, you’ve gotten a uncommon likelihood to place your portfolio on the forefront of this chance.

See High Quantum Shares Now >>

DaVita Inc. (DVA) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.