mohd izzuan/iStock through Getty Photos

Government Abstract

Some institutional buyers who had grown accustomed to outperforming the broader personal fairness composites are discovering they haven’t performed so constantly lately. Their diagnoses of the issue typically heart on particular selections or biases they made of their current supervisor choice, whereas a probable offender is a falloff within the persistence of outperformance amongst personal fairness managers.

Whereas broad efficiency dispersion persists amongst personal fairness funds of a given classic, tutorial analysis means that the tendency for a supervisor’s prior robust efficiency to persist into subsequent funds has largely disappeared, significantly when prior efficiency is predicated on the interim measures used to match funds lower than 10–15 years previous. If this lack of persistence is the “new regular,” will probably be very tough for buyers to anticipate to outperform the personal fairness composites by significant quantities going ahead.

Funding committees ought to encourage establishments to lift the bar for hiring personal fairness managers, as placing cash to work comparatively cheaply within the public markets is a greater funding than paying excessive charges for personal fairness managers they’ve lower than full confidence in.

Learn Half 1 of the Quarterly Letter, What Barbarians Wish to Take Personal (Or: The Dangers in Your Personal Fairness Portfolio), by which Ben Inker and John Pease use many years of buyout knowledge to exhibit how personal fairness portfolios have gotten ever extra targeting a small set of dangers.

My day job at GMO doesn’t straight contain personal fairness past being an observer. However I do wind up discussing personal fairness moderately repeatedly, each with funding committees that I serve on and when invited to talk to the funding committees of different establishments. And in these conditions, I’ve began to note one thing somewhat jarring that is probably not as apparent to funding committee members who solely expertise the efficiency of 1 or two establishments.

It’s well-known that personal fairness has didn’t sustain with the general public markets during the last a number of years. However I additionally appear to be listening to from a lot of establishments that the efficiency of their explicit PE portfolio, which up to now may need performed considerably higher than the Preqin, Cambridge Associates, or different composite, now not appears to be doing so. There may be normally an excuse that feels particular to the establishment in query—“we centered an excessive amount of on co-investment alternatives and didn’t maintain a excessive sufficient bar on our expectations for the precise fund efficiency,” or “we had been too gradual to react to our GPs’ lack of focus and mission creep.”

The implication of these explanations is that fixing a specific downside they diagnose will result in higher relative efficiency sooner or later. However there’s one other rationalization for this phenomenon that’s much less fixable and feels awfully believable to me: if the persistence of efficiency for PE managers has gone away, and even considerably deteriorated, the efficiency distinction between one of the best institutional PE portfolios and the imply is doomed to break down to low ranges. 1 For personal fairness allocations predicated on a perception within the funding employees’s means to search out and safe the easiest personal fairness managers, such a proof would name into query the rationale for the allocation within the first place.

The unique handbook for the endowment mannequin, David Swensen’s Pioneering Portfolio Administration (2009), made no claims about an inherent return premium for personal fairness. Whereas Swensen acknowledged some benefits of personal fairness in precept—higher alignment with buyers, longer time horizons, the deal with working effectivity that comes together with a larger debt load—he identified that personal fairness additionally suffers from excessive charges, principal-agent issues, and the tendency for profitable managers to lift ever-larger funds just for them to underperform their earlier, smaller ones.

He concluded that personal fairness was riskier than public equities because of its excessive leverage and, to one of the best of his data, achieved disappointing median returns over its historical past (pp. 220–235). 2 The case for personal fairness, slightly than resting on some obscure “illiquidity premium,” 3 was all about discovering extraordinary managers. He believed personal property had been a great place to try this, given their a lot wider vary of efficiency throughout managers relative to public equities or fastened revenue.

In apply, producing this alpha for an establishment would contain discovering extraordinary portfolio managers or corporations who can constantly outperform their friends. So the primary query any funding committee ought to ask when discussing an allocation to personal fairness or some other personal asset is: what makes us assured we are able to discover these extraordinary managers and get significant allocations to their funds?

If the committee can’t credibly reply that query, it makes little sense for them to attempt to replicate the asset allocation of establishments that may. However even for establishments which have purpose to assert such a range means, personal fairness fund efficiency actually must be considerably persistent for the sport to work. And it’s removed from clear that such persistence exists.

A number of lecturers have performed attention-grabbing work on the subject, noting that persistence of efficiency has fallen notably since 2000, and extra so for personal fairness than enterprise capital. 4 A very related discovering is that the interim efficiency of funds that haven’t accomplished their life cycles is fully unhelpful in predicting future fund returns, an actual downside since these are the one returns current sufficient to really feel related when contemplating a supervisor’s subsequent fund.

Whereas everyone knows “previous efficiency is just not indicative of future outcomes,” this can be very arduous to overstate how central previous efficiency is to buyers’ decision-making when selecting personal asset managers. You might be shopping for right into a blind pool, and nearly the one factor you understand is what the supervisor did up to now.

Whereas the efficiency of the investments in that earlier pool is just not the one factor you’ll be able to analyze, it feels like essentially the most salient piece of knowledge there’s. However what if that’s an phantasm? A mature personal fairness portfolio will include a number of funds from a number of managers, so the entire variety of totally different funds owned by an establishment will usually be fairly massive, simply a few dozen or extra, even when the establishment has relationships with a comparatively small variety of corporations.

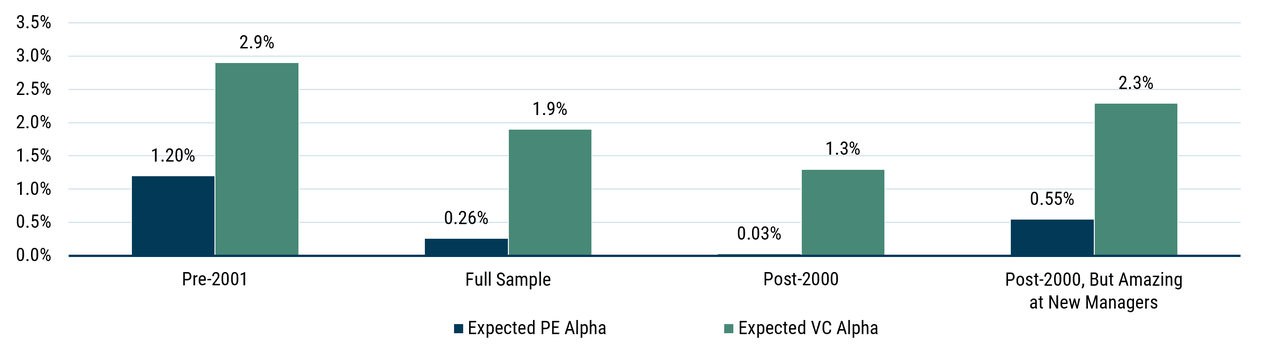

If there really is little persistence in personal fairness fund returns, it implies that even when the vary of returns between the best- and worst-performing funds stays massive, the combination returns for an establishment will nearly at all times be near the median. The chart beneath exhibits the implied alpha of a diversified PE portfolio throughout a number of ranges of efficiency persistence (Braun, Jenkinson, and Stoff 2017).

Impact of Efficiency Persistence on Anticipated PE and VC Alpha

Supply: Braun, Jenkinson, and Stoff (2017) Assumed alpha for quartiles of efficiency is 8%/3.5%/-3.5%/-8% for PE and 12%/4%/-4%/-12% for VC. “Superb at New Managers” assumption is 40%/30%/20%/10% odds of latest managers being in every alpha quartile, and 20% of property in PE/VC invested in such new managers.

I’ve put the enterprise capital leads to as effectively. Whereas there was principally no proof of persistent efficiency within the post-2000 pattern for personal fairness, enterprise capital did present a good quantity of persistence, even when it, too, exhibits considerably much less persistence than the early pattern. I added a fourth column by which I made a pleasant assumption in regards to the new funds that an establishment hires. I assumed that the establishment had a tremendous document in backing new managers, and that these new managers had a 40%/30%/20%/10% likelihood of being within the 1st via 4th quartiles of efficiency.

I additional made the (most likely insanely pleasant) assumption that the establishment’s full 20% PE or VC allocation was invested in such funds (such an establishment may nonetheless not anticipate very a lot alpha from a PE portfolio, although 55 foundation factors is a complete lot higher than the three foundation factors of implied alpha for an establishment that merely reupped with its strongest performers).

It’s doable I’m being unfair in assuming that the fundamental due diligence in selecting to spend money on the brand new funds of present managers is to have a look at the interim efficiency of their earlier funds, however for establishments whose present alpha relative to the PE composite doesn’t look significantly spectacular, I feel it’s honest to ask why you assume it is going to get higher sooner or later.

I’m not attempting to make the case that establishments ought to abandon personal fairness. Truly, if one believes, as I do, that personal fairness is selecting from a small, junky group of corporations, the business’s efficiency has been considerably higher than it appears to be like during the last decade. 5 I additionally consider that investing ability exists, 6 and that it is sensible for well-resourced establishments to take a position with personal fairness managers they really have excessive conviction in. The distinction between one of the best and worst performers amongst personal fairness funds stays massive, and an establishment that may really tilt the percentages in favor of top-quartile outcomes will reap substantial advantages.

However the bar to spend money on a personal fairness supervisor ought to be excessive—arguably even increased than it’s for lively public asset managers, because you’ll be caught paying PE managers excessive charges for a very long time, even when you lose conviction within the interim. And if particular person fund allocations really do have a excessive bar, a goal PE allocation could not even make sense (no less than not past establishing an higher restrict).

If, for instance, you goal 25% of your portfolio in U.S. public equities and may solely give you 10% value of allocations to lively managers you really consider in, you might have the choice to allocate the opposite 15% passively. That passive choice is just not obtainable to you in personal fairness. For those who max out on high-caliber PE managers in need of an total allocation goal, you’ll wind up investing the remainder of your allocation in managers you might have much less confidence in. Paying excessive charges to managers you might have much less confidence in is unlikely to be a great use of capital.

How can the funding committee assist? I feel a great begin can be for the funding committee to ask the funding employees to debate their beliefs about every asset class by which the establishment invests, the aim every serves within the portfolio, how a lot (if any) alpha they anticipate so as to add in every asset class, and, crucially, how they intend to check these beliefs over time. They need to doc their beliefs for every asset class and examine them periodically, maybe each three to 5 years. 7

On the finish of the day, the position of the funding committee is to assist the funding employees do a greater job managing the portfolio. That shouldn’t be about second-guessing particular person supervisor selections, however pushing the funding employees to assume critically about what they do and why is completely within the committee’s wheelhouse. Personal fairness applications should not meant to run on autopilot; there are important inquiries to reply and, for a lot of establishments, disappointing outcomes to grapple with.

1 There’ll nonetheless be a good bit of efficiency dispersion, since most buyers make investments with a comparatively small variety of PE managers, and there’ll nonetheless be loads of variability in precise fund returns. However with out persistence of returns, that variability will wind up largely owing to likelihood, and longer-term returns will are likely to converge.

2 Paraphrased from the 2009 version, which made principally the identical factors as the unique 2000 version (pp. 224–233) with some up to date knowledge.

3 An illiquidity premium for leveraged buyouts (LBOs), no less than, by no means made any sense within the first place. For those who voluntarily take a public firm personal and pay a premium to take action, there isn’t any believable mechanism by which you can probably receives a commission for taking over the illiquidity. The illiquidity is perhaps a way to an finish for another mechanism to realize increased returns, however the concept you’ll usually receives a commission for the truth that the asset is now not liquid is simply foolish when the illiquidity is fully self-imposed.

4 I’m not going to faux to provide a complete itemizing of the analysis, however a few research that stood out to me included Braun, Jenkinson, and Stoff (2017), which checked out efficiency by deal slightly than by fund, serving to to summary away from a number of the fund return calculation issues; and Harris, Jenkinson, Kaplan, and Stucke (2023), which seemed on the downside of interim efficiency calculations that buyers are compelled to depend on given the lengthy lives of funds.

5 See half 1, What Barbarians Wish to Take Personal, for proof of a small, low-quality bias in personal fairness.

6 Admittedly, I’m extremely prone to be biased towards such a perception.

7 The danger in doing that is that it simply turns right into a referendum on which property have performed effectively or badly within the trailing interval, which might be a profound mistake. There may be already an excessive amount of efficiency chasing within the funding world. However placing your beliefs down on paper is extraordinarily vital to keep away from the narrative creep that it’s all too simple to fall into. If ”personal actual property is a good place so as to add alpha” turns into “personal actual property is an inflation hedge,” then into “personal actual property is an under-owned asset class,” and so forth—every rationale changing the final because the thesis fails to play out—whereas the goal allocation stays pretty static, one thing has gone very flawed.

References

Braun, R., Jenkinson, T., & Stoff, I. (2017). How persistent is personal fairness efficiency? Proof from deal degree knowledge. Journal of Monetary Economics, 123 (2), 273–291. https://doi.org/10.1016/j.jfineco.2016.01.033

Harris, R.S., Jenkinson, T., Kaplan, S.N., & Stucke, R. (2023). Has persistence continued in personal fairness? Proof from buyout and enterprise capital funds. Journal of Company Finance, 81 (102361). https://doi.org/10.1016/j.jcorpfin.2023.102361

Swensen, D. (2009). Pioneering Portfolio Administration: An Unconventional Strategy to Institutional Funding, Absolutely Revised and Up to date. Free Press.

Disclaimer: The views expressed are the views of Ben Inker via the interval ending Might 2026 and are topic to alter at any time primarily based on market and different circumstances. This isn’t a suggestion or solicitation for the acquisition or sale of any safety and shouldn’t be construed as such. References to particular securities and issuers are for illustrative functions solely and should not supposed to be, and shouldn’t be interpreted as, suggestions to buy or promote such securities.

Copyright © 2026 by GMO LLC. All rights reserved.

Unique Submit

Editor’s Notice: The abstract bullets for this text had been chosen by Looking for Alpha editors.