Walmart WMT shares couldn’t maintain their spectacular year-to-date momentum following its quarterly outcomes, because the market was disenchanted by the modest steerage downgrade. The steerage concern was largely attributable to excessive gasoline prices, though they reaffirmed earlier gross sales and working earnings expectations.

Walmart shares had loved a formidable run earlier than the quarterly launch, outperforming the broader market by virtually 2X, so some sell-the-news habits could be anticipated. We must always have in mind, nevertheless, that the internals of the Walmart report reconfirm all of the positives which have boosted the inventory over the previous few years and allowed the corporate to briefly be a part of the trillion-dollar market cap membership.

Walmart continued to profit from market share positive aspects and confirmed robust momentum in newer, higher-margin companies equivalent to e-commerce, promoting, market, and membership subscriptions.

The dimensions and scale of Walmart’s operations make it a bellwether for shopper spending developments, which have been within the highlight amid excessive oil costs. Affordability was already a difficulty attributable to cumulative inflation within the post-COVID interval, and the latest rise in gasoline prices has raised issues about reversing the positive aspects made on the inflation entrance over the previous 12 months.

Walmart acknowledged stress in its buyer base, a remark that has a direct read-through to all retailers on deck to report ends in the approaching days. Retailers on deck to report outcomes this week embrace Finest Purchase, Costco, Hole, Kohl’s, Dicks Sporting Items, and others.

A positive read-through from the Walmart report is the robust outcomes from the corporate’s basic merchandise enterprise, which broadly corresponds to discretionary product classes. Administration famous that gross sales developments improved because the quarter progressed, and the positive aspects have been throughout numerous basic merchandise classes, equivalent to attire, gaming, and automotive.

The very robust gross sales efficiency at Goal TGT confirms this favorable studying for Walmart, suggesting that the persistent softness in discretionary spending classes within the post-COVID interval might have run its course. Goal is much extra listed to discretionary product classes than Walmart, although Goal administration was understandably cautious in its outlook given the macroeconomic uncertainty.

The chart beneath reveals the one-year efficiency of Walmart shares (inexperienced line, up +25.2%) relative to Goal (orange line, up +32.4%), the S&P 500 index (pink line, up +31.7%), and the Magazine 7 group (blue line, up +19.2%).

Picture Supply: Zacks Funding Analysis

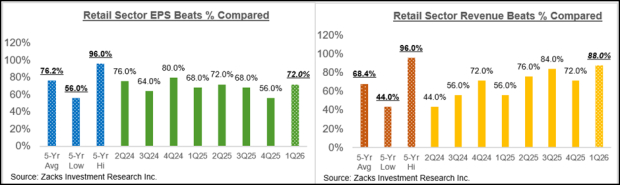

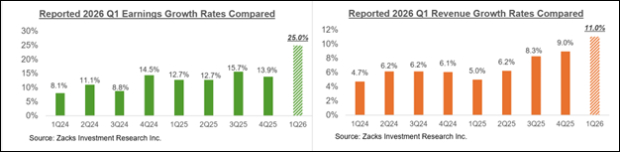

With respect to the Retail sector 2026 Q1 earnings season scorecard, we now have outcomes from 25 of the 31 retailers within the S&P 500 index. Common readers know that Zacks has a devoted stand-alone financial sector for the retail house, in contrast to its placement within the Shopper Staples and Shopper Discretionary sectors within the Normal & Poor’s business classification. The Zacks Retail sector contains not solely Walmart, Goal, and different conventional retailers, but additionally on-line distributors like Amazon AMZN and restaurant gamers.

Complete Q1 earnings for these 25 retailers which have reported are up +3.7% from the identical interval final 12 months on +10.7% increased revenues, with 72% beating EPS estimates and 88% beating income estimates.

The comparability charts beneath put the Q1 beats percentages for these retailers in a historic context.

Picture Supply: Zacks Funding Analysis

As you possibly can see above, the EPS beats percentages for these on-line gamers and restaurant operators are monitoring considerably beneath the historic averages for this group of firms, however income beats are way more quite a few.

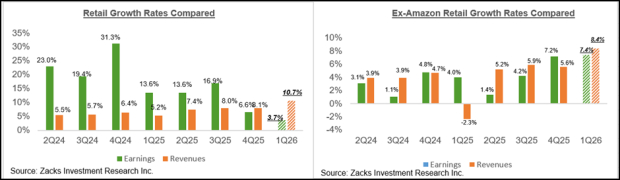

With respect to the earnings and income development charges at this stage, we like to point out the group’s efficiency with and with out Amazon, whose outcomes are among the many 17 firms which have already reported. As we all know, Amazon’s Q1 earnings have been modestly down (-0.8%) on +16.6% increased revenues, because it missed each EPS and top- line expectations.

The 2 comparability charts beneath present the Q1 earnings and income development relative to different latest durations, each with Amazon’s outcomes (left facet chart) and with out Amazon’s numbers (proper facet chart).

Picture Supply: Zacks Funding Analysis

As you possibly can see above, earnings for the group exterior of Amazon are up +7.4% on a +9.4% top-line acquire.

The Earnings Huge Image

The Q1 earnings season reconfirmed the steadily enhancing earnings outlook we’ve constantly highlighted in our earnings commentary.

The blockbuster earnings outcomes from Nvidia stored the highlight on the robust earnings energy of the mega-cap Tech gamers within the Magnificent 7 group, however outcomes have been spectacular throughout all sectors. Most firms comfortably beat the Zacks Consensus EPS and income estimates and are exhibiting accelerating earnings and income development developments.

Most significantly, the substance and tone of administration steerage have largely been reassuring, however the unsure geopolitical backdrop. That is conserving the mixture revisions development constructive, which we focus on in some element afterward.

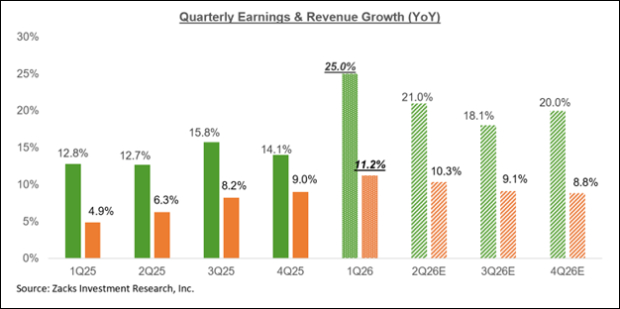

The chart beneath reveals present 2026 Q1 earnings and income development expectations within the context of the place development has been within the previous 5 quarters and what’s anticipated within the coming 4 quarters.

Picture Supply: Zacks Funding Analysis

Common readers of our earnings commentary are acquainted with the steadily enhancing earnings outlook we’ve constantly highlighted over the previous 12 months. This enchancment within the earnings outlook has been pushed largely by the Tech sector over the previous 12 months, with constructive Tech sector estimate revisions offsetting detrimental revisions elsewhere and conserving the mixture revisions development impartial to constructive.

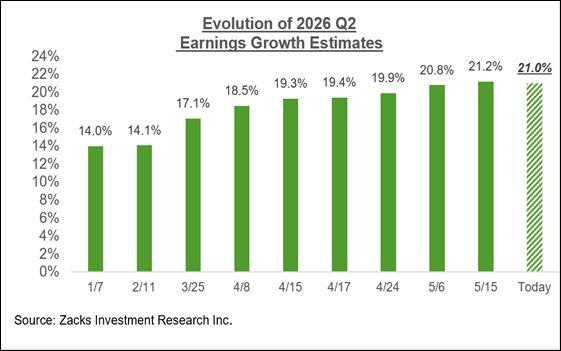

This favorable revisions development has modestly expanded past its Tech-sector core over the past couple of quarters, and we’re seeing that at play for 2026 Q2 as effectively, as proven close by.

As you possibly can see within the above chart, the present expectation is of +21% earnings development in 2026 Q2 on +10.3% increased revenues. The chart beneath reveals how these expectations have advanced in latest weeks.

Picture Supply: Zacks Funding Analysis

Whereas estimates have modestly declined over the previous week, they’re in any other case up for 7 of the 16 Zacks sectors because the quarter received underway. These sectors are: Tech, Power, Primary Supplies, Utilities, Industrials, Retail, and Enterprise Providers.

The constructive revisions development for the Power and Primary Supplies sectors is primarily a perform of the battle within the Persian Gulf and its impact on the availability of oil, LNG, and different commodities.

The improve to Retail sector earnings estimates is primarily a perform of momentum in Amazon’s enterprise, which we group within the Zacks Retail sector. We suspect that elevated oil costs will show to be a big headwind for the sector’s profitability. The detrimental influence on the Retail sector’s earnings outlook will largely be by diminished shopper demand, however the freight/logistics element may even be pressured attributable to excessive oil costs, as we noticed within the Walmart launch.

On the detrimental facet, Q2 estimates have declined for 9 of the 16 Zacks sectors. The sectors struggling essentially the most declines embrace Transportation, Autos, Shopper Discretionary, Building, Finance, and Shopper Staples.

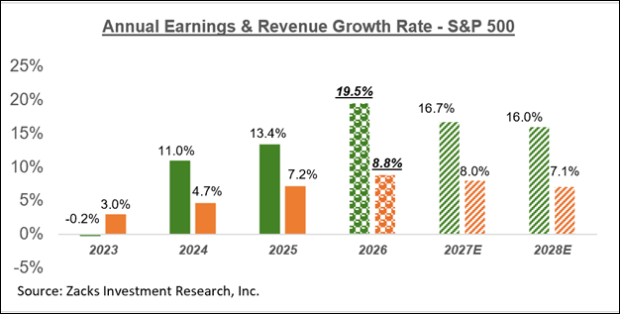

For calendar 12 months 2026, complete S&P 500 earnings are at present anticipated to be up +19.5%, in comparison with +13.4% earnings development final 12 months and +16.7% anticipated subsequent 12 months.

All 16 Zacks sectors are at present anticipated to get pleasure from constructive earnings development in 2026, a growth that we haven’t seen in a really very long time. The Tech and Power sectors are huge contributors to earnings development in 2026, with +34% and +60.5% earnings development, respectively.

Excluding the Power sector’s substantial contribution, 2026 earnings development for the remainder of the index would +17.6% (vs. +19.5% in any other case. Excluding the Tech sector, index earnings could be up +12.1% in 2026.

The chart beneath reveals the mixture development image on an annual foundation.

Picture Supply: Zacks Funding Analysis

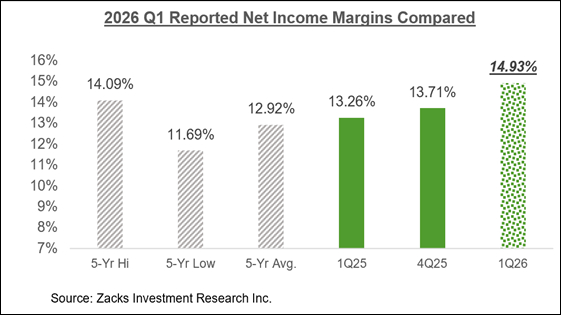

2026 Q1 Earnings Season Scorecard

By means of Friday, Might 22nd, we’ve seen Q1 outcomes from 474 S&P 500 members or 94.8% of the index’s complete membership. Complete earnings for these 474 index members are up +25% from the identical interval final 12 months on +11% increased revenues, with 80.2% beating EPS estimates and 79.1% beating income estimates.

We’ve greater than 100 firms on deck to report Q1 outcomes this week, together with 12 S&P 500 members. We listed earlier the notable retailers reporting this week, however different main firms on deck to report outcomes embrace Salesforce, Dell Applied sciences, HP, Snowflake, and others.

The comparability charts beneath put the expansion charges for the businesses which have reported with what we had seen from this identical group of firms in different latest durations.

Picture Supply: Zacks Funding Analysis

The comparability charts beneath put the Q1 EPS and income beats percentages for this group of firms relative to what we had seen from them in different latest durations.

Picture Supply: Zacks Funding Analysis

The chart beneath reveals how internet margins for the 474 index members which have reported Q1 outcomes examine to different latest durations for this identical group of firms.

Picture Supply: Zacks Funding Analysis

For an in depth take a look at the general earnings image, together with expectations for the approaching durations, please take a look at our weekly Earnings Tendencies report >>>>Tech and Power Contribute Closely to Optimistic Earnings Outlook

7 Finest Shares for the Subsequent 30 Days

Simply launched: Consultants distill 7 elite shares from the present record of 220 Zacks Rank #1 Robust Buys. They deem these tickers “Most Doubtless for Early Value Pops.”

Since 1988, the total record has crushed the market greater than 2X over with a median acquire of +23.9% per 12 months. So be sure you give these hand picked 7 your fast consideration.

Amazon.com, Inc. (AMZN) : Free Inventory Evaluation Report

Goal Company (TGT) : Free Inventory Evaluation Report

Walmart Inc. (WMT) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.