Traders searching for offers, worth, and probably flat-out low-cost know-how shares to purchase proper now may wish to take into account Salesforce CRM inventory.

The enterprise software program inventory is down over 50% from its 2024 peaks, whereas buying and selling at a 30% low cost to Tech and over 95% under its highs at 17.9X ahead 12-month earnings—despite the fact that CRM has climbed ~2,300% up to now 20 years vs. Tech’s ~1,100%.

Wall Road is rising more and more apprehensive that the fast rise and development of AI will make Salesforce’s enterprise software program choices progressively out of date. However Salesforce shouldn’t be rolling over and letting AI slowly destroy its enterprise; it’s adapting with AI and churning out spectacular development, poised to almost double its income and 3x its earnings between 2022 and 2027.

CRM is buying and selling at a few of its most oversold RSI ranges for the reason that 2022 tech selloff and the 2008/2009 monetary disaster, whereas the Nasdaq is buying and selling at a few of its most overbought.

Salesforce can be looking for help at a probably key technical vary highlighted under in blue.

After all, Salesforce may by no means return to its highs, which supply 100% upside from its present worth. The corporate might certainly show unable to navigate the AI age and all of the unknowns and modifications.

Nonetheless, it is perhaps price constructing a starter place within the beaten-down tech inventory as a result of, because the outdated saying goes, be grasping when others are fearful.

Picture Supply: Zacks Funding Analysis

Salesforce is about to announce its first-quarter outcomes on Wednesday, Could 27. Some may wish to wait till after its launch earlier than they purchase, or nibble now in case CRM impresses.

Finest Tech Shares to Purchase Now and in June?

Salesforce’s rising portfolio helps gross sales, advertising and marketing, commerce, buyer and shopper engagement, analytics, app growth, and far more.

The enterprise software program and SaaS vanguard’s days of large YoY development are over because it closes in on $50 billion in yearly income. This backdrop, and the top of ultra-low rates of interest, pressured CRM to show its consideration to regular worthwhile development, marked by sturdy earnings enlargement.

Salesforce has reworked right into a mature, regular development agency that went from dropping cash as lately as 2016 to posting sturdy GAAP and adjusted earnings. It additionally began paying dividends in 2024, becoming a member of the likes of Meta and Alphabet, whereas shopping for again inventory.

Picture Supply: Zacks Funding Analysis

None of those efforts matter to Wall Road, nonetheless, if AI eats away at its enterprise and the broader SaaS business.

Salesforce launched its Agentforce AI device in October 2024. Since then, it’s integrated and constructed out its agentic AI choices.

Agentforce reached $800 million in annual recurring income final 12 months (interval ended January 31), up 169% YoY. “We’ve rebuilt Salesforce to change into the working system for the Agentic Enterprise, bringing people and brokers collectively on one trusted platform,” CEO Marc Benioff mentioned in ready This autumn remarks in late February.

The enterprise software program energy grew its income by 10% final 12 months as a part of 10% common gross sales development within the trailing three years.

Picture Supply: Zacks Funding Analysis

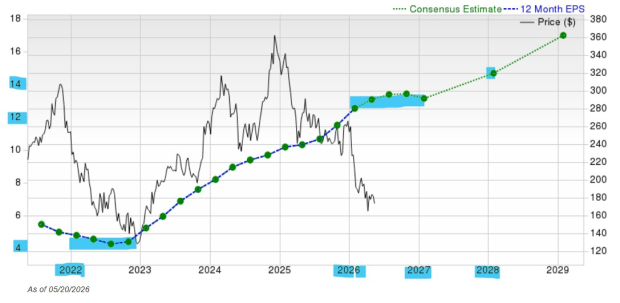

Salesforce mentioned it’s on its option to $63 billion in income in its FY30, boosted by Agentic AI. The corporate is projected to develop its income by 11% this 12 months and 9% subsequent 12 months to $50.32 billion, up from $41.52 billion final 12 months.

CRM expanded its adjusted and its GAAP earnings by ~23% final 12 months. Its earnings estimates have climbed lately, with it projected to increase its adjusted EPS by 5% this 12 months and 12% subsequent 12 months. Salesforce is then anticipated to ramp up its bottom-line development by an much more spectacular clip (see chart above).

Picture Supply: Zacks Funding Analysis

The inventory is down 20% over the previous 5 years whereas Tech has surged 115%, weighed down by its 50% fall from its 2024 highs. Salesforce’s common Zacks worth goal marks 50% upside from its present stage, and it must climb ~100% to return to its peaks.

CRM inventory has climbed ~2,300% up to now 20 years to blow away Tech’s ~1,100% and Microsoft’s MSFT ~1,750%. Regardless of this long-term outperformance, Salesforce trades at a 30% low cost to Tech, over 95% under its highs, and 20% under Microsoft at 17.9X ahead 12-month earnings

7 Finest Shares for the Subsequent 30 Days

Simply launched: Consultants distill 7 elite shares from the present record of 220 Zacks Rank #1 Sturdy Buys. They deem these tickers “Most Probably for Early Worth Pops.”

Since 1988, the complete record has overwhelmed the market greater than 2X over with a median acquire of +23.9% per 12 months. So remember to give these hand picked 7 your fast consideration.

Microsoft Company (MSFT) : Free Inventory Evaluation Report

Salesforce, Inc. (CRM) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.