Market sentiment pivoted on Thursday as shifting headlines round US-Iran peace talks drove a uneven and blended session throughout asset courses, with equities extending their weekly advance and oil reversing a major intraday achieve on hopes {that a} Hormuz reopening could possibly be approaching.

A dense world information slate, together with a four-year excessive in US Manufacturing PMI, a near-complete collapse within the Philly Fed headline studying, and deeply disappointing companies exercise throughout the eurozone and UK, added layers of complexity to an already headline-sensitive session with out resolving the central query merchants have been asking for weeks: how shut, precisely, is a deal.

Try the foreign exchange information and financial updates you’ll have missed within the newest buying and selling session!

Foreign exchange Information Headlines & Information:

- New Zealand Steadiness of Commerce for April 2026: 1.92B (0.8B forecast; 0.7B earlier)

- Australia S&P World Manufacturing PMI Flash for Might 2026: 50.2 (50.6 forecast; 51.3 earlier)

- Australia S&P World Providers PMI Flash for Might 2026: 47.7 (49.9 forecast; 50.7 earlier)

- Japan Steadiness of Commerce for April 2026: 301.9B (-150.0B forecast; 667.0B earlier)

- Japan Equipment Orders for March 2026: -9.4% m/m (-3.3% m/m forecast; 13.6% m/m earlier); 5.9% y/y (18.0% y/y forecast; 24.7% y/y earlier)

- Japan S&P World Manufacturing PMI Flash for Might 2026: 54.5 (54.0 forecast; 55.1 earlier)

- Japan S&P World Providers PMI Flash for Might 2026: 50.0 (50.7 forecast; 51.0 earlier)

- Australia Client Inflation Expectations for Might 2026: 5.6% (6.3% forecast; 5.9% earlier)

-

Australia Employment Change for April 2026: -18.6k (10.0k forecast; 17.9k earlier)

- Australia Unemployment Fee for April 2026: 4.5% (4.3% forecast; 4.3% earlier)

- New Zealand Credit score Card Spending for April 2026: 2.9% y/y (1.9% y/y forecast; 2.1% y/y earlier)

- Swiss Industrial Manufacturing for Q1 2026: -7.1% y/y (0.5% y/y forecast; -0.7% y/y earlier)

- Euro space Present Account for March 2026: 24.1B (32.0B forecast; 21.09B earlier)

- Euro space S&P World Manufacturing PMI Flash for Might 2026: 51.4 (51.5 forecast; 52.2 earlier)

- Euro space S&P World Providers PMI Flash for Might 2026: 46.4 (48.0 forecast; 47.6 earlier)

- U.Ok. S&P World Manufacturing PMI Flash for Might 2026: 53.7 (53.2 forecast; 53.7 earlier)

- U.Ok. S&P World Providers PMI Flash for Might 2026: 47.9 (51.7 forecast; 52.7 earlier)

- U.Ok. CBI Industrial Traits Orders for Might 2026: -41.0 (-40.0 forecast; -38.0 earlier)

- U.S. Constructing Permits Prel for April 2026: 5.8% m/m (0.5% m/m forecast; -11.4% m/m earlier)

- U.S. Preliminary Jobless Claims for Might 16, 2026: 209.0k (210.0k forecast; 211.0k earlier)

- U.S. Philadelphia Fed Manufacturing Index for Might 2026: -0.4 (19.0 forecast; 26.7 earlier)

- U.S. S&P World Manufacturing PMI Flash for Might 2026: 55.3 (53.0 forecast; 54.5 earlier)

- U.S. S&P World Providers PMI Flash for Might 2026: 50.9 (51.1 forecast; 51.0 earlier)

- Euro space Client Confidence Flash for Might 2026: -19.0 (-22.0 forecast; -20.6 earlier)

- U.S. Kansas Fed Manufacturing Index for Might 2026: 9.0 (9.0 forecast; 10.0 earlier)

Promoted: Day merchants & Scalpers have higher odds of creating nice selections in the event that they’re alerted to market catalysts instantly, like information of a possible US-Iran settlement, instantly. Get the real-time feed that professionals use to catch the information.

Be part of FinancialJuice for Free to study extra!

Disclosure: We might earn a fee from our companions should you enroll via our hyperlinks, at no further price to you.

Broad Market Worth Motion:

Greenback Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Quicker With TradingView

Thursday’s session was formed by a single overriding narrative: the prospect of a US-Iran peace settlement and what it would imply for the Strait of Hormuz. Markets swung round noon after reviews circulated suggesting a remaining draft settlement had been reached through Pakistani mediation, triggering a pointy sell-off in oil and a spike in equities earlier than danger urge for food stabilized into the shut. US financial information added conflicting alerts all through the day, with a traditionally sturdy Manufacturing PMI studying offset by a near-complete collapse within the Philly Fed headline print.

The S&P 500 superior roughly 0.67% to shut round 7,446, logging one other achieve for the week. The index navigated a uneven intraday path, dipping towards the 7,395 space through the London session earlier than recovering via the US morning on strong jobs and PMI information, then spiking to a session excessive close to 7,467 across the time of the Iran deal headlines. A modest pullback into the shut nonetheless left equities in constructive territory, with geopolitical optimism outweighing lingering uncertainty about whether or not a deal would really materialize.

WTI crude oil was the session’s standout underperformer, declining roughly 1.19% to shut close to $96.70 per barrel. Oil had rallied sharply via the London session, reaching a excessive above $101.50, earlier than reversing abruptly into and thru the US afternoon. The sharp decline carefully tracked the timing of the Iran deal headlines, which can have triggered hypothesis a couple of potential Hormuz reopening and the resumption of regular tanker flows. Oil’s internet loss on the day, from what had been a major intraday achieve, underscored how delicate vitality markets stay to any perceived change within the battle’s trajectory.

Gold ended primarily flat, up roughly 0.03% to roughly $4,542 per ounce. The dear steel had traded with notable intraday volatility, touching a session low close to $4,489 throughout London hours earlier than recovering via the US afternoon. The near-unchanged shut presumably mirrored competing forces: safe-haven demand tied to ongoing geopolitical uncertainty pulling in opposition to bettering danger sentiment as peace deal optimism grew via the session.

Bitcoin edged modestly increased, gaining roughly 0.38% to round $77,590. The cryptocurrency traded in a large intraday vary between roughly $76,634 and $78,091, with worth motion monitoring broader danger sentiment loosely quite than any crypto-specific catalyst. The muted internet achieve was per a session the place danger urge for food improved however with out the type of broad-based surge that sometimes lifts speculative belongings extra aggressively.

The US 10-year Treasury yield fell roughly 0.76% on the day to round 4.60%, regardless of spending a lot of the sooner session buying and selling increased. Yields climbed into the London open and reached a session excessive close to 4.63% earlier than reversing sharply within the US afternoon, a transfer that appeared to correlate with the Iran deal headlines and the corresponding drop in oil costs. A Hormuz reopening, if realized, would possible cut back the energy-driven inflation premium at present embedded in longer-dated yields, which can assist clarify the magnitude and timing of the reversal.

Promotion: In case your confidence has grown in your market consciousness & methods with this market recap, and also you wanna take motion, Maven Buying and selling will help. They supply simulated funding challenges beginning as little as $15, permitting you to commerce main pairs with professional-sized capital. No deadlines imply you may take swing performs on these market themes with out the stress of a ticking clock.

Study Extra About Maven Buying and selling At this time!

Disclosure: We might earn a fee from our companions should you enroll via our hyperlinks, at no further price to you.

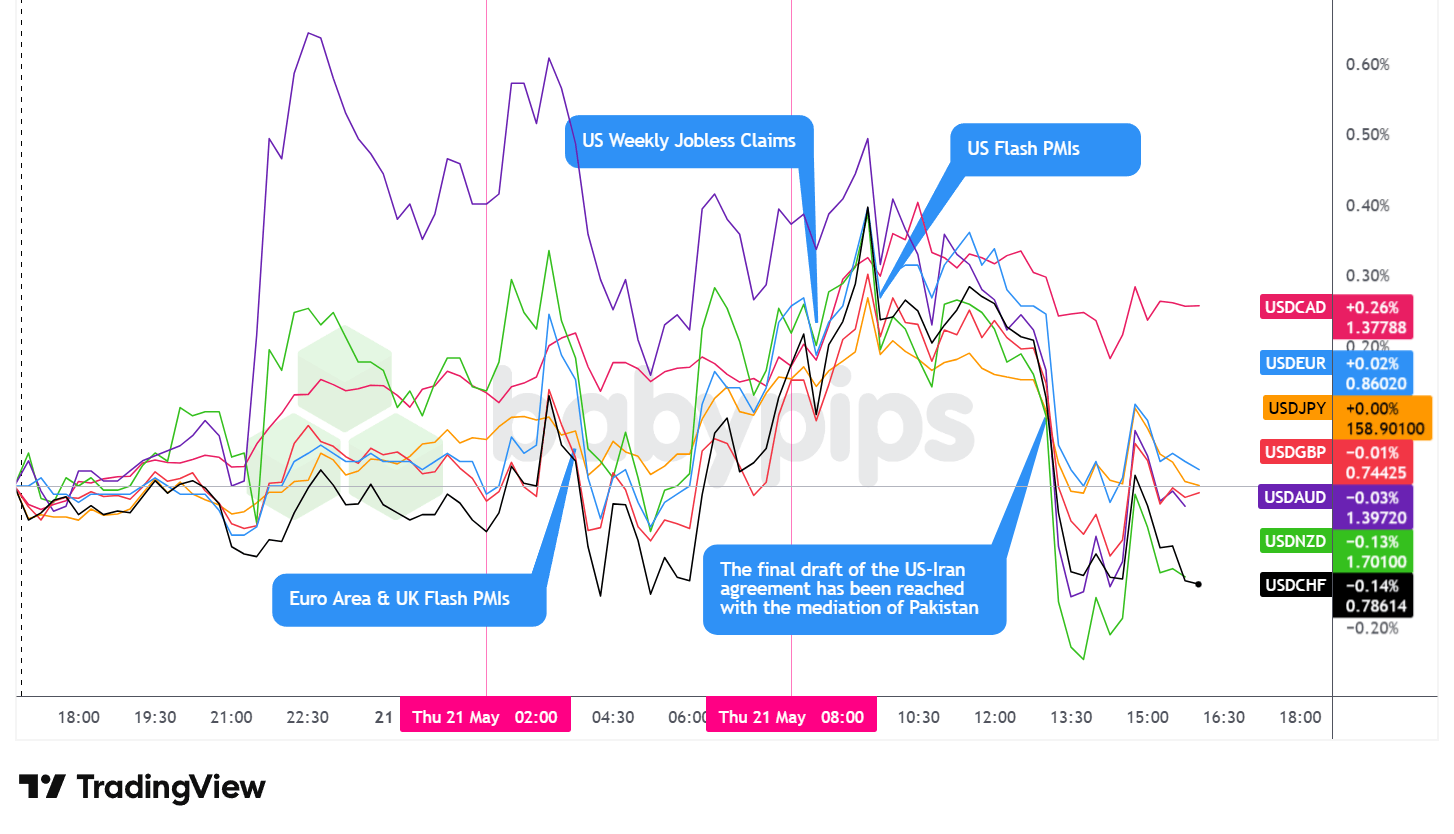

FX Market Habits: U.S. Greenback vs. Majors

Overlay of USD vs. Majors – Chart Quicker With TradingView

The US greenback traded with a broadly firmer tone from the Asian session via the early US morning earlier than a pointy noon pullback tied to Iran deal headlines, in the end closing blended however arguably internet constructive in opposition to the key currencies.

Through the Asian session, the greenback traded internet increased in opposition to the key currencies. The session delivered a heavy information circulation from throughout the Asia-Pacific area, although the broader greenback tone appeared underpinned whatever the particular person releases. Probably the most important catalyst was Australia’s April employment report, which printed a lack of 18,600 jobs in opposition to expectations of a 17,500 achieve, driving the unemployment fee to 4.5%, its highest studying since November 2021. The info triggered a pointy repricing of RBA fee expectations, with August hike likelihood collapsing from round 81% to 42%.

Japan’s commerce information delivered a shock surplus of 301.9 billion yen in opposition to a forecast deficit, as exports surged 14.8% year-on-year, although the headline was sophisticated by a 64% collapse in crude oil import volumes, reflecting provide disruption quite than natural demand enchancment. BOJ board member Koeda’s hawkish remarks, signaling that underlying inflation is round 2% and that charges must proceed rising, offered some incremental assist for the yen.

The London session introduced flash PMI readings throughout the eurozone and UK that painted an image of broadening contraction danger. The euro space companies PMI fell to 46.4, its weakest studying in over two years, whereas the UK companies PMI delivered a pointy miss, sliding to 47.9 from 52.7 in opposition to a 51.7 forecast. Manufacturing held up comparatively higher on either side of the Channel, however the composite readings pointed to deteriorating exercise. ECB sources indicating {that a} June fee hike is almost sure however July off the desk added a nuanced backdrop to European FX. The greenback held its internet increased posture from the Asian session via the London shut.

Through the US session, the greenback initially maintained its firmer tone following the discharge of US Weekly Jobless Claims and the Philly Fed information. Claims got here in at 209,000, barely beneath the 210,000 forecast and increasing their current enchancment. The Philly Fed Manufacturing Index delivered a stark miss, falling to -0.4 in opposition to a 19.0 forecast and a 26.7 prior studying, with new orders additionally contracting sharply.

US Flash PMI information launched shortly after instructed a unique story, with the Manufacturing PMI coming in at 55.3, nicely above the 53.0 forecast, per reporting that US manufacturing expanded at its quickest tempo in 4 years as clients front-loaded orders forward of mounting worth pressures. The conflicting alerts stored the greenback in a uneven however typically agency vary via late morning.

Round 1:00 PM ET, headlines started circulating suggesting a remaining draft US-Iran settlement had been reached through Pakistani mediation, sparking a pointy and fast decline within the greenback in opposition to most main currencies. The reversal appeared per a repricing of geopolitical danger premium tied to hopes of a Hormuz reopening, with oil costs dropping sharply on the identical time. The greenback discovered assist comparatively rapidly, nevertheless, as subsequent commentary, together with Secretary of State Rubio’s characterization of “some good indicators” quite than a confirmed deal, launched warning across the headline. The greenback stabilized and traded uneven via the rest of the session, recovering a significant portion of the noon decline.

At Thursday’s shut, the greenback was blended in opposition to the key currencies however arguably internet constructive for the day, with commodity-linked and safe-haven currencies displaying essentially the most sensitivity to the noon geopolitical headlines.

Promoted: The Technique is Half the Battle; Your Mindset is the Relaxation.

Most buying and selling errors aren’t technical—they’re psychological. Within the traditional “Buying and selling within the Zone” by Mark Douglas (⭐ 4.7★ | 10,000+ opinions on Amazon), you’ll learn to grasp the probabilistic pondering and emotional self-discipline talked about in at present’s article. In case you battle with hesitation or breaking your guidelines, that is your handbook for constant execution.

Click on on the hyperlink to study extra about “Buying and selling within the Zone” by Mark Douglas!

Disclosure: To assist assist our content material, we might earn a fee from our companions should you enroll via our hyperlinks, at no further price to you.

Upcoming Potential Catalysts on the Financial Calendar

- New Zealand Steadiness of Commerce for April 2026 at 10:45 pm GMT

- Australia S&P World Manufacturing & Providers PMI Flash for Might 2026 at 11:00 pm GMT

- Japan Steadiness of Commerce for April 2026 at 11:50 pm GMT

- Japan Equipment Orders for March 2026 at 11:50 pm GMT

- Japan S&P World Manufacturing & Providers PMI Flash for Might 2026 at 12:30 am GMT

- Australia Client Inflation Expectations for Might 2026

- Australia Westpac Main Index for April 2026

- Australia Employment State of affairs replace for April 2026 at 1:30 am GMT

- Financial institution of Japan Koeda Speech at 1:30 am GMT

- New Zealand Credit score Card Spending for April 2026 at 3:00 am GMT

- Swiss Industrial Manufacturing for March 31, 2026 at 6:30 am GMT

- Euro space S&P World Manufacturing & Providers PMI Flash for Might 2026 at 8:00 am GMT

- U.Ok. S&P World Manufacturing & Providers PMI Flash for Might 2026 at 8:30 am GMT

- Euro space Labour Price Index Flash for March 31, 2026 at 9:00 am GMT

- U.Ok. CBI Industrial Traits Orders for Might 2026 at 10:00 am GMT

- U.S. Constructing Permits & Housing Begins for April 2026 at 12:30 pm GMT

- U.S. Preliminary Jobless Claims for Might 16, 2026 at 12:30 pm GMT

- U.S. Philadelphia Fed Manufacturing Index for Might 2026 at 12:30 pm GMT

- Financial institution of England Taylor Speech at 1:00 pm GMT

- U.S. S&P World Manufacturing & Providers PMI Flash for Might 2026 at 1:45 pm GMT

- Euro space Client Confidence Flash for Might 2026 at 2:00 pm GMT

- U.S. Kansas Fed Manufacturing Index for Might 2026 at 3:00 pm GMT

Japan’s April CPI print in a single day can be watched fastidiously given BOJ board member Koeda’s hawkish commentary Thursday, with a studying above consensus possible reinforcing the case for continued BOJ fee hikes and including stress to USD/JPY.

UK Retail Gross sales Friday morning will entice consideration given Thursday’s UK companies PMI collapse to 47.9, with the info probably shedding additional gentle on the diploma of client softness within the UK economic system.

The College of Michigan Client Sentiment Index can be monitored for indicators of US client nervousness round vitality costs, notably related given Walmart’s warning Thursday that rising gas prices are squeezing margins and will translate to increased costs for customers.

Fed Governor Waller’s 3:00 PM GMT look can be carefully watched for any up to date steerage on the speed path, given Thursday’s contradictory information alerts: a pointy Philly Fed miss alongside a four-year excessive within the Manufacturing PMI. Any materials growth in US-Iran talks over the weekend or Friday morning stays the dominant wildcard throughout oil, yields, and FX.

Keep frosty on the market, foreign exchange associates!

Thursday’s sharp noon reversal exhibits what most merchants miss: how geopolitical headlines shift the market’s urge for food for danger, and which currencies profit when merchants flip from cautious to optimistic. Premium members can learn our lesson:

📖 Danger-On / Danger-Off: How World Temper Strikes Currencies

Studying this helps you perceive which currencies win when merchants really feel daring, which of them win after they get scared, and how you can verify the chance climate earlier than inserting any commerce.

And should you’re not a Premium subscriber but, now’s an excellent time to enroll.

With Babypips Premium, you get full entry to Faculty of Pipsology classes that provide help to perceive not simply what moved at present, however the structural risk-on/risk-off dynamics that transfer currencies each single day, so you may learn the market’s temper earlier than the following headline hits.

👉 Subscribe to Babypips Premium