Wednesday’s session pivoted on two forces pointing in sharply totally different instructions. President Trump’s assertion that US-Iran peace negotiations are approaching decision despatched crude oil tumbling beneath $100 per barrel and lifted equities and risk-sensitive currencies, whereas minutes from the Federal Reserve’s April 28–29 assembly confirmed a plainly hawkish inner debate, with a majority of officers warning that fee hikes might turn out to be vital if inflation stays persistently above goal.

Take a look at the foreign exchange information and financial updates you’ll have missed within the newest buying and selling session!

Foreign exchange Information Headlines & Knowledge:

- U.S. API Crude Oil Inventory Change for Could 15, 2026: -9.1M (-2.19M earlier)

- Japan Reuters Tankan Index for Could 2026: 8.0 (8.0 forecast; 7.0 earlier)

- Germany PPI for April 2026: 1.7% y/y (1.6% y/y forecast; -0.2% y/y earlier)

-

U.Okay. CPI Development Fee for April 2026: 2.8% y/y (3.0% y/y forecast; 3.3% y/y earlier)

- U.Okay. Core Inflation Fee for April 2026: 2.5% y/y (2.7% y/y forecast; 3.1% y/y earlier)

- Euro space Inflation Fee Last for April 2026: 3.0% y/y (3.0% y/y forecast; 2.6% y/y earlier)

- Euro space Core Inflation Fee Last for April 2026: 2.2% y/y (2.2% y/y forecast; 2.3% y/y earlier)

- U.S. MBA 30-Yr Mortgage Fee for Could 15, 2026: 6.56% (6.46% earlier)

- U.S. MBA Mortgage Functions for Could 15, 2026: -2.3% (-1.7% earlier)

- U.S. EIA Crude Oil Shares Change for Could 15, 2026: -7.86M (-4.31M earlier)

- FOMC Assembly Minutes: The Fed held charges regular at 3½–3¾%, with almost unanimous help, as elevated inflation (PCE at 3.5% in March, pushed largely by Center East conflict-related power costs) outweighed a softening labor market. A majority of contributors flagged that coverage firming might turn out to be applicable if inflation continues working persistently above 2%, and lots of wished to take away easing-bias language from the assertion.

- Throughout the Wednesday US session, the US President Donald Trump mentioned the US was within the “closing phases” of a take care of Iran

- Nvidia reported fiscal first-quarter outcomes after the Wednesday shut: Income of $81.62B vs $78.86 B; Earnings per share at $1.87

Promoted: Day merchants & Scalpers have higher odds of constructing nice choices in the event that they’re alerted to market catalysts straight away, like information of a possible US-Iran settlement, straight away. Get the real-time feed that professionals use to catch the information.

Be a part of FinancialJuice for Free to study extra!

Disclosure: We might earn a fee from our companions if you happen to join by means of our hyperlinks, at no further price to you.

Broad Market Value Motion:

Greenback Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Sooner With TradingView

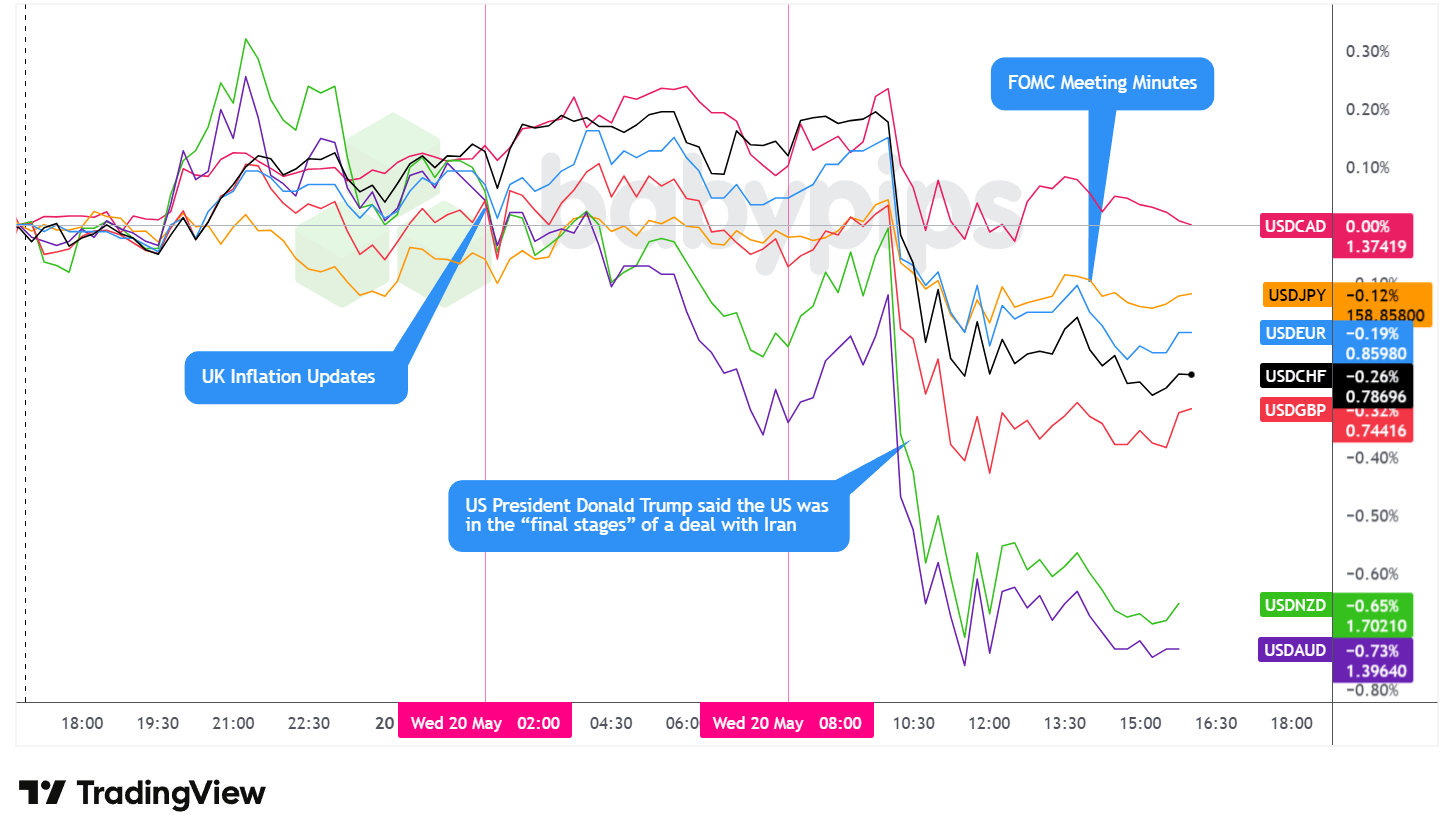

Wednesday’s session was outlined by two headline-driven inflection factors: President Trump’s mid-morning assertion that US-Iran negotiations had been within the “closing phases,” which triggered a pointy repricing throughout power, equities, and charges, and the afternoon launch of hawkish FOMC minutes from the April 28-29 assembly that confirmed a majority of Fed officers have put fee hikes again on the desk.

WTI crude oil suffered the session’s most dramatic transfer, falling roughly 5.29% to close $97.60 per barrel. The selloff had been constructing by means of the in a single day and London periods, with oil declining step by step earlier than accelerating sharply round mid-morning in New York following Trump’s Iran feedback. The intraday low got here close to $96.20 earlier than a partial restoration by means of the afternoon. The EIA crude stock report, launched across the similar time as Trump’s remarks, confirmed a draw of seven.86 million barrels for the week ended Could 15, bigger than the prior week’s 4.31 million barrel draw. That determine would ordinarily have been oil-supportive, however the diplomatic headlines appeared to dominate the worth motion totally, with markets pricing in the potential of resumed Hormuz transit and a gradual normalization of Center East provide.

The S&P 500 gained roughly 1.05%, closing close to 7,428 and halting a three-day shedding streak. The index had drifted step by step larger by means of the European morning earlier than making a pointy leg up across the time of Trump’s Iran feedback, briefly touching a excessive close to 7,437. It then settled into a spread simply above the prior day’s excessive space close to 7,418, absorbing the FOMC minutes with out giving again significant floor. Nvidia’s earnings, anticipated after the shut, supplied an extra layer of focus for fairness merchants given the inventory’s outsized affect on the broader index.

Gold posted the session’s strongest relative efficiency, climbing roughly 1.44% to close $4,546 per ounce. The valuable metallic had been beneath strain throughout the Asian session, sliding towards the $4,453 space, earlier than recovering by means of London commerce after which surging alongside the broader shift in danger sentiment throughout New York hours. Gold touched a session excessive close to $4,553 earlier than consolidating and persevering with to pattern larger by means of the afternoon. Its advance alongside equities might replicate that the FOMC minutes’ hawkish tone sustained safe-haven curiosity whilst danger belongings rallied — one potential interpretation being that markets seen the Iran deal as not but sure sufficient to totally unwind inflation hedges.

Bitcoin posted modest features of roughly 0.87%, buying and selling close to $77,626. The cryptocurrency pushed larger throughout early Asian commerce earlier than ranging broadly by means of the session, dipping briefly across the US open earlier than recovering to shut above the prior day’s excessive space. Its comparatively contained transfer in comparison with the bigger swings in oil and equities presumably mirrored consolidation inside a narrower current vary.

The 10-year US Treasury yield declined roughly 1.95%, settling close to 4.60%. Yields had been elevated throughout the Asian session earlier than starting a gradual descent by means of London. The drop accelerated sharply round mid-morning New York time, correlating with Trump’s Iran feedback and the related repricing of near-term energy-driven inflation danger, with the yield sliding from close to 4.663 to a low close to 4.568. Yields continued drifting decrease by means of the afternoon even after the FOMC minutes bolstered the potential of fee hikes, presumably suggesting the market’s dominant learn was {that a} diplomatic decision to the battle, if realized, would take away the first engine of near-term inflation moderately than implying an imminent tightening cycle.

Promotion: In case your confidence has grown in your market consciousness & methods with this market recap, and also you wanna take motion, Maven Buying and selling may also help. They supply simulated funding challenges beginning as little as $15, permitting you to commerce main pairs with professional-sized capital. No deadlines imply you possibly can take swing performs on these market themes with out the strain of a ticking clock.

Be taught Extra About Maven Buying and selling As we speak!

Disclosure: We might earn a fee from our companions if you happen to join by means of our hyperlinks, at no further price to you.

FX Market Habits: U.S. Greenback vs. Majors

Overlay of USD vs. Majors – Chart Sooner With TradingView

The US greenback closed Wednesday as arguably one of many worst performers among the many main currencies, with many of the harm concentrated within the US session as diplomatic headlines and an total risk-on tone mixed to strain the buck broadly.

Throughout the Asian session, the greenback traded uneven and sideways with an arguably internet bullish lean. No significant regional catalysts drove directional conviction. China’s choice to carry its one-year and five-year mortgage prime charges unchanged for a twelfth consecutive month got here in precisely as anticipated and generated little market response.

The London session opened with the greenback persevering with its broadly sideways, uneven habits. The headline financial launch was the UK April inflation bundle, which got here in beneath expectations throughout the important thing measures: headline CPI printed at 2.8% y/y in opposition to a 3.0% forecast and a previous studying of three.3%, whereas the core fee fell to 2.5% y/y versus 2.7% anticipated. Regardless of the softer UK client inflation information, the greenback didn’t strengthen materially in opposition to the pound, presumably as a result of the UK PPI figures — which beat expectations on the output, core output, and enter measures — supplied a extra hawkish counterpoint to the CPI softness.

Euro space closing CPI for April confirmed the headline at 3.0% y/y, selecting up from 2.6% within the prior month, including to a backdrop of elevated European inflation that saved ECB fee hike hypothesis energetic. By the strategy of the New York open, the greenback had begun dipping extra noticeably in opposition to most pairs.

The US session opened with the greenback trying a short and modest restoration, however the rebound proved short-lived. President Trump’s mid-morning assertion that US-Iran talks had been within the “closing phases” triggered a pointy, broad-based greenback selloff that deepened by means of the London shut.

The FOMC minutes, launched round 2:00 p.m. ET, confirmed the hawkish shift on the April assembly, with a majority of officers signaling openness to fee hikes if inflation runs persistently above 2%. The minutes didn’t reverse the greenback’s decline, presumably as a result of the diploma of Fed hawkishness had already been well-telegraphed in current weeks, leaving the Iran deal optimism because the dominant driver. After the London shut, the greenback stabilized and traded principally uneven and sideways for the rest of the session.

Promoted: The Technique is Half the Battle; Your Mindset is the Relaxation.

Most buying and selling errors aren’t technical—they’re psychological. Within the basic “Buying and selling within the Zone” by Mark Douglas (⭐ 4.7★ | 10,000+ opinions on Amazon), you’ll discover ways to grasp the probabilistic considering and emotional self-discipline talked about in at the moment’s article. If you happen to wrestle with hesitation or breaking your guidelines, that is your handbook for constant execution.

Click on on the hyperlink to study extra about “Buying and selling within the Zone” by Mark Douglas!

Disclosure: To assist help our content material, we might earn a fee from our companions if you happen to join by means of our hyperlinks, at no further price to you.

Upcoming Potential Catalysts on the Financial Calendar

- New Zealand Steadiness of Commerce for April 2026 at 10:45 pm GMT

- Australia S&P World Manufacturing & Companies PMI Flash for Could 2026 at 11:00 pm GMT

- Japan Steadiness of Commerce for April 2026 at 11:50 pm GMT

- Japan Equipment Orders for March 2026 at 11:50 pm GMT

- Japan S&P World Manufacturing & Companies PMI Flash for Could 2026 at 12:30 am GMT

- Australia Client Inflation Expectations for Could 2026

- Australia Westpac Main Index for April 2026

- Australia Employment Scenario replace for April 2026 at 1:30 am GMT

- Financial institution of Japan Koeda Speech at 1:30 am GMT

- New Zealand Credit score Card Spending for April 2026 at 3:00 am GMT

- Swiss Industrial Manufacturing for March 31, 2026 at 6:30 am GMT

- Euro space S&P World Manufacturing & Companies PMI Flash for Could 2026 at 8:00 am GMT

- U.Okay. S&P World Manufacturing & Companies PMI Flash for Could 2026 at 8:30 am GMT

- Euro space Labour Value Index Flash for March 31, 2026 at 9:00 am GMT

- U.Okay. CBI Industrial Tendencies Orders for Could 2026 at 10:00 am GMT

- U.S. Constructing Permits & Housing Begins for April 2026 at 12:30 pm GMT

- U.S. Preliminary Jobless Claims for Could 16, 2026 at 12:30 pm GMT

- U.S. Philadelphia Fed Manufacturing Index for Could 2026 at 12:30 pm GMT

- Financial institution of England Taylor Speech at 1:00 pm GMT

- U.S. S&P World Manufacturing & Companies PMI Flash for Could 2026 at 1:45 pm GMT

- Euro space Client Confidence Flash for Could 2026 at 2:00 pm GMT

- U.S. Kansas Fed Manufacturing Index for Could 2026 at 3:00 pm GMT

Thursday brings a dense lineup of flash PMI readings from Australia, Japan, the eurozone, the UK, and the US, providing the primary Could snapshot of enterprise exercise momentum throughout main economies.

The Australia employment report at 1:30 am GMT will draw explicit consideration given the Australian greenback’s outperformance on Wednesday, with any softness in jobs information doubtlessly testing whether or not AUD’s features can maintain.

The BOJ’s Koeda speech and the BOE’s Taylor speech might appeal to scrutiny given ongoing yen intervention sensitivity and the BOE’s delicate positioning following Wednesday’s softer-than-expected UK CPI print.

Within the US session, weekly preliminary jobless claims and the Philadelphia Fed Manufacturing Index at 12:30 pm GMT arrive in opposition to a backdrop of heightened Fed inflation vigilance bolstered by Wednesday’s minutes, with markets delicate to any indicators of labor market deterioration or financial cooling. The flash US PMIs at 1:45 pm GMT will add additional coloration on whether or not underlying progress momentum is holding or starting to melt beneath the load of elevated power prices.

Keep frosty on the market, foreign exchange associates!

Wednesday’s session confirmed precisely how the bond market, fairness indices, oil costs, and geopolitical danger all moved collectively to form forex flows. However most merchants watch these markets individually, lacking the connections that predicted the greenback’s transfer earlier than it occurred. Premium members can learn our lesson:

📖 What Is Intermarket Evaluation?

Studying this helps you perceive how Treasury yields have an effect on forex actions, why rising bond yields supported the greenback whereas pressuring equities and gold, and tips on how to learn shares, bonds, commodities, and currencies collectively so that you see the total image earlier than putting any commerce.

And if you happen to’re not a Premium subscriber but, now’s a superb time to enroll.

With Babypips Premium, you get full entry to Faculty of Pipsology classes that assist you perceive not simply how particular person markets transfer, however how they drive one another and form forex flows earlier than value motion even seems in your chart.

👉 Subscribe to Babypips Premium