After greater than a decade of disciplined budgeting and restricted capital expenditure, oil and fuel corporations are opening their wallets once more. The commodity supercycle of the mid-2000s left the business overextended, with bloated deepwater tasks, uneconomic oil sands expansions, and Arctic ventures that by no means panned out. When crude collapsed in 2014, the ensuing hangover ushered in a structural shift towards capital restraint, shareholder returns, and ESG-driven warning that persevered for the higher a part of a decade.

That period seems to be ending. With oil costs hovering close to $100 and no near-term catalyst for a significant pullback, producers are doing one thing they have not finished in years, investing aggressively in new manufacturing. And the largest beneficiaries aren’t the producers themselves, however the corporations that provide the rigs, the frac crews, and the subsea gear that make drilling attainable.

Amongst this group, Valaris (VAL), ProFrac Holding Corp. (ACDC) andHelix Power Options Group (HLX) stand out for sturdy momentum, earnings upgrades and appreciable business tailwinds.

Picture Supply: Zacks Funding Analysis

The Capex Cycle Is Turning and Oil Providers Shares Lead

The parallel to the know-how sector is difficult to disregard. After a short self-discipline section in 2022-2023 marked by layoffs and “12 months of effectivity” mantras, Massive Tech discovered its permission slip in synthetic intelligence and started spending at document ranges. The Magazine 7 are collectively guiding for over $680 billion in capex for 2026, up from roughly $400 billion in 2025, funding knowledge facilities, GPU clusters and AI infrastructure at a tempo that may have been unthinkable two years in the past.

To place that in perspective, whole international oil and fuel capital expenditure throughout all segments, upstream, midstream, and downstream is estimated at roughly $680 billion in 2026. Seven know-how corporations are actually spending as a lot on AI infrastructure as all the international power business spends to search out, produce, transport, and refine the commodity that powers the bodily economic system. However we might see that already sizable power capex rise, which might have a big ripple impact on adjoining industries.

Oil and fuel is getting its personal model of a permission slip, not from a technological paradigm shift, however from geopolitics and provide shortage. The Strait of Hormuz disaster, triggered by the US-Israeli strikes on Iran in late February 2026 and the next regional escalation involving Gulf states has successfully eliminated roughly 20 million barrels per day of transit capability from international markets. WTI crude surged from the mid-$50s at first of the 12 months to properly above $100, and the disruption reveals no indicators of resolving rapidly.

The response from producers has been swift. Diamondback Power, the third-largest Permian operator, deserted its capital self-discipline framework and started including rigs and frac crews. ConocoPhillips raised capex steerage. Continental Sources reversed a deliberate 20% spending lower and as a substitute elevated caped 15% to twenty%. These symbolize a possible strategic shift in how administration groups are interested by reinvestment.

Why Providers and Drilling Shares are Beating Producers

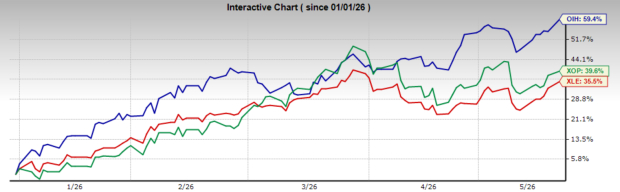

The VanEck Oil Providers ETF (OIH) is up almost 60% year-to-date, nearly doubling the return of the Power Choose Sector SPDR Fund (XLE) at round 36%. The SPDR S&P Oil & Fuel Exploration & Manufacturing ETF (XOP) sits in between at roughly 40%. This dispersion tells an necessary story about the place the true leverage sits in a capex upcycle.

XLE is dominated by built-in majors, ExxonMobil and Chevron alone account for over 40% of the portfolio. These corporations profit from increased oil costs, however their earnings are diversified throughout refining, chemical substances, and midstream operations. That diversification dampens their sensitivity to the upstream drilling cycle. XOP captures purer E&P publicity, however producers are price-takers and their fortunes rise and fall with the commodity itself.

Oil providers corporations function in another way. They receives a commission when producers drill, and so they profit from pricing energy when capability will get tight. SLB, Halliburton, and Baker Hughes, the core holdings of OIH, are picks-and-shovels performs on the drilling cycle. When each E&P within the Permian is scrambling so as to add rigs concurrently, the businesses that personal these rigs and frac fleets can command premium pricing.

The Zacks Rank knowledge confirms this dynamic from the underside up. Scanning the Oils-Power sector, the strongest momentum and earnings revision developments are concentrated in providers and drilling names, comparable to Patterson-UTI, Valaris, Nabors, ProFrac, KLX Power, and Helix Power Options are all clustered close to the highest of the momentum rankings. The E&P corporations sit within the center tier, whereas the built-in majors, the names that dominate XLE, are close to the underside.

This is not coincidental. It is the anatomy of a capex upcycle: the picks-and-shovels names lead on earnings revisions, the producers observe, and the diversified giants lag as a result of their different enterprise segments dilute the upstream sign.

Picture Supply: Zacks Funding Analysis

The Capability Bottleneck Is Actual

What makes this cycle significantly compelling for providers traders is the diploma to which a decade of underinvestment has constrained supply-side capability. Halliburton’s CEO famous on the Q1earnings callthat “white house” within the frac calendar is “all however gone” for Q2, with an uptick in inbound requires spot work. Transocean booked $1.6 billion in new contracts at roughly $410,000 common day charges, the best in over a decade.

That is the pure consequence of years of capital hunger. Rig counts had been slashed, fleets had been cold-stacked, and gear was decommissioned. Rebuilding that capability takes time and capital, which implies the businesses that maintained their fleets by way of the downturn are actually ready to dictate phrases.

The offshore market is telling an analogous story. Deepwater commitments in Brazil’s Santos Basin, Guyana’s Stabroek block, and West Africa aren’t short-cycle spending choices that may be reversed if oil pulls again. These are multi-billion-dollar infrastructure tasks with manufacturing timelines stretching many years. SLB’s Manufacturing Programs phase grew 23% year-over-year in Q1, reflecting the sturdiness of those long-cycle commitments.

ProFrac Holding Corp Shares Push New Highs

ProFrac is a pure-play completions firm centered on hydraulic fracturing, proppant manufacturing, and associated oilfield providers. If there’s a single firm that captures the home land-based capex acceleration story, it is ACDC.

When US producers determine to drill extra wells, they want frac crews to finish them, and ProFrac controls significant capability in that market. The corporate has been by way of a tough stretch with Q1 2026 income of $450 million was down meaningfully from the prior 12 months, and the corporate posted a internet lack of $83.5 million. However the quarter was marred by roughly $9 million in weather-related EBITDA headwinds, and importantly, the trajectory shifted meaningfully in late February as operator sentiment improved and exercise ranges accelerated.

CEO Ladd Wilkes made a degree on theearnings callthat ought to catch traders’ consideration, noting that present pricing stays at roughly 60% of the place it was in 2022, indicating substantial room for value enchancment as demand catches as much as capability. The corporate’s frac calendar has continued to tighten from Q1 ranges, with vital spot work changing to devoted packages, significantly amongst personal operators.

Regardless of the combined outcomes, the inventory is up roughly 63% year-to-date and pushing new YTD highs at this time, reflecting the market’s anticipation of the capex inflection and robust value momentum. But when pricing energy continues to construct as frac capability tightens additional, there’s nonetheless significant earnings revision upside forward. Within the final 60 days, present 12 months estimates are up 10% and subsequent 12 months 33%, giving the inventory a Zacks Rank #2 (Purchase) score.

Picture Supply: TradingView

Valaris Inventory Breaks Out

Valaris is likely one of the world’s largest offshore contract drillers, working a fleet of drillships, semisubmersibles, and trendy jackups throughout deepwater and worldwide markets. The corporate represents the long-cycle, offshore facet of the capex thesis, a basically completely different dynamic than the short-cycle shale performs that dominate home providers.

The story right here begins with the post-bankruptcy transformation. Valaris emerged from Chapter 11 in 2021 with a clear steadiness sheet, and the present offshore upcycle has positioned the corporate squarely within the path of rising demand. Day charges have surged to decade-plus highs as deepwater operators in Brazil, Guyana, and West Africa decide to multi-year drilling packages that can not be simply unwound.

Q1 2026 outcomes confirmed income of $465 million, a top-line beat versus consensus expectations of $446 million, although income was down 25% year-over-year because of fewer working days and the sale of a number of items. The EPS miss (-$0.24 versus expectations of -$0.12) mirrored merger-related integration prices and elevated war-risk insurance coverage bills tied to the Center East battle. Income effectivity remained sturdy at 98%, indicating that when rigs are working, they’re performing reliably. The corporate ended Q1 with $578 million in money and a contract backlog of $4.9 billion.

The transformative catalyst for Valaris is the pending all-stock merger with Transocean, introduced in February 2026. The mixed entity will function a fleet of 73 rigs, together with 33 ultra-deepwater drillships, 9 semisubmersibles, and 31 trendy jackups, with a professional forma enterprise worth of roughly $17 billion and a mixed backlog approaching $11 billion, making the mixed group the world’s largest offshore drilling contractor by fleet measurement.

For traders, the Transocean mixture creates a dominant offshore drilling platform positioned for a multi-year deepwater capex cycle. The mixed fleet may have unmatched attain the world over’s most tasty offshore basins, and the dimensions benefits ought to enhance money stream and speed up deleveraging.

Earnings estimates have risen throughout the board, with present quarter forecasts leaping 37% within the final month and subsequent quarter by 22% in the identical interval, giving it a Zacks Rank #2 (Purchase) score. The inventory additionally simply broke out from a bullish consolidation, making it a worthy candidate for getting shares on a pullback.

Picture Supply: TradingView

Helix Power Options Group Approaches Breakout Degree

Helix Power Options occupies a singular area of interest within the offshore providers worth chain. Whereas corporations like Valaris drill the wells, Helix handles what comes after — properly intervention, subsea robotics, and decommissioning providers. It is the upkeep and lifecycle administration facet of offshore power, which gives a extra sturdy income stream than pure drilling exercise.

The corporate reported Q1 2026 income of $288 million, beating consensus estimates by a significant margin ($24 million above expectations). The quarter mirrored anticipated seasonality, winter climate impacts the North Sea and Gulf of America shelf operations, and included prices from the profitable workover of the corporate’s Thunder Hawk discipline. Regardless of a internet lack of $13 million, Helix generated $59 million in free money stream and ended the quarter with $501 million in money and $612 million in whole liquidity towards simply $310 million in funded debt. That is a notably sturdy steadiness sheet for a corporation of this measurement.

Full-year 2026 steerage requires income of $1.2-$1.4 billion and EBITDA of $230-$290 million, with the second and third quarters anticipated to be probably the most lively. CEO Owen Kratz famous that current commodity value will increase have generated improved demand for the corporate’s providers, and authorities actions within the North Sea have offered a regulatory catalyst for decommissioning exercise.

The strategic catalyst for Helix is the not too long ago introduced all-stock merger with Hornbeck Offshore Providers, anticipated to shut within the second half of 2026. The mixture creates what each corporations describe as a “premier built-in offshore providers firm,” merging Helix’s properly intervention belongings and subsea robotics with Hornbeck’s high-specification offshore help vessel fleet. The mixed entity will function beneath the Hornbeck Offshore Providers identify (ticker: HOS) and is predicted to generate $75 million or extra in annual income and value synergies inside three years. Hornbeck shareholders will personal roughly 55% of the mixed firm, with Helix shareholders holding 45%.

What makes Helix significantly fascinating within the present setting is the diversification of its finish markets. Past conventional oil and fuel, the mixed firm will serve protection, renewables, and scientific analysis purposes, offering some insulation from crude value volatility that pure drillers do not have.

Helix group has seen earnings estimates rise throughout timeframes, incomes it a Zacks Rank #2 (Purchase) score, whereas the inventory concurrently approaches a significant breakout stage.

Picture Supply: TradingView

What Might Derail the Thesis

The bull case for oil providers rests on the sturdiness of the capex cycle. If crude costs stay elevated and producers proceed to take a position, providers corporations will proceed to see sturdy demand and bettering pricing energy. However this thesis will not be with out danger.

The obvious danger is a decision to the Hormuz disaster. A ceasefire or diplomatic breakthrough that reopens the Strait might take $20-30 off crude comparatively rapidly. The reminiscence of $57 oil at first of the 12 months is contemporary, and the Dallas Fed’s newest power survey confirmed loads of E&P executives nonetheless skeptical that present costs will maintain lengthy sufficient to justify main funding commitments. If crude falls sharply, the capex acceleration might stall as rapidly because it began, and providers corporations would give again their outperformance sooner than XLE, given the identical working leverage that drove them increased.

The counterpoint is {that a} decision does not essentially imply quick normalization. Oil analysts have estimated that for day-after-day the Strait is closed, it takes roughly every week for the market to normalize when accounting for tanker fleet dislocations, port backlogs, insurance coverage repricing, and the restart of shut-in manufacturing. The Strait has been successfully closed for 78 days, which factors to roughly 78 weeks of normalization, stretching into November 2027. Saudi Aramco CEO Amin Nasser strengthened this on his Q1earnings name warning that even when Hormuz opened at this time, it could take months to rebalance, and if the reopening is delayed additional, normalization extends properly into 2027.

There’s additionally a historic precedent price noting: OIH’s 10-year return is definitely damaging. The oil providers sector has been probably the most brutal areas of the market over the previous decade, and traders who overstayed their welcome within the 2014 cycle paid dearly for it. It is a sector the place timing and self-discipline matter enormously.

That mentioned, the structural underinvestment argument helps elevated costs even with out the geopolitical premium. The world has not constructed sufficient manufacturing capability to fulfill demand progress, and the capex required to shut that hole flows straight by way of the providers corporations that sit on the middle of this text.

It is also price noting that two of the three corporations profiled above. These aren’t defensive consolidation performs to outlive a downturn. These are offers structured across the perception that the demand setting has legs and that deepwater packages, properly intervention backlogs, and offshore exercise ranges justify constructing bigger, extra succesful platforms to seize multi-year income streams. When administration groups and boards are betting their company construction on a cycle, that tells you one thing about their confidence in its sturdiness.

For now, the earnings revision cycle is pointing clearly in a single path, and the Zacks Rank knowledge is confirming it throughout the providers and drilling advanced. The tech sector discovered its motive to spend. Oil and fuel might have discovered its personal.

Radical New Know-how Might Hand Traders Large Good points

Quantum Computing is the subsequent technological revolution, and it might be much more superior than AI.

Whereas some believed the know-how was years away, it’s already current and transferring quick. Giant hyperscalers, comparable to Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to combine quantum computing into their infrastructure.

Senior Inventory Strategist Kevin Cook dinner reveals 7 rigorously chosen shares poised to dominate the quantum computing panorama in his report, Past AI: The Quantum Leap in Computing Energy.

Kevin was among the many early consultants who acknowledged NVIDIA’s monumental potential again in 2016. Now, he has keyed in on what might be “the subsequent large factor” in quantum computing supremacy. Right this moment, you could have a uncommon likelihood to place your portfolio on the forefront of this chance.

See Prime Quantum Shares Now >>

Valaris Restricted (VAL) : Free Inventory Evaluation Report

State Road Power Choose Sector SPDR ETF (XLE): ETF Analysis Experiences

Helix Power Options Group, Inc. (HLX) : Free Inventory Evaluation Report

State Road SPDR S&P Oil & Fuel Exploration & Manufacturing ETF (XOP): ETF Analysis Experiences

VanEck Oil Providers ETF (OIH): ETF Analysis Experiences

ProFrac Holding Corp. (ACDC) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.