The Zacks Automotive – Unique Gear business is benefiting from rising automation adoption, which is enhancing manufacturing effectivity, productiveness, high quality and security whereas decreasing labor prices for producers. Nonetheless, weakening automobile demand, geopolitical tensions and rising oil costs are pressuring automobile manufacturing and automotive tools demand. The anticipated decline in North America automobile manufacturing in 2026 and 2027 displays these challenges. Regardless of the business’s weak near-term outlook and underperformance relative to the broader market, firms corresponding to Garrett Movement Inc. GTX, PHINIA Inc. PHIN and LCI Industries LCIIremain well-positioned as a consequence of innovation, diversified operations and increasing aftermarket companies.

Trade Description

The Zacks Automotive – Unique Gear Trade includes firms that design, produce and supply passive security programs for the automotive sector. These programs goal to enhance security, increase effectivity, scale back general possession prices and streamline fleet administration, supporting people who sort out a few of the hardest jobs globally. Corporations that design, engineer and manufacture Driveline and Metallic Forming applied sciences to assist electrical, hybrid and inside combustion automobiles are additionally a part of the identical business. The business provides tools to the U.S. authorities and massive automotive producers. Some firms additionally interact in tools financing and leasing options for his or her prospects, primarily by means of third-party funding preparations.

Elements Shaping Trade’s Outlook

Automation to Improve Manufacturing Effectivity: Automation entails using superior applied sciences and equipment to carry out duties that had been historically carried out by people, serving to enhance effectivity, productiveness, high quality and security whereas lowering labor prices. This transformation has considerably reshaped manufacturing by enabling quicker and extra environment friendly manufacturing processes. For authentic tools producers, automation gives a aggressive benefit by decreasing working prices, mitigating rising labor bills and boosting general effectivity. It additionally permits producers to reply extra shortly to altering market circumstances, improve product high quality and assist the environment friendly manufacturing of electrical and next-generation automobiles, all of that are important for sustaining competitiveness within the international automotive business.

Weak Auto Manufacturing to Harm Demand: Demand for auto tools is carefully tied to automobile manufacturing ranges at automakers. When demand for brand new automobiles weakens, producers usually scale back manufacturing, which, in flip, lowers demand for automotive tools and parts. The near-term outlook for the worldwide auto business has turn into more and more unsure as a result of ongoing battle in Iran. The scenario has led to larger oil costs and elevated market volatility, elevating manufacturing and logistics prices throughout the business. These pressures are anticipated to weigh on automobile demand and manufacturing ranges. The S&P International has lowered its North America automobile manufacturing outlook by 63,000 models for 2026 and 235,000 models for 2027. The anticipated decline in automobile manufacturing is prone to scale back demand for automotive tools, creating further stress on the income progress of auto tools producers.

Margin Stress Intensifies: Unique tools producers’ profitability is coming beneath stress as a consequence of growing pricing competitors and continued excessive financing and uncooked materials prices, per Bain & Firm. On the similar time, uncertainty surrounding the pace of electrical automobile adoption is including additional pressure, as automakers proceed to assist each EV and inside combustion engine product lineups concurrently.

Zacks Trade Rank Signifies Dim Close to-Time period Prospects

The Zacks Automotive – Unique Gear Trade is a part of the broader Zacks Autos/ Tires/ Vans sector. It carries a Zacks Trade Rank #183, which locations it within the backside 25% of greater than 250 Zacks industries.

The group’s Zacks Trade Rank, which is the typical of the Zacks Rank of all of the member shares, signifies dim near-term prospects. Our analysis reveals that the highest 50% of the Zacks-ranked industries outperform the underside 50% by an element of greater than two to 1.

The business’s place within the backside 50% of the Zacks-ranked industries is a results of a damaging earnings outlook for the constituent firms in combination. Wanting on the combination earnings estimate revisions, it seems that analysts are pessimistic about this group’s earnings progress potential.

Regardless of the damaging business outlook, we’ll current a couple of shares that you just may take into account including to your watchlist. Earlier than that, let’s talk about the business’s current inventory market efficiency and valuation image.

Trade Lags the S&P 500 & Sector

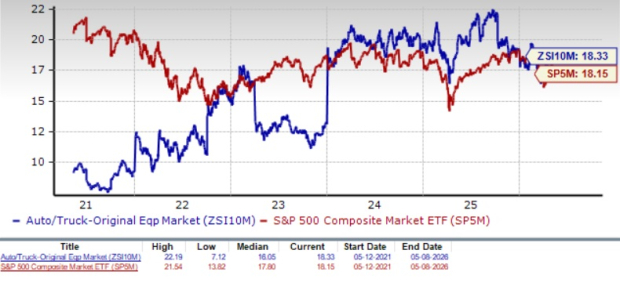

The Zacks Automotive – Unique Gear Trade has underperformed the S&P 500 and its sector over the previous yr. The business has declined 5% over this era towards the S&P 500’s progress of 31.9%. The broader sector has returned 25.7% in the identical timeframe.

One-12 months Worth Efficiency

Picture Supply: Zacks Funding Analysis

Trade’s Present Valuation

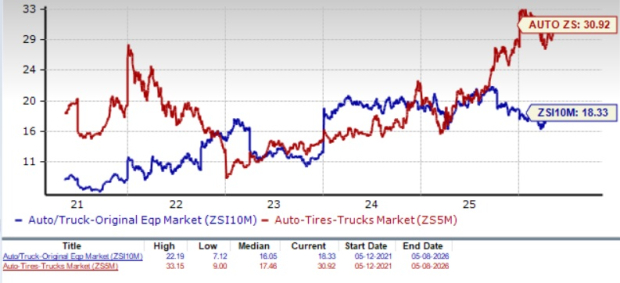

Since automotive firms are debt-laden, it is smart to worth them primarily based on the Enterprise Worth/ Earnings earlier than Curiosity Tax Depreciation and Amortization (EV/EBITDA) ratio.

Primarily based on the trailing 12-month enterprise worth to EBITDA (EV/EBITDA), the business is at the moment buying and selling at 18.33X in contrast with the S&P 500’s 18.15X and the sector’s 30.92X.

Over the previous 5 years, the business has traded as excessive as 22.19X and as little as 7.12X, with the median being 16.05X, because the chart beneath reveals.

EV/EBITDA Ratio (Previous 5 Years)

Picture Supply: Zacks Funding Analysis

Picture Supply: Zacks Funding Analysis

3 Shares to Take into account Proper Now

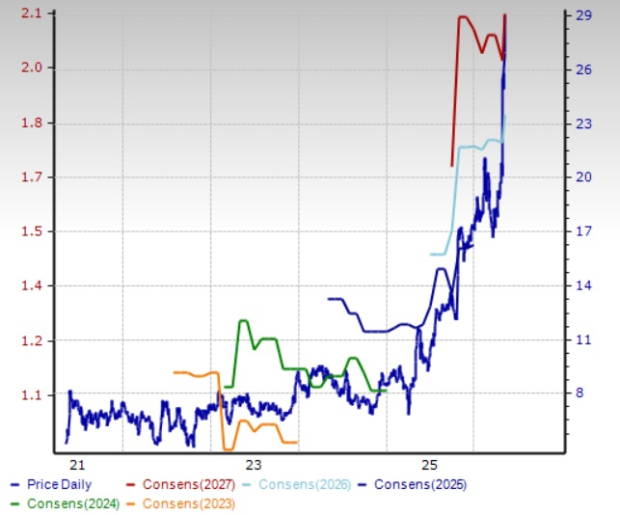

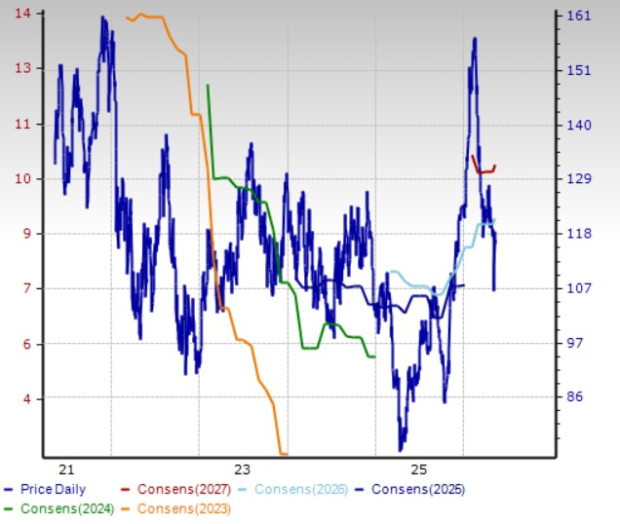

Garrett: It designs, manufactures and sells turbocharging, air and fluid compression, and high-speed electrical motor applied sciences for mobility and industrial functions. It continues to strengthen its management within the international turbocharger market, supported by a robust know-how portfolio and a constant observe file of profitable new program awards.

GTX at the moment carries a Zacks Rank #2 (Purchase) and has a Worth Rating of B. The Zacks Consensus Estimate for 2026 gross sales and EPS implies year-over-year progress of 5.7% and 20.4%, respectively. Garrett has surpassed estimates in every of the trailing 4 quarters, the typical earnings shock being 16.33%.

Worth & Consensus: GTX

Picture Supply: Zacks Funding Analysis

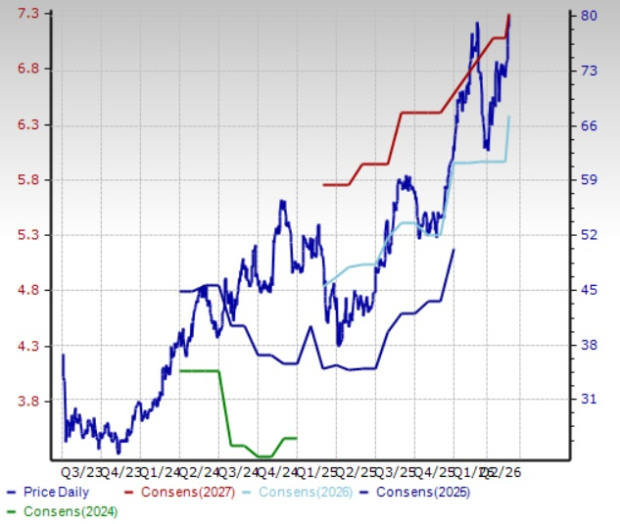

PHINIA: It’s a international chief within the improvement, design and manufacture of built-in parts and programs that improve efficiency, enhance gasoline effectivity and scale back emissions throughout combustion and hybrid propulsion platforms. It advantages from a well-diversified enterprise mannequin spanning geographies, finish markets and prospects, which helps scale back dependence on any single income stream.

PHIN at the moment carries a Zacks Rank #2 and has a Worth Rating of A. The Zacks Consensus Estimate for 2026 gross sales and EPS implies year-over-year progress of 6.6% and 28.2%, respectively. PHINIA has surpassed estimates in three of the trailing 4 quarters and missed as soon as, the typical earnings shock being 22.95%.

Worth & Consensus: PHIN

Picture Supply: Zacks Funding Analysis

LCI Industries: It’s a provider of parts to the leisure automobile and manufactured housing industries in addition to adjoining industries, together with bus, cargo and equestrian trailers, marine and heavy truck. The corporate expects progress in 2026 to be pushed by growing content material per unit by means of continued innovation, a robust emphasis on increasing its aftermarket enterprise that may serve almost each RV at the moment in operation and rising momentum throughout OEM markets. In October 2025, LCI acquired the entire enterprise property of Leveltron, a well known supplier of Bigfoot Hydraulic Methods. The corporate intends to broaden Bigfoot’s presence within the RV aftermarket by leveraging its intensive distribution and seller community to make the leveling programs extra extensively out there.

LCII at the moment carries a Zacks Rank #2 and has a Worth Rating of A. The Zacks Consensus Estimate for 2026 gross sales and EPS implies year-over-year progress of three.6% and 20%, respectively. LCI Industries has surpassed estimates in every of the trailing 4 quarters, the typical earnings shock being 22.06%.

Worth & Consensus: LCII

Picture Supply: Zacks Funding Analysis

Past Nvidia: AI’s Second Wave Is Right here

The AI revolution has already minted millionaires. However the shares everybody is aware of about aren’t prone to preserve delivering the largest income. AI’s second wave is transferring from infrastructure to implementation and these firms are on the forefront of this transition, positioned to turn into what Amazon and Google had been to the web period.

Garrett Movement Inc. (GTX) : Free Inventory Evaluation Report

LCI Industries (LCII) : Free Inventory Evaluation Report

PHINIA Inc. (PHIN) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.