The 2026 Q1 earnings season continues to chug alongside, with an enormous chunk of S&P 500 members already delivering their outcomes. Thus far, a number of firms – Alphabet GOOGL, Roku ROKU, and Interactive Brokers IBKR – have crushed it regarding key metrics, with every additionally seeing share momentum within the days which have adopted post-earnings.

Google Cloud Development Impresses

Alphabet posted a powerful double-beat relative to our consensus estimates, crushing our EPS estimate by greater than 90% and posting a 2.7% gross sales shock. Each objects noticed nice YoY development, with the inventory’s response post-earnings reflecting the strongest of the Magazine 7 bunch to this point.

Importantly, Google Cloud income totaled $20.0 billion, crushing our estimate and reflecting a rock-solid 62.7% YoY development fee. The expansion acceleration is exactly what the market needed to see, one other huge purpose why the inventory has soared post-earnings.

The EPS outlook stays bullish throughout the board for the Magazine 7 member, an enormous constructive regarding near-term momentum.

Picture Supply: Zacks Funding Analysis

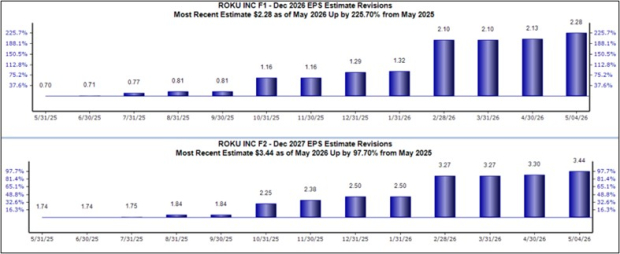

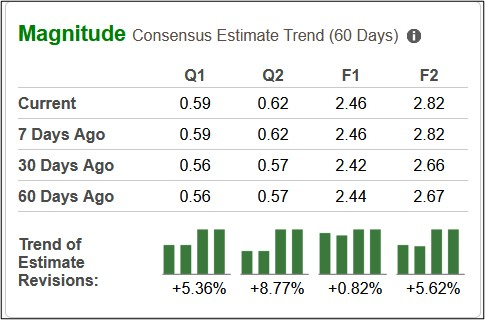

Roku Sees Huge Profitability Enchancment

Roku equally posted a double-beat relative to our consensus expectations, beating our EPS estimate by greater than 65% and posting a 3.8% gross sales shock. The profitability image strengthened considerably, with gross revenue climbing 27% YoY to $565 million.

The EPS outlook throughout its present and subsequent fiscal yr have moved bullishly, with upward revisions coming in following the discharge.

Picture Supply: Zacks Funding Analysis

Roku’s platform income grew 28% year-over-year, with robust Promoting and Subscription outcomes main the cost. Complete Streaming Hours additionally noticed a pleasant 8% YoY climb, with the corporate additionally now reporting greater than 100 million households worldwide use a tool powered by the Roku TV working system (OS) month-to-month.

Interactive Brokers Retains Executing

IBKR has been a powerful earnings performer over the previous a number of years, with shares benefiting in consequence. Fee income all through its reported interval elevated 19% YoY to a file $613 million, with buyer buying and selling quantity in shares, futures, and choices rising by 25%, 20%, and 16%, respectively.

The corporate’s choices proceed to draw a variety of latest clients, with buyer accounts rising by a rock-solid 31% YoY to roughly 4.8 million. The inventory noticed a weak response to the outcomes however shortly bounced again over current days. The EPS outlook for its present fiscal yr stays notably bullish, with the present $2.46 per share estimate up greater than 30% over the past yr.

IBKR’s EPS outlook stays bullish throughout the board.

Picture Supply: Zacks Funding Analysis

Backside Line

We’ve heard from a whole lot of S&P 500 members to this point within the 2026 Q1 earnings cycle, with a number of – Alphabet GOOGL, Interactive Brokers IBKR, and Roku ROKU – all posting strong outcomes throughout key metrics.

Zacks’ Analysis Chief Names “Inventory Most Prone to Double”

Our crew of specialists has simply launched the 5 shares with the best likelihood of gaining +100% or extra within the coming months. Of these 5, Director of Analysis Sheraz Mian highlights the one inventory set to climb highest.

This prime choose is a little-known satellite-based communications agency. Area is projected to change into a trillion greenback trade, and this firm’s buyer base is rising quick. Analysts have forecasted a significant income breakout in 2025. After all, all our elite picks aren’t winners however this one may far surpass earlier Zacks’ Shares Set to Double like Hims & Hers Well being, which shot up +209%.

Free: See Our High Inventory And 4 Runners Up

Interactive Brokers Group, Inc. (IBKR) : Free Inventory Evaluation Report

Alphabet Inc. (GOOGL) : Free Inventory Evaluation Report

Roku, Inc. (ROKU) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.