International markets closed final week on an unsure footing. Whereas bears appeared to have an higher hand, the management was by no means firmly gripped. Conviction was comparatively skinny as merchants had been reluctant to commit decisively. The general impression was of markets nonetheless trying to find a coherent theme to latch onto. Equities in main facilities mirrored the unease, struggling to carry early positive aspects and in the end turning decrease as worries over stretched AI valuations resurfaced. Treasury yields pushed greater, solely to reverse on Friday.

A part of the hesitation stems from the contradictory nature of final week’s info. The FOMC minutes had been hawkish. The delayed September NFP report confirmed strong hiring. However then New York Fed President John Williams unexpectedly opened the door to a different “near-term adjustment,” forcing merchants to reprice December odds but once more. Markets had been left with no clear coverage narrative, and worth motion mirrored that lack of anchor.

Within the foreign money markets, Greenback ended the week broadly greater however not forcefully so. Canadian Greenback was the second greatest, whereas Sterling adopted. Swiss Franc was the worst performer as merchants unwound the positive aspects following the US-Switzerland commerce deal. Aussie was the second worst regardless of hawkish as dragged down by weaker risk-sentiment. Yen was pressured nearly all of the weak on BoJ expectations, however ended simply on the third backside because of a late rebound. Euro and Kiwi led to center floor.

Fed December Name Turns Right into a Excessive-Stakes Guesswork Train

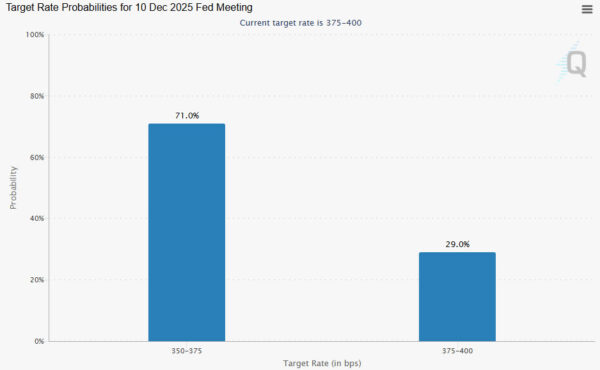

If there was one theme dominating markets this week, it was the extraordinary uncertainty surrounding the Fed’s December assembly. Usually, by this stage of the cycle, merchants would have a transparent sense of whether or not policymakers had been leaning towards easing or holding. As an alternative, expectations noticed their sharpest whiplash in months.

The discharge of the FOMC minutes was the primary main shock. The doc revealed that “many members” believed it will be acceptable to carry charges regular for the rest of the yr, a stronger pushback than markets had anticipated. Mixed with strong September job positive aspects, this led futures merchants to slash the chances of a December minimize to round 35%, the bottom in weeks.

However the image modified abruptly when New York Fed President John Williams—some of the influential voices on the Committee—argued there was nonetheless room for a “near-term adjustment” to convey coverage nearer to impartial. As a result of he’s a everlasting voter, and never often called a political actor, his remarks carried vital weight. Markets quickly repriced, with December minimize odds surging again above 70%.

However this surge in confidence is barely a part of the story, as a result of the Fed now lacks the info required to make an knowledgeable judgment. The delayed CPI and employment stories imply policymakers will enter the December 9–10 assembly with out realizing how inflation behaved in November or how the labor market advanced. Their new forecasts should due to this fact depend on incomplete info—an nearly unprecedented state of affairs for a choice of this magnitude.

This leaves policymakers in an unusually uncomfortable place. They need to resolve whether or not to take out one other “insurance coverage” minimize at nighttime or wait till they’ve fuller info. Consequently, December’s assembly is shaping as much as be some of the unpredictable in latest reminiscence. The Committee might moderately justify both motion, and market pricing could proceed to swing sharply with each speech or secondary indicator. Till higher knowledge arrives in mid-December, uncertainty will stay the defining function of Fed expectations.

AI Reversal Bruises Sentiment

The sharp swings in Fed expectations spilled instantly into fairness markets, the place sentiment deteriorated noticeably. Optimism following Nvidia’s blockbuster earnings lasted solely a matter of hours earlier than the market staged its largest intraday reversal since April. Buyers appeared desirous to fade rallies slightly than chase them.

This hesitation has been compounded by the shifting interest-rate backdrop. Whereas John Williams’ feedback gave equities a quick reprieve, the speed outlook didn’t change. Even when the Fed does minimize in December—the bar for additional easing is turning into considerably greater. Two consecutive charge reductions earlier within the yr don’t assure an open-ended cycle,That prospect alone threatens the liquidity tailwind that has supported high-growth tech names. and policymakers have signaled a want to proceed extra cautiously from right here.

Technical situations additionally argue for warning. DOW has damaged beneath its 55 D EMA, with bearish divergence on D MACD elevating the chance {that a} medium-term prime has already shaped at 48,431.57 earlier within the month. Within the much less bearish case, fall from 48,431.57 is merely correcting the rise from 36,611.78. However nonetheless, break of 45,452.03 assist would convey deeper fall to 38.2% retracement of 36,611.78 to 48,431.57 at 43,916.41.

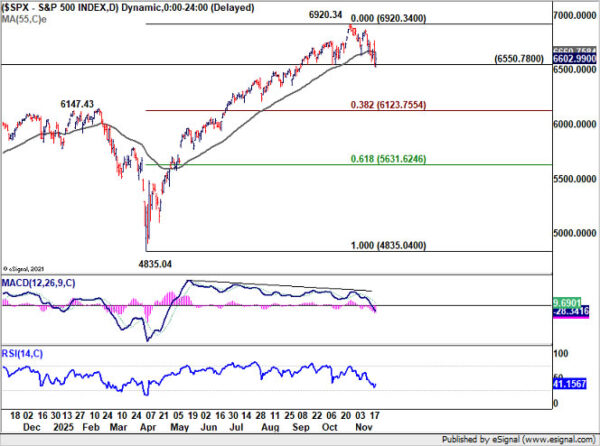

Comparable indicators are current throughout the S&P 500 and NASDAQ. A medium time period prime may very well be shaped at 6,290.34 in S&P 500, with the shut beneath 55 D EMA and bearish divergence situation in D MACD. Decisive break of 6,550.78 assist will convey deeper fall to 38.2% retracement of 4,835.04 to six,920.34 at 6,123.75.

For NASDAQ, the autumn from 24,019.99 is seen as a correction to the up development from 14,784.03. Agency break of 22,193.07 assist will pave the way in which to 38.2% retracement of 14,784.03 to 24,019.99 at 20,491.85.

Europe Turns Decrease Whereas Nikkei is an Outlier

European fairness markets endured a tough week too. Main benchmarks — together with FTSE, DAX, and CAC — traded sharply decrease

Germany’s DAX stands out as probably the most structurally susceptible. The index broke decisively beneath 23,284 assist following a bearish gap-down earlier within the week, signaling {that a} medium-term prime has possible shaped at 24,771.34. The minimal goal for corretion needs to be 38.2% retracement of 18,489.91 to 24,771.34 at 23,371.83n. It might properly prolong to 61.8% retracement at 20,889.42 earlier than discovering a backside.

FTSE’s image is marginally higher, although nonetheless threatened. The index is clinging to its 55D EMA (now at 9,506.54), with the market awaiting readability from subsequent week’s Autumn Funds. Any signal of tax will increase or lowered fiscal assist might add vital draw back strain. One other selloff will align the outlook with the US markets, and means that FTSE is already in correction to the rise from 7,544.83. That may convey deeper fall to 38.2% retracement of seven,544.83 to 9,930.09 at 9,018.92.

Throughout Asia, sentiment was equally fragile. Japan’s Nikkei gyrated decrease in sympathy with world declines, however continues to show relative resilience. Sentiment was supported by expectations that the BoJ will keep away from tightening in December and probably even in January. Optimism over Japan’s JPY 17.7T stimulus package deal has additionally helped cushion draw back dangers, alongside Prime Minister Sanae Takaichi’s exceptionally sturdy approval rankings, which have restored a level of political stability.

Nonetheless, Nikkei just isn’t resistant to world danger dynamics. The AI-led reversal in U.S. tech shares has begun to cap upside momentum, and sustained break beneath its 55 Day EMA (now at 47,729.68) would sign that Japanese equities are additionally getting into a deeper correction part. Till then, the uptrend from 30,792.74 technically stays intact.

Greenback Index’s Bounce from 96.21 Nonetheless in Power Regardless of Weak Momentum

Greenback Index’s rebound from 96.21 prolonged greater final week regardless that momentum is missing. Outlook is unchanged that rise from 96.21 is considered as a correction to the decline from 110.17 solely. Therefore, whereas additional rise may very well be seen, sturdy resistance ought to emerge from 38.2% retracement of 110.17 to 96.21 at 101.54 to restrict upside. Break of 98.99 assist will argue that the corrective bounce has already accomplished.

Nonetheless, the long run image needs to be emphasised once more. Greenback index has simply bounced off from a multi-decade channel flooring that outlined the up development since 2008. Agency break of 101.54 might push Greenback Index by way of 55 M EMA (now at 101.85). That may elevate the prospect that entire down development from 114.77 (2022 excessive) has accomplished as a 3 wave correction to 96.21. A sustained, prolonged medium time period rally would then comply with. This isn’t the bottom case for now, nevertheless it’s believable, particularly if danger aversion intensifies.

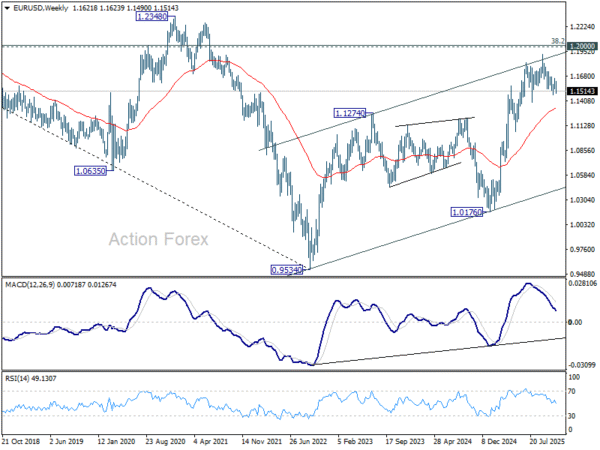

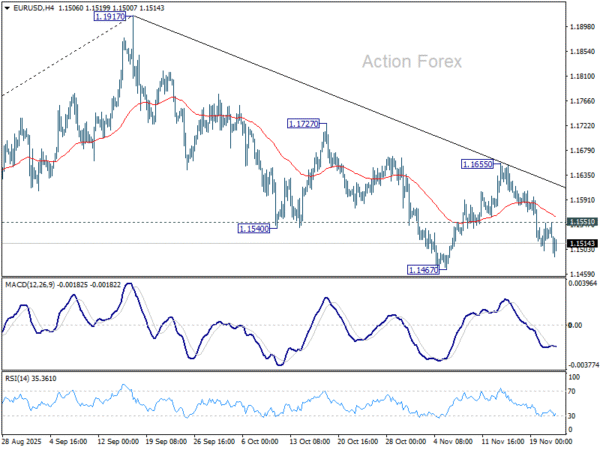

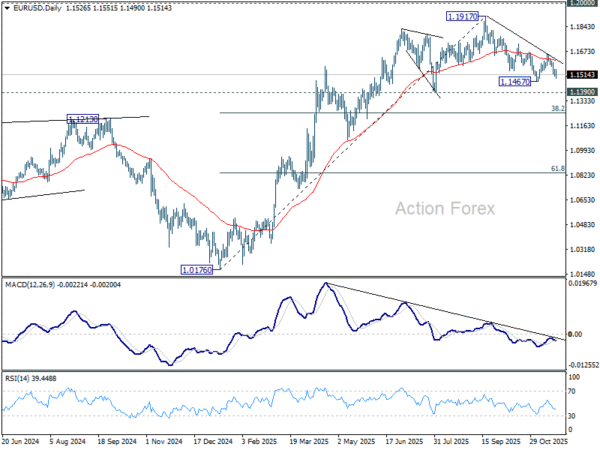

EUR/USD Weekly Outlook

EUR/USD’s prolonged decline final week means that rebound from 1.1467 has accomplished at 1.1655. Extra importantly fall from 1.1917 excessive just isn’t full. Preliminary bias stays on the draw back this week for 1.1467 first. Agency break there’ll goal 1.1390, after which 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, above 1.1551 minor resistance will flip intraday bias impartial. However danger will keep on the draw back so long as 1.1655 resistance holds, in case of restoration.

Within the greater image, contemplating bearish divergence situation in D MACD, a medium time period prime is probably going in place at 1.1917, simply forward of 1.2 key psychological degree. So long as 55 W EMA (now at 1.1328) holds, the up development from 0.9534 (2022 low) remains to be in favor to proceed. Decisive break of 1.2000 will carry bigger bullish implications. Nonetheless, sustained buying and selling beneath 55 W EMA will argue that rise from 0.9534 has accomplished as a 3 wave corrective bounce, and hold long run outlook bearish.

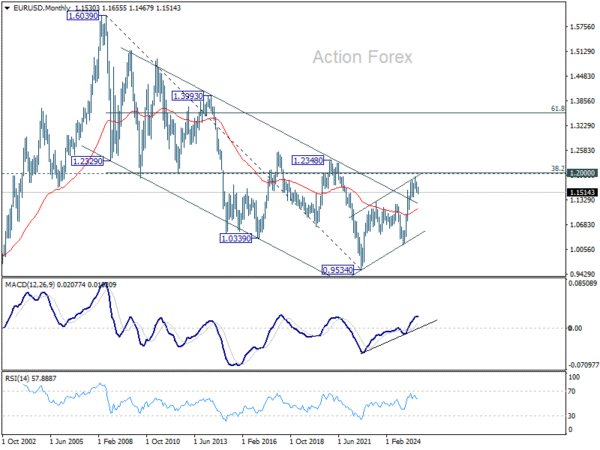

In the long run image, 38.2% retracement of 1.6039 to 0.9534 at 1.2019, which is near 1.2000 psychological degree is the important thing for the outlook. Rejection by this degree will hold the multi decade down development from 1.6039 (2008 excessive) intact, and hold outlook impartial at greatest. Nonetheless, decisive break of 1.2000/19, will recommend long run bullish development reversal, and goal 61.8% retracement at 1.3554.