")

POOLCORP POOL is seeing a slowdown in pool demand this summer time. This Zacks Rank #5 (Sturdy Promote) lately lowered full 12 months steerage.

POOLCORP is the world’s largest wholesale distributor of swimming pool and associated outside dwelling merchandise. It operates about 440 gross sales facilities in North America, Europe and Australia from the place it distributes greater than 200,000 merchandise to 125,000 wholesale clients.

POOLCORP Warns on the Full 12 months

On June 24, 2024, POOLCORP warned on the complete 12 months as discretionary pool spending has slowed. The corporate believed that new building pool exercise might be down 15% to twenty% for the 12 months with transform exercise down as a lot as 15%.

For the year-to-date interval, POOLCORP’s gross sales have been trending down roughly 6.5% from the identical interval in 2023. Whereas swimming swimming pools and outside dwelling initiatives are anticipated to say no, it was inspired as maintenance-related product gross sales remained secure.

There’s been quantity progress in chemical substances, and gear gross sales, excluding cleaners, have been down solely 2% for the 12 months. That was an enchancment from the three% decline within the first quarter of the 12 months.

Full 12 months Steerage Slashed

Given the pool slowdown, it isn’t a shock that POOLCORP lower its full 12 months steerage. It lowered the vary to $11.04 to $11.44 from $13.19 to $14.19.

The analysts adopted by chopping their earnings estimates. 5 estimates have been lower after the corporate warned.

It has pushed the Zacks Consensus Estimate right down to $11.10 from $13.21. That is on the low finish of the corporate’s steerage vary.

That is an earnings decline of 16.9% from 2023 as the corporate made $13.35 final 12 months.

Here is what it seems to be like on the value and consensus chart.

Picture Supply: Zacks Funding Analysis

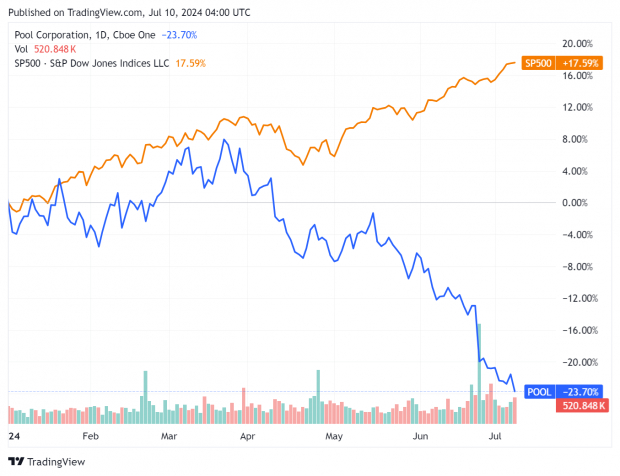

Shares Fall to New 52-Week Lows

Not shocking, the shares fell on the steerage warning and are actually down 23.7% year-to-date.

Picture Supply: Zacks Funding Analysis

However with the earnings being lower, the shares aren’t that low cost. It is buying and selling at 27x ahead earnings.

POOLCORP additionally pays a dividend, at present yielding 1.6%.

POOLCORP will probably be reporting second quarter outcomes on July 25, 2024 so the corporate will give extra coloration then.

However till the pool slowdown hits a backside, traders would possibly wish to keep on the sidelines. Watch the earnings estimates for indicators of a turnaround.

Zacks Names “Single Finest Choose to Double”

From 1000’s of shares, 5 Zacks specialists every have chosen their favourite to skyrocket +100% or extra in months to come back. From these 5, Director of Analysis Sheraz Mian hand-picks one to have essentially the most explosive upside of all.

It’s a little-known chemical firm that’s up 65% over final 12 months, but nonetheless filth low cost. With unrelenting demand, hovering 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail traders might soar in at any time.

This firm might rival or surpass different current Zacks’ Shares Set to Double like Boston Beer Firm which shot up +143.0% in little greater than 9 months and NVIDIA which boomed +175.9% in a single 12 months.

Free: See Our High Inventory and 4 Runners Up >>

Pool Company (POOL) : Free Inventory Evaluation Report

To learn this text on Zacks.com click on right here.

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.