")

Software program shares Intuit and Salesforce tanked to begin 2026 based mostly on fears that synthetic intelligence is crushing SaaS and all the software program {industry}.

AI is, certainly, shaking up the SaaS area, forcing Salesforce, Intuit, and numerous others to shortly adapt and develop their AI efforts.

Salesforce and Intuit are software program powerhouses that won’t go down and not using a combat. Their most up-to-date steerage and present gross sales and earnings estimates showcase resilience and spectacular development, indicating AI fears are overblown. The software program giants are additionally efficiently rolling out AI all through a lot of their choices.

INTU and CRM are two of the worst-performing S&P 500 shares in 2026, down 35% and 27%, respectively. Their latest downturns are a part of bigger selloffs which have Intuit and Salesforce buying and selling roughly 45% under their all-time highs.

This backdrop signifies that each large-cap tech shares provide practically 90% upside in the event that they ever make it again to their earlier peaks.

The selloff, blended with their robust earnings development outlooks, has additionally turned Intuit and Salesforce into potential worth shares proper now.

CRM and INTU have discovered some assist lately as Wall Avenue slowly dips its toes again into the software program area. Now may be a good time to contemplate shopping for Salesforce and Intuit as they combat to thrive within the AI age.

Purchase Software program Shares Now for Worth, Development, and AI Upside

Software program shares offered off sharply in early 2026 attributable to mounting investor fears that advancing AI applied sciences may disrupt conventional software program enterprise fashions.

Speedy enhancements in massive language fashions and agentic AI instruments have raised considerations that firms may construct customized in-house options or change costly SaaS subscriptions with AI-driven options.

However there are zero ensures that OpenAI, Anthropic, and others might be long-term winners given how shortly the expertise is altering. Extra importantly, Intuit and Salesforce have each spent the previous few years ramping up their very own AI efforts into practically each pocket of their portfolios.

Purchase INTU Inventory Now and Maintain Ceaselessly?

Intuit Inc. INTU inventory outpaced Microsoft over the previous 20 years as a result of its important tax-heavy software program allowed it to constantly generate spectacular double-digit income development. INTU has expanded its software program portfolio far past TurboTax to turn out to be a one-stop store for enterprise and client finance, electronic mail advertising, and extra through Credit score Karma, QuickBooks, and Mailchimp.

Intuit in 2024 started revamping its enterprise to shortly incorporate AI wherever it may to verify it was prepared to keep up its standing as essential hub for taxes, enterprise software program, and extra. It grew its FY25 income by 16%, matching its 16% common income growth over the previous 10 years.

Picture Supply: Zacks Funding Analysis

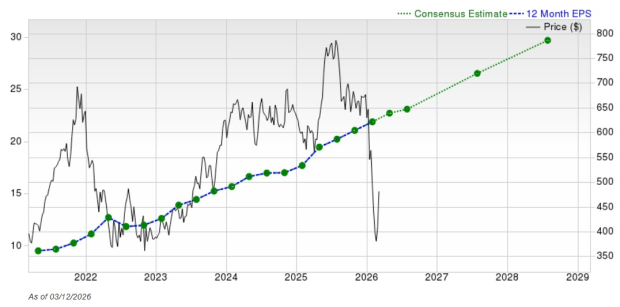

Most lately, it expanded its Q2 FY26 income by 17%, because it “defines” a brand new class on the “intersection of AI and human intelligence, one which delivers autonomous, done-for-you experiences.” Intuit is projected to develop its gross sales by roughly 12.5% in 2026 and 2027 to achieve $23.80 billion.

The tech agency helps its roughly 100 million international clients expertise new AI-boosted choices to nice success. INTU expanded its GAAP earnings by 31% in FY25, with its adjusted earnings 19% increased. The agency then elevated its GAAP earnings by 49% in Q2 FY26 and its adjusted earnings by 25%.

Picture Supply: Zacks Funding Analysis

INTU’s upward EPS revisions land the inventory a Zacks Rank #2 (Purchase) proper now, with it projected to develop its adjusted EPS by one other 15% in FY26 and FY27. The chart above highlights its long-term earnings growth outlook, which showcases its capability to efficiently develop amid AI disruption fears.

The inventory has climbed 1,530% previously 20 years to crush Tech’s 820% and outclimb Microsoft’s 1,350%. This run contains Intuit’s ~45% tumble from its summer time 2025 peaks. Its common Zacks value goal gives 43% upside from its present ranges, and it must climb practically 90% (~87%) to return to its all-time highs.

Picture Supply: Zacks Funding Analysis

Intuit shares have discovered assist at its post-Covid breakout lows because it continues to commerce at its most oversold RSI ranges of the previous 20 years.

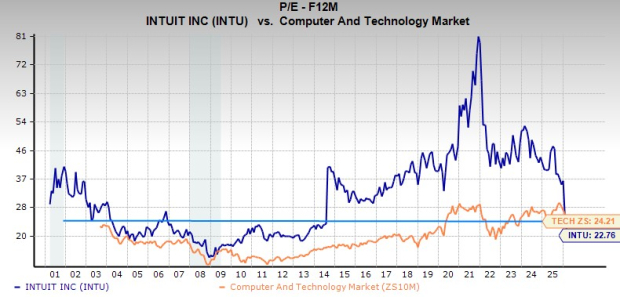

On the valuation entrance, INTU is buying and selling at its lowest ahead P/E since Wall Avenue started placing an enormous premium on its SaaS choices. It’s buying and selling at a reduction to Tech’s 24.2X and 72% under its all-time highs at 22.8X ahead earnings.

Ought to Merchants and Lengthy-Time period Traders Purchase CRM Inventory Now?

Salesforce CRM was on the vanguard of enterprise software program, buyer relationship administration, and full Saas {industry}. CRM’s rising portfolio helps gross sales, advertising, buyer and consumer engagement, analytics, app improvement, and rather more.

The corporate began to focus closely on earnings growth when the Fed first started lifting charges off their Covid lows as a part of an industry-wide transition towards worthwhile development.

Picture Supply: Zacks Funding Analysis

Salesforce can also be shopping for again a ton of inventory to reward shareholders, and it began paying dividends in 2024, becoming a member of the likes of Meta and Alphabet.

Most significantly, its successfully introduction AI throughout its portfolio. Salesforce launched its Agentforce AI software again in 2024, frequently adapting to the agentic AI area since then.

Agentforce reached $800 million in annual recurring income in fiscal 2026 (interval ended January 31), up 169% YoY. “We’ve rebuilt Salesforce to turn out to be the working system for the Agentic Enterprise, bringing people and brokers collectively on one trusted platform,” CEO Marc Benioff mentioned in ready This fall remarks in late February.

The enterprise software program energy grew its income by 10% final yr as a part of 10% common gross sales development within the trailing three years. The corporate is projected to develop its income by 11% this yr and over 9% subsequent yr to $50.32 billion.

Salesforce provided robust steerage for its FY27. It additionally mentioned CRM is effectively on its strategy to $63 billion in income by FY30, because it rides Agentic AI as an enormous tailwind.

Picture Supply: Zacks Funding Analysis

CRM expanded its adjusted and its GAAP earnings by ~23% final yr. Its earnings estimates have improved since its This fall launch with it projected to develop its adjusted EPS by 5% in FY27 and 12% in FY28. Salesforce is then anticipated to ramp up its bottom-line development by an much more spectacular clip.

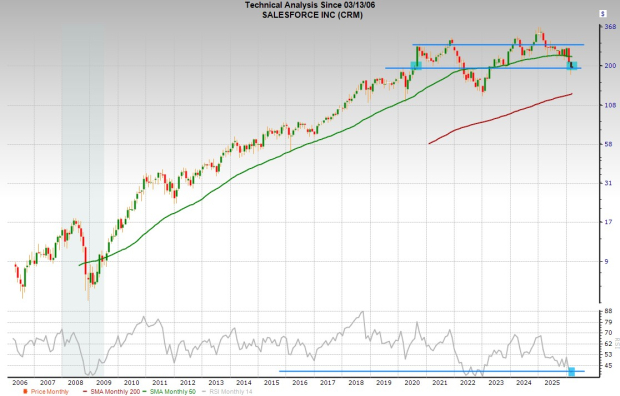

CRM shares have climbed ~2,000% previously twenty years to greater than double Tech’s 820%. But, the inventory is down 9% previously 5 years due, largely, to its 47% drop from its December 2024 peaks.

Salesforce’s common Zacks value goal marks 40% upside from its present ranges. Plus, the inventory must climb round 88% to return to its peaks.

Picture Supply: Zacks Funding Analysis

Salesforce is holding its floor close to its pre-2020 breakout highs because it trades at its most oversold RSI ranges since 2022 and 2008.

Its selloff, blended with its robust earnings outlook, has CRM buying and selling at a lowest-ever ahead P/E at 20.3X. This additionally marks 90% worth vs. its five-year highs and a stable low cost to the Tech sector.

Zacks’ Analysis Chief Picks Inventory Most Prone to “At Least Double”

Our specialists have revealed their High 5 suggestions with money-doubling potential – and Director of Analysis Sheraz Mian believes one is superior to the others. In fact, all our picks aren’t winners however this one may far surpass earlier suggestions like Hims & Hers Well being, which shot up +209%.

See Our High Inventory to Double (Plus 4 Runners Up) >>

Salesforce, Inc. (CRM) : Free Inventory Evaluation Report

Intuit Inc. (INTU) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.