")

Between spring and summer season of final 12 months, Oracle (ORCL) inventory almost tripled as maverick founder and CEO Larry Ellison laid all the things on the road to hitch the AI race. The inventory surged from beneath $130 to $346 on a wave of Stargate bulletins, hyperscaler partnerships, and Ellison’s unmistakable conviction that this was the second to go all-in. But within the months since final fall shares have collapsed greater than 50%.

Was this only a flash within the pan, an ageing tech large’s last-ditch effort to experience the AI wave earlier than it crested? Or is the market misunderstanding Oracle’s genuinely advantaged place in an important infrastructure buildout of a era? I imagine it’s the latter. And if that’s right, Oracle could also be probably the greatest uneven alternatives within the fairness market at this time.

Picture Supply: TradingView

A Robust Earnings Report Provides ORCL Inventory a Increase

Earlier this week, Oracle reported fiscal Q3 2026 outcomes that have been, by any measure, distinctive. Complete income rose 22% year-over-year to $17.2 billion, with cloud income surging 44% to $8.9 billion. Cloud infrastructure income, the section most straight tied to the AI buildout, grew 84% to $4.9 billion, accelerating from the 68% progress posted the prior quarter. Non-GAAP EPS got here in at $1.79, up 21%, beating consensus estimates. Administration famous this was the primary quarter in over fifteen years the place each natural whole income and non-GAAP EPS every grew 20% or extra.

Maybe probably the most staggering determine was remaining efficiency obligations (RPO), primarily contracted however not but acknowledged income, exploded to $553 billion, up 325% from a 12 months in the past and $29 billion sequentially. It is a backlog that dwarfs the corporate’s $67 billion in anticipated FY2026 income by an element of greater than eight. Administration additionally raised FY2027 income steerage to $90 billion, implying roughly 34% progress, tempo that may have been unthinkable for Oracle even two years in the past.

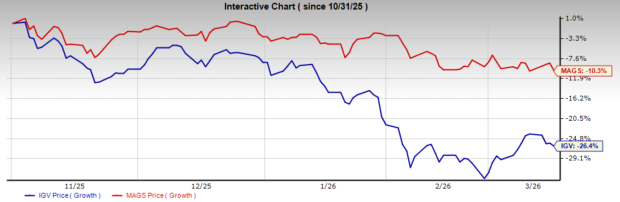

Main AI Shares Have Obtained No Love for Months

In latest months, traders have broadly punished the businesses pouring tens of billions into AI infrastructure. The Magnificent Seven shares have confronted headwinds from AI capex skepticism, and Oracle has been crushed down even worse.

However the comparability to the Magnificent Seven obscures a crucial distinction. Firms like Amazon (AMZN), Microsoft (MSFT), and Meta Platforms (META) have considerably delicately managed their AI spending to guard margins and quarterly earnings trajectories. They’re investing, however they’re doing so in a manner that retains Wall Road a bit extra snug, as capex is rising, however profitability is being maintained.

Oracle has taken the other method. Below Ellison’s course, the corporate has been unconcerned with deftness, pouring capital into knowledge heart buildouts at a tempo that exceeds its personal working money circulate. Within the first 9 months of FY2026, Oracle spent $39.2 billion in capex towards $17.4 billion in working money circulate. On a trailing four-quarter foundation, free money circulate has plunged to damaging $24.7 billion. The corporate raised $30 billion in debt and fairness financing in February alone, and whole debt now exceeds $134 billion.

Wall Road hates this damaging free money circulate, rising leverage and margin compression because it seems reckless. However context issues enormously right here. Ellison is executing what could also be a calculated land seize, investing in bodily AI infrastructure with the conviction that first-mover scale will generate sturdy aggressive benefits and probably extraordinary future money flows. That is the form of transfer that appears horrible on a trailing foundation and doubtlessly sensible on a ahead one.

Ellison additionally has a particular benefit (or drawback relying on the way you suppose). At 40% of shares excellent, he has probably the most pores and skin within the recreation in comparison with the opposite tech founders. Meta Platforms proprietor Zuckerberg holds 15%, Musk owns lower than 20% of Tesla and Bezos is down to simply 8% of Amazon. Ellison has been taking massive and contrarian bets for nearly 50 years together with his firm, so his massive strikes aren’t unprecedented. He has expertise on this recreation of epically excessive stakes.

Oracle Inventory Caught in A number of Weak Themes

A part of why Oracle inventory has been dragged down up to now is its publicity to 2 key themes which have suffered vital drawdowns in latest months. As we famous, former leaders within the AI infrastructure commerce have been hit exhausting as traders query the returns on huge capital spending applications. Extra lately, software program shares have additionally come beneath extreme stress as worries about AI disruption shook investor confidence throughout the sector. That mentioned, Oracle’s rising debt load, speculative investments in AI infrastructure, and infrequently doubtful enterprise partnerships have not helped both.

The selloff in these themes seems to have reached the purpose of being indiscriminate, nevertheless, and in software program particularly, the promoting seems to be like it might be nearing exhaustion. Choose names within the sector, in addition to Magnificent Seven leaders like Amazon and Meta Platforms, are buying and selling at a few of their most interesting ranges in years.

Amongst large-cap, AI-adjacent shares, Oracle stands out as one of the crucial enticing at present ranges. At roughly 21x ahead earnings, with long-term EPS progress above 19%, gross sales projected to develop almost 17% this 12 months and 32% subsequent 12 months, and $553 billion in contracted future income, the elemental setup is compelling to say the least.

Picture Supply: Zacks Funding Analysis

Ought to Traders Purchase Shares in ORCL?

The chance is just not with out threat. The standard of that half-trillion-dollar backlog of contracted future income stays to be seen, the appreciable debt taken on provides a level of uncertainty, and naturally, the large projections for AI business progress are nonetheless very a lot up within the air, although all accessible knowledge continues to level to demand outstripping capability.

That mentioned, Oracle at present ranges presents a uncommon mixture: an organization rising income north of 20%, an infrastructure enterprise scaling at hyper-growth charges, a half-trillion-dollar contracted backlog, and a controlling shareholder with extra pores and skin within the recreation than arguably anybody out there, all buying and selling at a reduction to the software program sector it is being lumped in with. The market is pricing Oracle as a software program firm being disrupted by AI however it’s truly the corporate constructing the infrastructure for it. That disconnect may very well be the chance.

Simply Launched: Zacks Prime 10 Shares for 2026

Hurry – you may nonetheless get in early on our 10 prime tickers for 2026. Handpicked by Zacks Director of Analysis Sheraz Mian, this portfolio has been stunningly and persistently profitable.

From inception in 2012 by way of November, 2025, the Zacks Prime 10 Shares gained +2,530.8%, greater than QUADRUPLING the S&P 500’s +570.3%.

Sheraz has combed by way of 4,400 firms coated by the Zacks Rank and handpicked the most effective 10 to purchase and maintain in 2026. You possibly can nonetheless be among the many first to see these just-released shares with monumental potential.

Amazon.com, Inc. (AMZN) : Free Inventory Evaluation Report

Microsoft Company (MSFT) : Free Inventory Evaluation Report

Oracle Company (ORCL) : Free Inventory Evaluation Report

Meta Platforms, Inc. (META) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.