")

Prologis, Inc. (PLD) presently sits in our impartial vary for valuation. I feel that’s truthful. Listed below are a number of components to think about:

-

Shares (at $132.05 intraday) commerce at 27.63x ahead AFFO consensus estimates of $4.80. That is on the excessive finish for REITs presently.

-

Shares are about 47.8% above their lowest shut over the past 52 weeks.

-

Shares are about 7% beneath their highest shut over the past 52 weeks (set in early March 2026).

-

Dividend yield is at 3% with about 4.9% steerage for development in Core FFO per share excluding web promote revenue this yr.

-

We need to pay sturdy consideration to the expansion. Nevertheless, we’re centered on long-term development charges whereas acknowledging that short-term development charges can have a big affect on the a number of.

-

Prologis has rallied all the way in which from our “Sturdy Purchase” vary to our “impartial” vary. We presently have a impartial rating on PLD. (For reference, our final article was right here).

Right here’s a chart exhibiting the historic worth and multiples:

TIKR

Utilizing the share worth or the ahead AFFO a number of, we noticed the valuation transfer up fairly a bit.

Prologis has delivered a powerful rally over the past yr, with shares climbing considerably in roughly the final 11 months. That efficiency has pushed the valuation increased and took our valuation from sturdy purchase to our impartial space. With the inventory already reflecting some optimism, it turns into vital to guage the most recent working outcomes and the outlook for continued development.

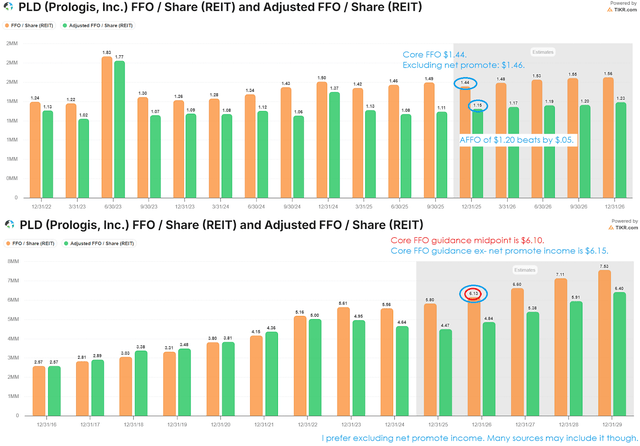

Prologis Core FFO And AFFO Outcomes And Steering

Prologis outcomes:

-

Core FFO of $1.44 matched estimates of $1.44. Excluding web promote revenue, $1.46 would beat estimates.

-

AFFO per share of $1.20 beat estimates of $1.15 by $.05.

Right here’s the large chart:

TIKR

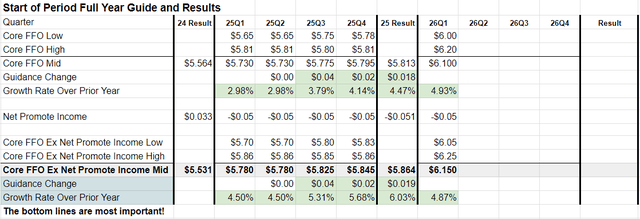

We additionally monitor the steerage for Core FFO Ex Internet Promote Revenue as a result of I discover that worth is extra helpful for reflecting the efficiency of the true property portfolio:

The REIT Discussion board

Observe: We may use the time period “Internet Promote Expense.” For simplicity, I checklist it as “revenue” even when now we have a detrimental worth. Over lengthy intervals the worth will normally be constructive.

Trying To 2026

-

Consensus estimate was $6.13.

-

Steering for Core FFO was $6.10 (decrease by $.03).

-

Steering for Core FFO Ex Internet Promote Revenue was $6.15 (increased by $.02).

That’s implying development continues at about 5%. Absent any detrimental shocks, we might even see PLD beat the unique steerage as they did final yr. For 2025 they ended up about 1.5% above the unique steerage.

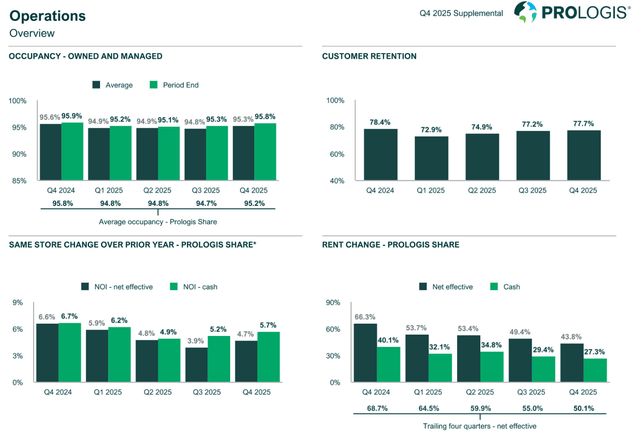

Steering for same-store web working revenue is vital additionally. It is likely one of the main components we take into account when evaluating long-term development charges and the attraction of the underlying actual property.

The REIT Discussion board

That’s barely quicker development in money NOI than PLD noticed in 2025.

Normal Notes

The main standards proceed to look good.

PLD

Common occupancy steerage has a midpoint of 95.25%, much like the most effective quarter for PLD in 2025. This matches commentary from a lot earlier (a number of quarters in the past) about when occupancy was anticipated to hit the low level and the rebound we’d more than likely see.

Hire change on renewals (leasing unfold) is coming down however remains to be fairly stable. If this development continues, it may stress same-store web working revenue. However we’re nonetheless seeing wholesome efficiency for PLD.

Curiosity Charges

Like many REITs with operations across the globe, PLD has utilized decrease rates of interest in Europe for a larger portion of their debt just lately. This mitigates a part of the stress from increased charges. Additionally they have a fairly lengthy weighted maturity on their money owed at 8.5 years. Nevertheless, long-duration (like 10-year Treasury) rates of interest are presently trending increased in the USA. That’s typically detrimental for valuation.

Over the past a number of days, we’ve additionally seen short-term charges leaping increased.

Knowledge Facilities

We might even see PLD placing about 40% of their new growth into knowledge facilities (based mostly on the PLD This fall 2025 earnings name).

I’ve talked about earlier than that knowledge facilities might be constructed at pretty excessive yields, which is sort of engaging. It creates a possible problem down the highway from extreme growth, but it surely makes them engaging growth tasks at this time. That is nonetheless a minor portion of PLD’s portfolio, however they’ve evaluated the land of their portfolio and located many circumstances the place they’ll optimize the worth by constructing knowledge facilities (as a substitute of commercial). This will also be used for attracting investor capital into the event funds Prologis manages. I like this technique of publicity to knowledge facilities way more than I would love proudly owning knowledge heart REITs. PLD remains to be an overwhelmingly industrial REIT with an amazing steadiness sheet and experience in growth.

My Expectations

I’m inclined to suppose PLD will barely outperform steerage as long as the economic system doesn’t go off the rails. That’s fairly good. They maintain the steadiness sheet sturdy and ship regular development over time. The efficiency of the underlying portfolio backs the expansion in AFFO per share. Nevertheless, valuation has been pushing fairly a bit increased. I’m not drawn to the present a number of.

With occupancy averaging about 95% over 2025, PLD has some room to develop there. Administration is nice at forecasting world growth and demand ranges. I count on them to be proper. Nevertheless, I discover the projections they supply sometimes are normally designed to be barely cautious, so they’re much less prone to have one thing “go unsuitable.” Administration requires world warehouse occupancy to extend barely over the yr, with lease development rising in direction of the top of the yr.

Conclusion

AFFO per share solidly beat estimates, however AFFO could be a bit unstable due to the timing for upkeep capex. On this case, I feel AFFO introduces extra volatility for PLD than it does for a few of the non-industrial REITs.

Steering was roughly on par with estimates, relying on how we modify for the detrimental $.05 associated to web promote revenue. I see that as a non-issue. So I don’t suppose something right here ought to land as a constructive or detrimental shock.

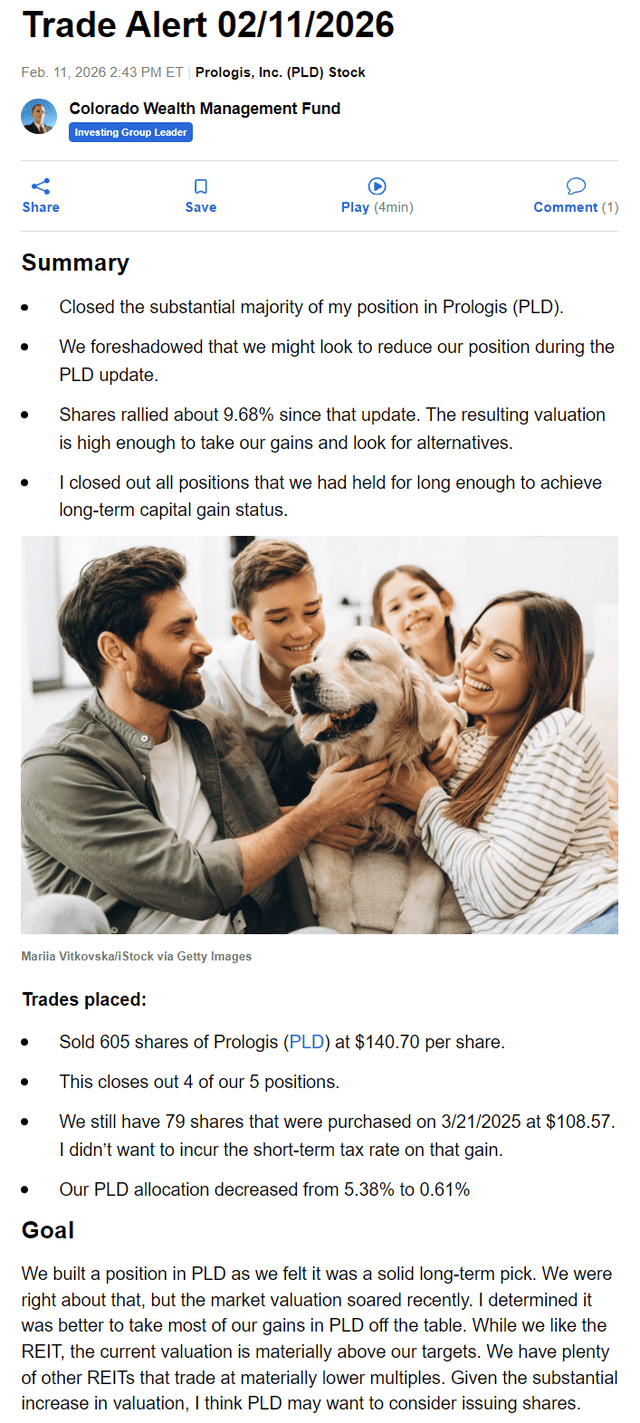

Current Commerce

I consider you will need to disclose buying and selling exercise and to supply proof for trades. If traders don’t monitor their positions, they’ll find yourself with some delusional concepts about their efficiency. We just lately closed out the overwhelming majority of our place in Prologis. The commerce was offered to subscribers with a real-time commerce alert:

Looking for Alpha

To reinforce transparency, I additionally consider you will need to embody screenshots exhibiting affirmation of a commerce. Some folks say there is no such thing as a cause to do this. I do it for 2 causes:

-

Many traders have instructed me that it’s simpler for them to be clear about my outlook once they can see the commerce.

-

It establishes a definitive assertion in regards to the precise execution. Typos occur. Miscommunication occurs. The screenshot prevents miscommunication. Both that commerce occurred precisely as proven, or the analyst faked the screenshot and must be held to account.

Due to this fact, right here is the screenshot:

Schwab

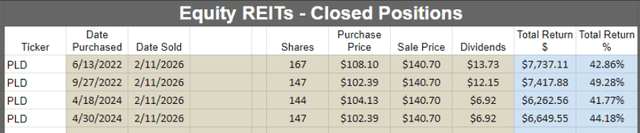

Listed below are the returns on the shares I bought:

The REIT Discussion board