The earnings focus stays on the retail area, with a number of bellwether operators on deck to report outcomes this week, together with Goal TGT, Finest Purchase BBY, Costco COST, Macy’s M, and others.

The earnings releases so far present a reassuring view of client spending, with broad spending developments largely secure and according to what we’ve been seeing in latest quarters. That mentioned, cumulative inflation stays a headwind, notably on the decrease finish of revenue distribution. The secure combination spending developments mirror power amongst high-income and youthful client teams, with the majority of the outlays going in the direction of necessities and experiences.

Demand for discretionary spending classes akin to big-ticket merchandise has remained tender within the post-COVID interval, although latest outcomes from Walmart WMT present some indicators of enchancment. Weak spot within the discretionary spending classes explains a giant a part of Goal’s underperformance relative to Walmart and others over the previous 12 months, although Goal shares are off to an awesome begin in 2026.

The chart under reveals the one-year efficiency of Goal (inexperienced line; down -8.7%), Finest Purchase (blue line; down -31.5%), Costco (purple line; down – 4.7%), Walmart (orange line; up +29.2%), and the S&P 500 index (pink line; up +18.8%).

Picture Supply: Zacks Funding Analysis

As famous earlier, Goal shares have performed exceptionally properly this 12 months, up +15.6% and outperforming Walmart’s 15% rise and the broader market’s +0.6% acquire.

Goal shares had been down following every of the final 5 quarterly releases. Nonetheless, the inventory’s latest momentum means that market contributors count on administration to offer a constructive outlook once they report earlier than the market’s open on Tuesday (March 3rd).

The expectation is for Goal to report $2.17 per share in earnings on $30.52 billion in revenues, representing year-over-year adjustments of -10% and -1.3%, respectively. Estimates had modestly inched up following the February 10th administration replace however have remained unchanged since then. Comps are anticipated to be down -2.48%, which might comply with the corporate’s disappointing exhibiting on this depend within the previous interval, when it reported a -2.7% comp decline vs. expectations of -1.89%.

Finest Purchase is anticipated to return out with EPS of $2.48 on $13.91 billion in revenues Tuesday morning, representing year-over-year adjustments of -3.9% and -0.3%, respectively. With respect to same-store gross sales, the expectation is a +0.14% acquire, following the +2.7% acquire within the final quarterly launch on November twenty fifth, relative to expectations of +1.57% comp progress.

Finest Purchase shares had been up following the November launch, because the Q3 comp progress had crushed expectations in a giant manner. The revisions development has been modestly detrimental, reflecting the comparatively tender vacation gross sales for the electronics class. There may be seemingly not an entire lot of draw back danger in Finest Purchase shares at this stage, however detrimental surprises on the comps entrance will seemingly put extra strain on the inventory.

With respect to the Retail sector’s 2025 This autumn earnings season scorecard, we now have outcomes from 22 of the 30 retailers within the S&P 500 index. Common readers know that Zacks has a devoted stand-alone financial sector for the retail area, which is not like the position of the area within the Client Staples and Client Discretionary sectors within the Customary & Poor’s normal trade classification. The Zacks Retail sector contains not solely Goal, Finest Purchase, and different conventional retailers, but additionally on-line distributors like Amazon AMZN and restaurant gamers.

Complete This autumn earnings for these 22 retailers which have reported are up +6.9% from the identical interval final 12 months on +8.6% greater revenues, with 50% beating EPS estimates and 77.3% beating income estimates.

The comparability charts under put the This autumn beats percentages for these retailers in a historic context.

Picture Supply: Zacks Funding Analysis

As you may see above, the proportion of those firms beating consensus EPS estimates is the bottom at 50% for this group of twenty-two retailers within the index over the previous 5-year interval. We must also notice that the sector’s 50% EPS beats proportion is the bottom, together with the Auto sector, of all 16 Zacks sectors this earnings season.

With respect to the elevated earnings progress charge at this stage, we like to point out the group’s efficiency with and with out Amazon, whose outcomes are among the many 22 firms which have already reported. As we all know, Amazon’s This autumn earnings had been up +5.9% on +13.6% greater revenues, because it missed EPS and income expectations.

The 2 comparability charts under present This autumn earnings and income progress relative to different latest intervals, with Amazon’s outcomes included (left aspect chart) and excluded (proper aspect chart).

Picture Supply: Zacks Funding Analysis

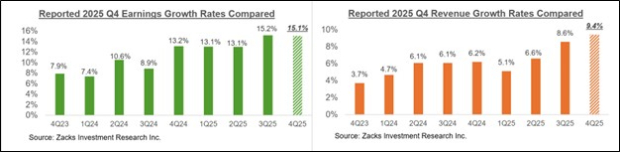

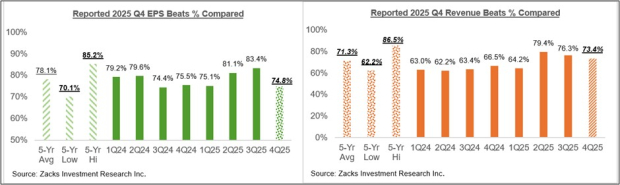

This autumn Earnings Season Scorecard

By means of Friday, February 27th, we’ve seen This autumn outcomes from 481 S&P 500 members, or 96.2% of the index’s complete membership. Complete earnings for these firms are up +15.1% from the identical interval final 12 months on +9.4% greater revenues, with 74.8% beating EPS estimates and 73.4% beating income estimates.

We’ve got greater than 300 firms on deck to report outcomes this week, together with 12 index members. The week’s line-up contains Broadcom, together with the aforementioned retailers.

The comparability charts under show the expansion charges for the businesses which have reported with what we had seen from this identical group of firms in different latest intervals.

Picture Supply: Zacks Funding Analysis

The comparability charts under present the This autumn EPS and income beats percentages for this group of firms relative to what we had seen from them in different latest intervals.

Picture Supply: Zacks Funding Analysis

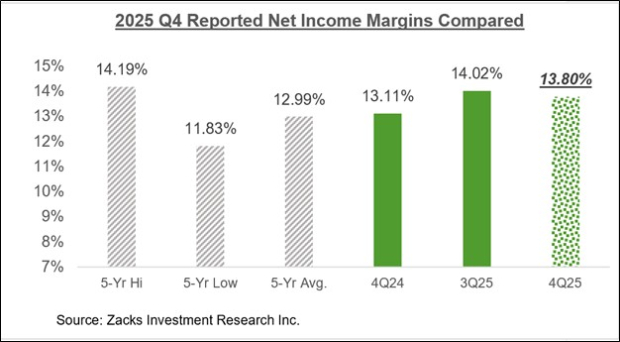

The comparability chart under reveals the This autumn web margins for the 481 firms which have reported in a historic context.

Picture Supply: Zacks Funding Analysis

The Earnings Huge Image

The chart under reveals the This autumn earnings and income progress expectations within the context of the place progress has been within the previous 4 quarters and what’s anticipated within the coming 4 quarters.

Picture Supply: Zacks Funding Analysis

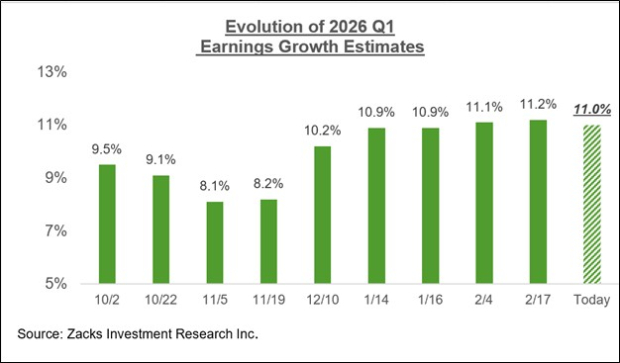

Estimates for the present interval (2026 Q1) have inched down in latest days after persistently transferring greater earlier, because the chart under reveals.

Picture Supply: Zacks Funding Analysis

The chart under reveals the general earnings image on a calendar-year foundation, with double-digit earnings progress anticipated in 2025 and 2026.

Picture Supply: Zacks Funding Analysis

For an in depth have a look at the general earnings image, together with expectations for the approaching intervals, please try our weekly Earnings Developments report >>>> Retail Sector Earnings in Focus

Zacks’ Analysis Chief Names “Inventory Most Prone to Double”

Our workforce of consultants has simply launched the 5 shares with the best likelihood of gaining +100% or extra within the coming months. Of these 5, Director of Analysis Sheraz Mian highlights the one inventory set to climb highest.

This prime choose is a little-known satellite-based communications agency. Area is projected to grow to be a trillion greenback trade, and this firm’s buyer base is rising quick. Analysts have forecasted a significant income breakout in 2025. In fact, all our elite picks aren’t winners however this one may far surpass earlier Zacks’ Shares Set to Double like Hims & Hers Well being, which shot up +209%.

Free: See Our Prime Inventory And 4 Runners Up

Amazon.com, Inc. (AMZN) : Free Inventory Evaluation Report

Macy’s, Inc. (M) : Free Inventory Evaluation Report

Goal Company (TGT) : Free Inventory Evaluation Report

Walmart Inc. (WMT) : Free Inventory Evaluation Report

Finest Purchase Co., Inc. (BBY) : Free Inventory Evaluation Report

Costco Wholesale Company (COST) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.