TL;DR

- Bitcoin miners constructed power infrastructure now price greater than their computing {hardware}.

- AI corporations want precisely the facility supply programs miners spent years establishing.

- Debt markets present collectors view AI infrastructure companies as greater threat than utilities.

There’s an asset Bitcoin miners spent years constructing with out realizing it will at some point be price greater than the compute itself: power supply infrastructure. Substations, transmission interconnections, long-term energy provide agreements, operations groups able to preserving {hardware} working across the clock. All of it value billions of {dollars} and took years to barter. And now it seems to be precisely what the factitious intelligence trade can not construct quick sufficient.

That’s the thesis behind the migration. Not that miners deserted Bitcoin —many nonetheless run each companies in parallel. What they acknowledged was that they owned the bottleneck of the following cycle’s digital financial system: put in power capability in grid-connected places, already operational cooling infrastructure, and technical groups educated in high-density compute environments. Promoting that capability to AI workloads generates margins that mining, topic to Bitcoin value volatility and successive halvings, can not often assure on a sustained foundation.

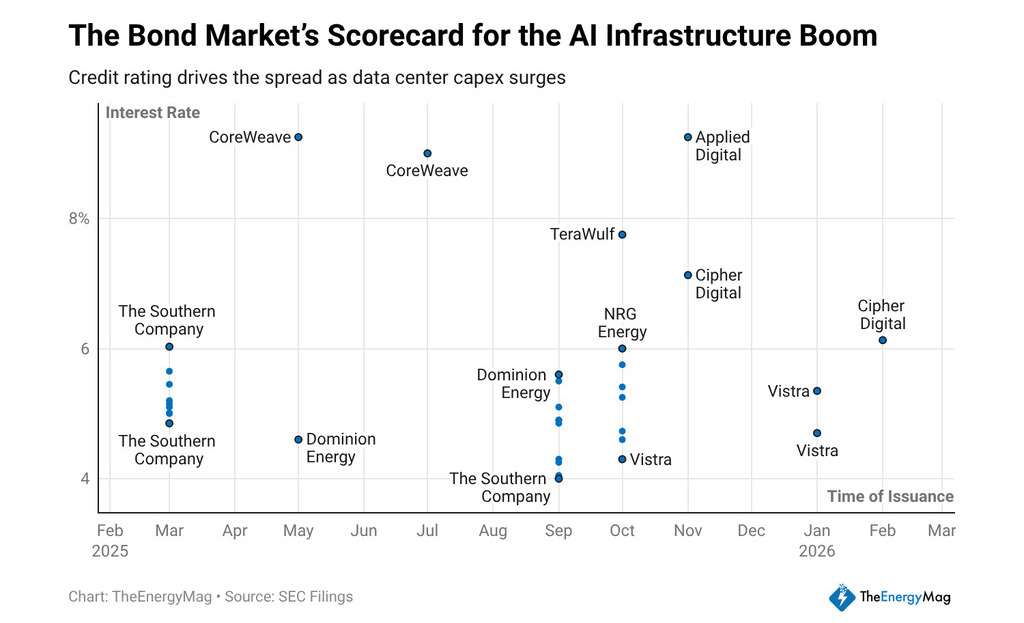

Over the previous twelve months, corporations within the sector raised roughly $33 billion in long-term senior notes, and the coupons they paid inform a exact story about how collectors learn the mannequin. CoreWeave closed placements at 9.25% and 9%. Utilized Digital paid 9.2%. TeraWulf issued at 7.75%. Cipher Mining at 7.125% and 6.125%. All are corporations touring, to various levels, the identical route: from mining operators to AI compute infrastructure suppliers.

What the Value of Cash Says In regards to the Mannequin

A hard and fast-income investor doesn’t finance narratives —they finance money flows. When a creditor expenses an AI infrastructure firm between 300 and 500 foundation factors greater than a regulated utility, they’re expressing an opinion in regards to the predictability of these flows.

Utilities have contract-backed revenues reviewed by regulators, permitted charge constructions, and property with helpful lives measured in many years. Corporations that migrated from mining to AI have offtake agreements —long-term provide contracts with purchasers committing to devour compute capability— however collectors nonetheless don’t grant them the identical institutional standing.

The distinction will not be irrational. An offtake contract with an AI consumer is barely as stable as that consumer’s solvency and the sustained demand for the fashions it runs. If the AI market faces a requirement correction, or if buyer focus amongst a handful of tech corporations creates counterparty threat, the money flows from these operations turn out to be much less predictable than these of an influence distribution firm. Collectors cost for that distinction, and the coupons seen out there mirror precisely that calculation.

For traders in digital property, the unfold carries an extra studying. The differential between what an AI infrastructure firm pays and what a consolidated asset pays equals the price of transition. Till corporations within the sector accumulate sufficient money circulation historical past beneath long-term contracts, the credit score market will maintain treating them as development bets. That pressures working margins, as a result of a part of the money circulation they generate goes immediately into servicing costly debt.

The dimensions of the wager turns into clear when deliberate electrical capability: mining corporations have roughly 30 gigawatts of latest capability in growth geared toward AI workloads, almost triple what they at the moment function.

Not all of that capability will probably be constructed on introduced timelines or at projected prices —allowing delays, transmission grid constraints, and development prices are variables that traditionally compress the returns introduced in investor shows. However the course of capital is evident, and Nvidia’s outcomes —94% earnings development, 73% income development, $68.1 billion in quarterly gross sales— affirm that the compute demand driving these funding selections exhibits no indicators of retreat.

The ensuing enterprise mannequin combines two logics that beforehand operated individually

On one aspect, the logic of the power infrastructure operator: maximize uptime, reduce value per megawatt-hour, negotiate energy provide contracts that defend margins towards spot market volatility. On the opposite, the logic of the compute companies supplier: entice purchasers with intensive workloads, signal long-term contracts that justify the debt issued, and construct a recurring income base that finally convinces collectors to decrease coupons.

The mannequin’s success is determined by whether or not corporations handle to compress that unfold earlier than present debt matures. If in two or three years they will refinance at 5% or 6% as an alternative of the present 9%, the enterprise improves structurally. If offtake contracts don’t renew, if purchasers migrate towards proprietary infrastructure, or if power costs rise sooner than compute service revenues, the fastened value of pricey debt turns into a burden that compresses returns and forces dilution or restructuring.

For a digital asset investor evaluating publicity to the phase, the query will not be whether or not the miners-to-AI migration is sensible as a long-term thesis —it clearly does. The query is which a part of the capital construction is sensible to carry. Debt at 9% affords yield with liquidation precedence, however upside is capped.

Fairness captures the appreciation if the mannequin works, however absorbs losses first if contracts don’t maintain. The unfold on these bonds isn’t just a credit score market information level —it’s the entry value for a query that doesn’t but have a solution.